Walmart 2012 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2012 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

|

|

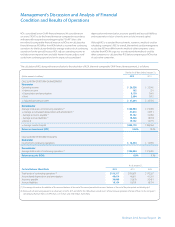

Management’s Discussion and Analysis of Financial

Condition and Results of Operations

20 Walmart 2012 Annual Report

Comparable store and club sales in the U.S., including fuel, increased 1.6% in fi scal 2012 and decreased 0.6% and 0.8% in fi scal 2011 and 2010,

respectively. U.S. comparable store sales increased during fi scal 2012 primarily due to an increase in average ticket, partially off set by a decline in traffi c.

Comparable club sales were higher during fi scal 2012 due to a larger member base driving increased traffi c, as well as a broader assortment of items.

Total U.S. comparable store and club sales decreased during fi scal 2011 primarily due to a decline in customer traffi c. Although customer traffi c

increased in fi scal 2010, comparable store and club sales in the U.S. were lower than those in the previous fi scal year due to defl ation in certain

merchandise categories and lower fuel prices.

As we continue to add new stores and clubs in the U.S., we do so with an understanding that additional stores and clubs may take sales away from

existing units. We estimate the negative impact on comparable store and club sales as a result of opening new stores and clubs was approximately

0.8% in fi scal 2012 and 2011 and 0.6% in fi scal 2010.

Leverage

Operating Income

Fiscal Years Ended January 31,

(Dollar amounts in millions)

2012 2011 2010

Operating Percent Percent Operating Percent Percent Operating Percent

Income of Total Change Income of Total Change Income of Total

Walmart U.S. $20,367 76.7% 2.2% $19,919 78.0% 3.1% $19,314 80.5%

Walmart International 6,214 23.4% 10.8% 5,606 21.9% 14.4% 4,901 20.4%

Sam’s Club 1,865 7.0% 9.0% 1,711 6.7% 12.9% 1,515 6.3%

Other unallocated (1,888) -7.1% 11.5% (1,694) -6.6% -2.0% (1,728) -7.2%

Total operating income $26,558 100.0% 4.0% $25,542 100.0% 6.4% $24,002 100.0%

We believe comparing the growth of our operating expenses to the

growth of our net sales and comparing the growth of our operating

income to the growth of our net sales are meaningful measures as they

indicate how eff ectively we manage costs and leverage operating

expenses. Our objective is to grow operating expenses at a slower rate

than net sales and to grow operating income at a faster rate than net sales.

On occasion, we may make strategic growth investments that may, at

times, cause our operating expenses to grow at a rate faster than net sales

and that may grow our operating income at a slower rate than net sales.

Operating Expenses

We leveraged operating expenses in fi scal 2012 and 2011. In fi scal 2012,

our operating expenses increased 4.8% compared to fi scal 2011, while

net sales increased 5.9% in fi scal 2012 compared to fi scal 2011. Operating

expenses grew at a slower rate than net sales due to our continued focus

on expense management. Our Global eCommerce initiatives contributed

to the majority of the increase in operating expenses, as we continue

to invest in our e-commerce platforms. Depreciation expense increased

year-over-year based on our fi nancial system investments with the

remainder of the increase being driven by multiple items, none of which

were individually signifi cant. In fi scal 2011, our operating expenses

increased 1.7% compared to fi scal 2010, while net sales increased 3.4%

during fi scal 2011 compared to fi scal 2010. Operating expenses grew at a

slower rate than net sales in fi scal 2011 due to improved labor productivity

and organizational changes made at the end of fi scal 2010 designed to

strengthen and streamline our operations, as well as a reduction in certain

incentive plan expenses.

Operating Income

As a result of the factors discussed above and our investment in price

for products sold in our retail operations, which reduced our gross

margin, our operating income increased 4.0% and 6.4% in fi scal 2012

and 2011, respectively, while net sales increased 5.9% and 3.4% in fi scal

2012 and 2011, respectively.

Returns

Return on Investment

Management believes return on investment (“ROI”) is a meaningful metric

to share with investors because it helps investors assess how eff ectively

Walmart is deploying its assets. Trends in ROI can fl uctuate over time as

management balances long-term potential strategic initiatives with any

possible short-term impacts. ROI was 18.6% and 19.2% for fi scal 2012 and

2011, respectively. The decrease in ROI in fi scal 2012 from fi scal 2011 was

due primarily to additional investments in property, plant and equipment,

Global eCommerce and higher inventories, as well as price investment

ahead of full realization of productivity improvements. In future periods,

productivity gains are expected to align more closely with price invest-

ments. Additionally, to a lesser degree, ROI was positively impacted by

currency translation fl uctuations, but off set by acquisitions.

We defi ne ROI as adjusted operating income (operating income plus

interest income, depreciation and amortization, and rent expense) for

the fi scal year divided by average invested capital during that period.

We consider average invested capital to be the average of our beginning

and ending total assets of continuing operations, plus average accumulated

depreciation and average amortization, less average accounts payable

and average accrued liabilities for that period, plus a rent factor equal to

the rent for the fi scal year multiplied by a factor of eight.