Sprint - Nextel 2007 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2007 Sprint - Nextel annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

subscriber additions. In previous periods, we had expected that we would be able to produce net post-paid

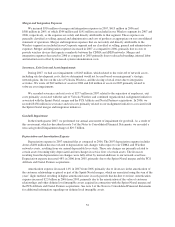

subscriber additions during 2007. In the fourth quarter, we reported a loss of 683,000 post-paid subscribers which

was the most post-paid subscribers we had ever lost in a quarter.

We also updated our forecasted cash flows of the wireless reporting unit during the fourth quarter. This

update considered current economic conditions and trends; estimated future operating results; our views of

growth rates, anticipated future economic and regulatory conditions; and the availability of necessary technology,

network infrastructure, handsets and other devices. Several factors led to a reduction in forecasted cash flows,

including, among others, our ability to attract and retain subscribers, particularly subscribers of our iDEN-based

services, in a highly competitive environment; expected reductions in voice revenue per subscriber; the costs of

acquiring subscribers; and the costs of operating our wireless networks.

Based on the results of our annual assessment of goodwill for impairment, the net book value of the wireless

reporting unit exceeded its fair value. Therefore, we performed the second step of the impairment test to

determine the implied fair value of goodwill. Specifically, we hypothetically allocated the fair value of the

wireless reporting unit as determined in the first step to our recognized and unrecognized net assets, including

allocations to intangible assets such as customer relationships, FCC licenses and trade names. Such items had fair

values substantially in excess of current book values. The resulting implied goodwill was $935 million;

accordingly, we reduced the goodwill recorded prior to this assessment by $29.7 billion to write our goodwill

down to the implied goodwill amount as of December 31, 2007. The $29.7 billion goodwill impairment charge is

our best estimate of the goodwill charge as of December 31, 2007. Any adjustment to that estimated charge

resulting from the completion of the measurement of the impairment loss will be recognized in the first quarter

2008. The allocation discussed above is performed only for purposes of assessing goodwill for impairment;

accordingly, we do not adjust the net book value of the assets and liabilities on our consolidated balance sheet

other than goodwill as a result of this process.

We performed extensive valuation analyses, utilizing both income and market approaches, in our goodwill

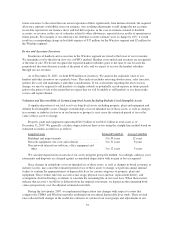

assessment process. The following describes the valuation methodologies used to derive the fair value of the

wireless reporting unit.

•Income Approach: To determine fair value, we discounted the expected cash flows of the wireless

reporting unit. The discount rate used represents the estimated weighted average cost of capital, which

reflects the overall level of inherent risk involved in our wireless operations and the rate of return an

outside investor would expect to earn. To estimate cash flows beyond the final year of our model, we

used a terminal value approach. Under this approach, we used estimated operating income before

interest, taxes, depreciation and amortization in the final year of our model, adjusted it to estimate a

normalized cash flow, applied a perpetuity growth assumption and discounted by a perpetuity discount

factor to determine the terminal value. We incorporated the present value of the resulting terminal

value into our estimate of fair value.

•Market-Based Approach: To corroborate the results of the income approach described above, we

estimated the fair value of our wireless reporting unit using several market-based approaches, including

the value that we derive based on our consolidated stock price as described above. We also used the

guideline company method, which focuses on comparing our risk profile and growth prospects to select

reasonably similar/guideline publicly traded companies.

The determination of fair value of the wireless reporting unit and other assets and liabilities within the

wireless reporting unit requires us to make significant estimates and assumptions. These estimates and

assumptions primarily include, but are not limited to, the discount rate, terminal growth rates, operating income

before depreciation and amortization, or OIBDA and capital expenditures forecasts. Due to the inherent

uncertainty involved in making these estimates, actual results could differ from those estimates. We evaluated the

merits of each significant assumption, both individually and in the aggregate, used to determine the fair value of

the wireless reporting unit, as well as the fair values of the corresponding assets and liabilities within the wireless

reporting unit, and concluded they are reasonable.

58