Starbucks 2004 Annual Report Download - page 10

Download and view the complete annual report

Please find page 10 of the 2004 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

|

|

Fiscal 2004 Annual Report 21

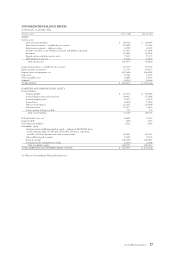

Torrefazione Italia stores.

The Company derived the remaining 15% of total net revenues

from its Specialty Operations. Specialty revenues, which include

licensing revenues and foodservice and other revenues, increased

$129.9 million, or 26.2%, to $625.9 million for the fi scal year

ended 2003, from $496.0 million for the corresponding fi scal

2002 period.

Licensing revenues, which are derived from retail store

licensing arrangements, grocery and warehouse club licensing

and certain other branded-product licensed operations,

increased 31.3% to $409.6 million for the fi scal year ended

2003, from $311.9 million for the corresponding fi scal 2002

period. The increase was due to higher product sales and

royalty revenues from opening 599 new licensed retail stores

during the previous 12 months and growth in the licensed

grocery and warehouse club businesses.

Foodservice and other revenues increased 17.5% to $216.3

million for the fi scal year ended 2003, from $184.1 million

for the corresponding fi scal 2002 period. The increase was

primarily attributable to broader distribution and growth in

new and existing foodservice accounts.

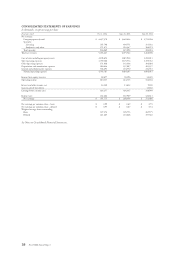

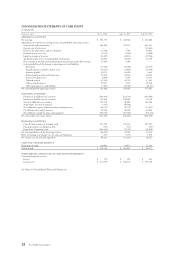

Cost of sales and related occupancy costs increased to 41.4%

of total net revenues in fi scal 2003, from 41.0% in fi scal 2002.

The increase was primarily due to higher green coffee costs

and a shift in specialty revenue mix to lower margin products.

The Company’s green coffee costs reached a historic low for

Starbucks in the second and third fi scal quarters of 2002 and

have gradually increased since then. These increases were

partially offset by leverage gained on fi xed occupancy costs

distributed over an expanded revenue base.

Store operating expenses as a percentage of Company-operated

retail revenues increased to 40.0% in fi scal 2003, from 39.7%

in fi scal 2002, primarily due to higher payroll-related and

advertising expenditures. Payroll-related costs have increased

primarily due to an increase in the number of partners eligible

to participate in the Company’s medical and vacation benefi ts.

Advertising expenditures increased in fi scal 2003 due to

promotions for new and existing products. These increases

were partially offset by lower provisions for asset impairment

for International Company-operated retail stores in 2003 as

compared to the prior year.

Other operating expenses (expenses associated with the

Company’s Specialty Operations) were 22.6% of specialty

revenues in fi scal 2003, compared to 21.4% in fi scal 2002,

primarily due to higher payroll-related expenditures to support

the continued development of the Company’s foodservice

distribution network and international infrastructure, including

regional offi ces and fi eld personnel.

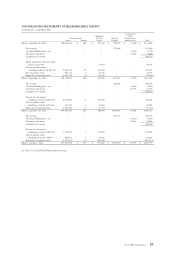

Depreciation and amortization expenses increased to $237.8

million in fi scal 2003, from $205.6 million in fi scal 2002,

primarily due to opening 602 Company-operated retail stores

during the previous 12 months and the refurbishment of

existing Company-operated retail stores.

General and administrative expenses increased to $244.6 million

in fi scal 2003, compared to $234.6 million in fi scal 2002, which

included an $18.0 million charge for the litigation settlement of

two California class action lawsuits. Excluding the litigation

charge, general and administrative expenses increased $28.0

million from the comparable fi scal 2002 period due to higher

payroll-related expenditures and costs related to the acquisition

of Seattle Coffee Company. General and administrative

expenses as a percentage of total net revenues decreased to 6.0%

in fi scal 2003, compared to 7.1% in fi scal 2002.

Operating income increased 34.3% to $424.7 million in fi scal

2003, from $316.3 million in fi scal 2002. The operating margin

increased to 10.4% of total net revenues in fi scal 2003, compared

to 9.6% in fi scal 2002, primarily due to leverage gained on fi xed

costs distributed over an expanding revenue base, partially offset

by higher green coffee costs, as discussed above.

Income from equity investees was $38.4 million in fi scal

2003, compared to $33.4 million in fi scal 2002. The increase

was mainly attributable to continued strong results by The

North American Coffee Partnership, the Company’s 50%-

owned partnership with the Pepsi-Cola Company, from

expanded ready-to-drink product lines, lower direct costs and

manufacturing effi ciencies. Partially offsetting this increase

was the Company’s proportionate share of the net losses of

Starbucks Japan in fi scal 2003, compared to a net profi t in fi scal

2002, primarily due to lower average sales per store.

Net interest and other income, which primarily consists of

interest income, increased to $11.6 million in fi scal 2003, from

$9.3 million in fi scal 2002. The growth was a result of increased

interest received on higher balances of cash, cash equivalents

and liquid securities during fi scal 2003, compared to the prior

year, as well as gains realized on market revaluations of the

Company’s trading securities, compared to realized losses on

this portfolio in the prior year.

The Company’s effective tax rate for fi scal 2003 was 38.5%

compared to 37.3% in fi scal 2002, as a result of a shift in the

composition of the Company’s pretax earnings in fi scal 2003.

Operations taxed in the United States had higher pretax earnings

and International operations generated greater nondeductible

losses during fi scal 2003 than during fi scal 2002.