Starbucks 2004 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2004 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

|

|

Fiscal 2004 Annual Report 31

the related accumulated derivative gains or losses are recognized

into net earnings in “Interest and other income, net” on the

consolidated statements of earnings.

Forward contract effectiveness for cash fl ow hedges is calculated

by comparing the fair value of the contract to the change in

value of the anticipated transaction using forward rates on a

monthly basis. For net investment hedges, the spot-to-spot

method is used to calculate effectiveness. Any ineffectiveness is

recognized immediately in “Interest and other income, net” on

the accompanying consolidated statements of earnings.

Inventories

Inventories are stated at the lower of cost (primarily moving

average cost) or market. The Company records inventory

reserves for obsolete and slow-moving items and for estimated

shrinkage between physical inventory counts. Inventory reserves

are based on inventory turnover trends, historical experience and

application of the specifi c identifi cation method.

Property, Plant and Equipment

Property, plant and equipment are carried at cost less

accumulated depreciation. Depreciation of property, plant and

equipment, which includes assets under capital leases, is provided

on the straight-line method over estimated useful lives, generally

ranging from two to seven years for equipment and 30 to 40

years for buildings. Leasehold improvements are amortized over

the shorter of their estimated useful lives or the related lease life,

generally 10 years. The portion of depreciation expense related to

production and distribution facilities is included in “Cost of sales

and related occupancy costs” on the accompanying consolidated

statements of earnings. The costs of repairs and maintenance are

expensed when incurred, while expenditures for refurbishments

and improvements that signifi cantly add to the productive

capacity or extend the useful life of an asset are capitalized. When

assets are retired or sold, the asset cost and related accumulated

depreciation are eliminated with any remaining gain or loss

refl ected in net earnings.

Goodwill and Other Intangible Assets

At the beginning of fi scal 2003, Starbucks adopted SFAS

No. 142, “Goodwill and Other Intangible Assets” (“SFAS 142”).

As a result, the Company discontinued amortization of its

goodwill and indefi nite-lived trademarks and determined that

provisions for impairment were unnecessary. Impairment tests

are performed annually in June and more frequently if facts and

circumstances indicate goodwill carrying values exceed estimated

reporting unit fair values and if indefi nite useful lives are no

longer appropriate for the Company’s trademarks. If the

nonamortization provision of SFAS 142 had been applied to

fi scal 2002, net earnings would have been $214.7 million, as

compared to actual net earnings of $212.7 million. Basic earnings

per share for fi scal 2002 would have increased to $0.56 per share

from $0.55 per share, while diluted earnings per share would

have remained unchanged. Defi nite-lived intangibles, which

mainly consist of contract-based patents and copyrights, are

amortized over their estimated useful lives. For further

information on goodwill and other intangible assets, see Note 9.

Long-Lived Assets

When facts and circumstances indicate that the carrying values of

long-lived assets may be impaired, an evaluation of recoverability

is performed by comparing the carrying values of the assets to

projected future cash fl ows in addition to other quantitative and

qualitative analyses. Upon indication that the carrying values

of such assets may not be recoverable, the Company recognizes

an impairment loss by a charge against current operations.

Property, plant and equipment assets are grouped at the lowest

level for which there are identifi able cash fl ows when assessing

impairment. Cash fl ows for retail assets are identifi ed at the

individual store level.

Insurance Reserves

The Company uses a combination of insurance and self-insurance

mechanisms, including a wholly owned captive insurance entity

and participation in a reinsurance pool, to provide for the

potential liabilities for workers’ compensation, general liability,

property insurance, director and offi cers’ liability insurance,

vehicle liability and employee healthcare benefi ts. Liabilities

associated with the risks that are retained by the Company are

estimated, in part, by considering historical claims experience,

demographic factors, severity factors and other actuarial

assumptions. The estimated accruals for these liabilities could

be signifi cantly affected if future occurrences and claims differ

from these assumptions and historical trends. As of October 3,

2004, and September 28, 2003, these reserves were $77.6 million

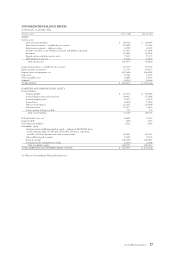

and $51.6 million, respectively, and were included in “Accrued

compensation and related costs” and “Other accrued expenses”

on the consolidated balance sheets.

Revenue Recognition

Company-operated retail store revenues are recognized when

payment is tendered at the point of sale. Revenues from

stored value cards are recognized upon redemption. Until

the redemption of stored value cards, outstanding customer

balances on such cards are included in “Deferred revenue” on the

accompanying consolidated balance sheets. Specialty revenues

consist primarily of product sales to customers other than

through Company-operated retail stores, as well as royalties and

other fees generated from licensing operations. Sales of coffee, tea

and related products are generally recognized upon shipment to

customers, depending on contract terms. Initial nonrefundable

development fees required under licensing agreements are

recognized upon substantial performance of services for new

market business development activities, such as initial business,

real estate and store development planning, as well as providing

operational materials and functional training courses for opening

new licensed retail markets. Additional store licensing fees are

recognized when new licensed stores are opened. Royalty revenues

based upon a percentage of reported sales and other continuing

fees, such as marketing and service fees, are recognized on a

monthly basis when earned. Arrangements involving multiple

elements and deliverables are individually evaluated for revenue

recognition. Cash payments received in advance of product or

service delivery are recorded as deferred revenue. Consolidated

revenues are net of all intercompany eliminations for wholly

owned subsidiaries and for licensees accounted for under the

equity method based on the Company’s percentage ownership.

All revenues are recognized net of any discounts.

Advertising

The Company expenses costs of advertising the fi rst time the

advertising campaign takes place. Total advertising expenses,

recorded in “Store operating expenses” and “Other operating

expenses” on the accompanying consolidated statements of

earnings totaled $68.3 million, $49.5 million and $25.6 million

in 2004, 2003 and 2002, respectively.

Store Preopening Expenses

Costs incurred in connection with the start-up and promotion of

new store openings are expensed as incurred.

Rent Expense

Certain of the Company’s lease agreements provide for scheduled

rent increases during the lease terms or for rental payments

commencing at a date other than the date of initial occupancy.

Minimum rental expenses are recognized on a straight-line basis

over the terms of the leases.