Starbucks 2004 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2004 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33

|

|

Fiscal 2004 Annual Report 35

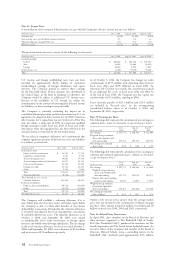

revenues generated from, equity investees. Revenues generated

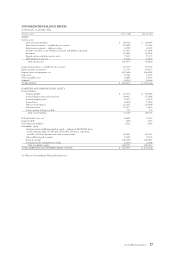

from these related parties, net of eliminations, were $75.2

million, $68.0 million and $67.7 million in fi scal years 2004,

2003 and 2002, respectively. Related costs of sales, net of

eliminations, were $37.5 million, $35.7 million and $37.9

million in fi scal years 2004, 2003 and 2002, respectively.

As of October 3, 2004, the aggregate market value of the

Company’s investment in Starbucks Coffee Japan, Ltd., was

approximately $149.9 million based on its available quoted

market price.

Cost Method

The Company has equity interests in entities to develop

Starbucks licensed retail stores in certain Chinese markets and

in Puerto Rico, Germany, Mexico, Chile, Cyprus and Greece.

As of October 3, 2004, management determined that the

estimated fair value of each cost method investment exceeded its

carrying value as part of the formal adoption of the impairment

provisions of EITF 03-1.

Starbucks has the ability to acquire additional interests in some

of its cost method investees at certain intervals. Depending

on the Company’s total percentage of ownership interest and

its ability to exercise signifi cant infl uence over fi nancial and

operating policies, additional investments may require the

retroactive application of the equity method of accounting.

Other Investments

Starbucks has investments in privately held equity securities that

are recorded at their estimated fair values.

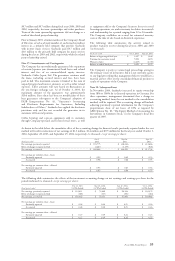

Note 8: Property, Plant and Equipment

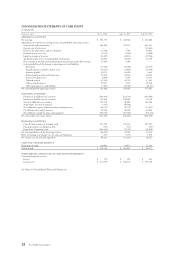

Property, plant and equipment are recorded at cost and consist

of the following (in thousands):

Fiscal year ended Oct 3, 2004 Sept 28, 2003

Land $ 13,118 $ 11,414

Buildings 66,468 64,427

Leasehold improvements 1,497,941 1,311,024

Roasting and store equipment 683,747 613,825

Furniture, fixtures and other 415,307 375,854

2,676,581 2,376,544

Less accumulated depreciation

and amortization (1,298,270) (1,049,810)

1,378,311 1,326,734

Work in progress 93,135 58,168

Property, plant and equipment, net $ 1,471,446 $ 1,384,902

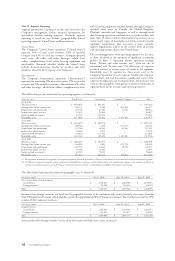

Note 9: Other Intangible Assets and Goodwill

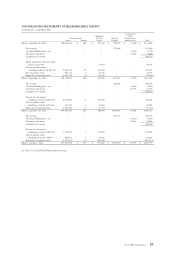

As of October 3, 2004, indefi nite-lived intangibles were $24.3

million and defi nite-lived intangibles, which collectively had a

remaining weighted average useful life of approximately eight

years, were $2.5 million, net of accumulated amortization

of $1.3 million. As of September 28, 2003, indefi nite-lived

intangibles were $23.3 million and defi nite-lived intangibles

were $1.6 million, net of accumulated amortization of $0.9

million. Amortization expense for defi nite-lived intangibles

was $0.5 million and $0.4 million during fi scal 2004 and

2003, respectively.

The following table summarizes the estimated amortization

expense for each of the next fi ve fi scal years (in thousands):

Fiscal year ending

2005 $ 536

2006 606

2007 647

2008 782

2009 908

Total 3,479

During fi scal 2004 and 2003, goodwill increased by

approximately $6.1 million for the acquisition of licensed

operations in Singapore and $43.3 million for the acquisition of

the Seattle Coffee Company, respectively. No impairment was

recorded during fi scal 2004 or 2003.

The following table summarizes goodwill by operating segment

(in thousands):

Fiscal year ended Oct 3, 2004 Sept 28, 2003

United States $ 60,540 $ 60,965

International 8,410 2,379

Total $ 68,950 $ 63,344

The reduction in goodwill assigned to the United States

operating segment during fi scal 2004 refl ects a net decrease for

Seattle Coffee Company, primarily from adjustments to values

estimated in the initial purchase price allocation. The increase

in goodwill assigned to the International operating segment

during fi scal 2004 relates to the acquisition of licensed

operations in Singapore, partially offset by fl uctuations in

foreign exchange rates.

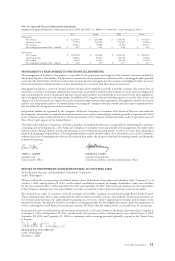

Note 10: Long-term Debt

In September 1999, Starbucks purchased the land and building

comprising its York County, Pennsylvania, roasting plant and

distribution facility. The total purchase price was $12.9 million.

In connection with this purchase, the Company assumed

loans totaling $7.7 million from the York County Industrial

Development Corporation. The remaining maturities of these

loans range from fi ve to six years, with interest rates from 0.0%

to 2.0%.

Scheduled principal payments on long-term debt are as follows

(in thousands):

Fiscal year ending

2005 $ 735

2006 748

2007 762

2008 775

2009 790

Thereafter 543

Total principal payments $ 4,353

Note 11: Leases

The Company leases retail stores, roasting and distribution

facilities and offi ce space under operating leases expiring

through 2027. Most lease agreements contain renewal options

and rent escalation clauses. Certain leases provide for contingent

rentals based upon gross sales.

Rental expense under these lease agreements was as follows

(in thousands):

Fiscal year ended Oct 3, 2004 Sept 28, 2003 Sept 29, 2002

Minimum rentals –

retail stores $ 283,351 $ 237,742 $ 200,827

Minimum rentals – other 28,064 22,887 19,143

Contingent rentals 24,638 12,274 5,415

Total $ 336,053 $ 272,903 $ 225,385

Minimum future rental payments under noncancelable lease

obligations as of October 3, 2004, are as follows (in thousands):

Fiscal year ending

2005 $ 355,079

2006 340,360

2007 321,047

2008 299,601

2009 272,806

Thereafter 1,020,143

Total minimum lease payments $ 2,609,036