Sprint - Nextel 2007 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2007 Sprint - Nextel annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

During 2007, we endeavored to retain subscribers and attract new subscribers by improving our customer care and

sales and distribution functions. In addition, we took other actions in an effort to improve our customers’ experience

including improving our network performance by adding cell sites to expand the coverage and capacity of our networks,

enhancing our brand awareness by increased media spending, and broadening our handset portfolio primarily through the

introduction of new CDMA and PowerSource handsets.

We added about 1.6 million net post-paid subscribers on the CDMA network in 2007; however, we have experienced

a continued decline in the number of new post-paid CDMA subscribers in the fourth quarter 2007. Competitive marketing

conditions including increased advertising and promotions by our competitors have contributed to the decline in the

number of new customers. Earlier in the year, we adjusted our credit policy in certain markets in an effort to attract new

subscribers. In late 2007, we adjusted our credit policies and returned to policy standards similar to those in mid 2006,

which also contributed to the decline in subscriber additions on our CDMA platform in the fourth quarter 2007. We

continually monitor and adjust our credit policies in an effort to attract desirable and profitable customers, including our

lower credit quality customers. Our ratio of subscribers with a subprime credit rating to those with a prime credit rating

has decreased slightly from the fourth quarter 2006. Refer to “—Results of Operations—Segment Results of Operations—

Wireless—Wireless Segment Earnings” below for a discussion of subscriber trends.

We have experienced declines in the number of new iDEN post-paid subscribers in recent quarters and we lost about

2.8 million net post-paid subscribers on this network during 2007. Consumer sentiment regarding the iDEN network,

reduced marketing programs and limited new handset offerings at higher than market prices have all contributed to the

decline in new iDEN customers.

We calculate churn by dividing net subscriber deactivations for the quarter by the sum of the average number of

subscribers for each month in the quarter. Net subscriber deactivations are used in the numerator of the churn calculation.

For accounts comprised of multiple subscribers, such as family plans and enterprise accounts, net deactivations are

defined as deactivations in excess of customer activations in a particular account within 30 days. Post-paid churn consists

of both voluntary churn, where the subscriber makes his or her own determination to cease being a customer, and

involuntary churn, where we terminate the customer’s service due to a lack of payment or other reasons. Involuntary

deactivations represent slightly over half of all deactivations on our CDMA network in 2007. Although overall post-paid

churn was relatively flat in 2007 as compared to 2006, post-paid churn on our iDEN platform increased, which was offset

by reduced post-paid churn on our CDMA platform. Voluntary churn on the iDEN network has been adversely impacted

by customer sentiment related to: the network, limited handset offerings at higher than market prices, and customer care

experience. Our overall 2007 post-paid churn remains high relative to that of our competitors for the same reasons.

Prepaid subscriber churn increased as compared to 2006, primarily due to competition in our prepaid and youth markets

from new entrants. Refer to “—Results of Operations—Segment Results of Operations—Wireless—Wireless Segment

Earnings” below for a discussion of churn trends.

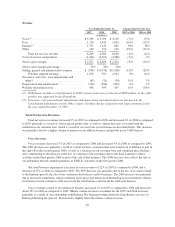

Average Revenue per Subscriber

Below is a table showing our average revenue per post-paid and prepaid subscriber for the past twelve quarters.

Quarter Ended

March 31,

2005

June 30,

2005

September 30,

2005

December 31,

2005

March 31,

2006

June 30,

2006

September 30,

2006

December 31,

2006

March 31,

2007

June 30,

2007

September 30,

2007

December 31,

2007

Average monthly service

revenue per user

Direct post-paid ........... $ 61 $ 62 $63 $63 $62 $62 $61 $60 $59 $60 $59 $58

Direct prepaid ............ — — $37 $37 $36 $34 $33 $32 $32 $31 $30 $28

Average monthly service revenue per subscriber for the quarter is calculated by dividing our quarterly service

revenue by the sum of our average number of subscribers for each month in the quarter. Changes in average monthly post-

paid service revenue are due to changes in the rate plans we offer and usage of our service and applications by subscribers.

The decline in our average monthly voice revenue is primarily due to the loss of subscribers with higher priced service

plans, while new subscribers and the subscribers acquired from the PCS Affiliates have lower priced service plans. In

addition, the decline is partly attributable to the migration of our existing customers to family add-on plans or plans that

include roaming in their service plan, as well as increased sales to businesses and the government, which receive favorable

39