Walmart 2012 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2012 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

|

|

46 Walmart 2012 Annual Report

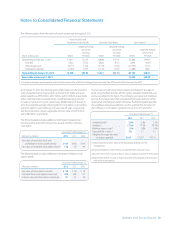

9 Derivative Financial Instruments

The Company uses derivative fi nancial instruments for hedging and

non-trading purposes to manage its exposure to changes in interest and

currency exchange rates, as well as to maintain an appropriate mix of

fi xed- and fl oating-rate debt. Use of derivative fi nancial instruments in

hedging programs subjects the Company to certain risks, such as market

and credit risks. Market risk represents the possibility that the value of the

derivative instrument will change. In a hedging relationship, the change

in the value of the derivative is off set to a great extent by the change in

the value of the underlying hedged item. Credit risk related to derivatives

represents the possibility that the counterparty will not fulfi ll the terms

of the contract. The notional, or contractual amount of the Company’s

derivative fi nancial instruments, is used to measure interest to be paid or

received and does not represent the Company’s exposure due to credit

risk. Credit risk is monitored through established approval procedures,

including setting concentration limits by counterparty, reviewing credit

ratings and requiring collateral (generally cash) from the counterparty

when appropriate. The Company’s transactions are with counterparties

rated “A-” or better by nationally recognized credit rating agencies. In

connection with various derivative agreements with counterparties, the

Company held cash collateral from these counterparties of $387 million

and $344 million at January 31, 2012 and 2011, respectively. The Company’s

policy is to record cash collateral exclusive of any derivative asset, and

any collateral holdings are refl ected in the Company’s accrued liabilities

as amounts due to the counterparties. Furthermore, as part of the master

netting arrangements with these counterparties, the Company is also

required to post collateral if the derivative liability position exceeds

$150 million. The Company has no outstanding collateral postings; and

in the event of providing cash collateral, the Company would record

the posting as a receivable exclusive of any derivative liability.

When the Company uses derivative fi nancial instruments for the purpose

of hedging its exposure to interest and currency exchange rates, the

contract terms of a hedged instrument closely mirror those of the

hedged item, providing a high degree of risk reduction and correlation.

Contracts that are eff ective at meeting the risk reduction and correlation

criteria are recorded using hedge accounting. If a derivative instrument

is a hedge, depending on the nature of the hedge, changes in the fair

value of the instrument are either off set against the change in fair value

of the hedged assets, liabilities or fi rm commitments through earnings

or recognized in accumulated other comprehensive income (loss) until

the hedged item is recognized in earnings. The ineff ective portion of an

instrument’s change in fair value is immediately recognized in earnings

during the period. Instruments that do not meet the criteria for hedge

accounting, or contracts for which the Company has not elected hedge

accounting, are valued at fair value with unrealized gains or losses

reported in earnings during the period of change.

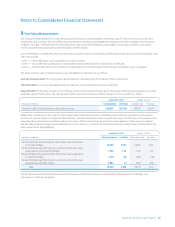

Fair Value Instruments

The Company is party to receive fi xed-rate, pay fl oating-rate interest rate

swaps to hedge the fair value of fi xed-rate debt. The notional amounts

are used to measure interest to be paid or received and do not represent

the exposure due to credit loss. The Company’s interest rate swaps that

receive fi xed-interest rate payments and pay fl oating-interest rate pay-

ments are designated as fair value hedges. As the specifi c terms and

notional amounts of the derivative instruments match those of the

instruments being hedged, the derivative instruments were assumed to

be perfectly eff ective hedges and all changes in fair value of the hedges

were recorded in long-term debt and accumulated other comprehensive

income (loss) in the Company’s Consolidated Balance Sheets with no net

impact in the Company’s Consolidated Statements of Income. These fair

value instruments will mature on various dates ranging from April 2012

to May 2014.

Net Investment Instruments

The Company is party to cross-currency interest rate swaps that hedge

its net investments, as well as its currency exchange rate fl uctuation

exposure associated with the forecasted payments of principal and

interest of non-U.S. denominated debt. The agreements are contracts to

exchange fi xed-rate payments in one currency for fi xed-rate payments

in another currency. All changes in the fair value of these instruments are

recorded in accumulated other comprehensive income (loss), off setting

the currency translation adjustment that is also recorded in accumulated

other comprehensive income (loss). These instruments will mature on

dates ranging from October 2023 to February 2030.

The Company has outstanding debt of approximately £3.0 billion as of

January 31, 2012 and 2011 that is designated as a hedge of the Company’s

net investment in the United Kingdom. The Company also has outstanding

debt of approximately ¥275.0 billion and ¥437.0 billion as of January 31,

2012 and 2011, respectively, that is designated as a hedge of the Company’s

net investment in Japan. Any translation of non-U.S.-denominated debt

is recorded in accumulated other comprehensive income (loss), off setting

the currency translation adjustment that is also recorded in accumulated

other comprehensive income (loss). These instruments will mature on

dates ranging from January 2013 to January 2039.

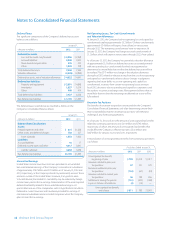

Cash Flow Instruments

The Company is party to receive fl oating-rate, pay fi xed-rate interest rate

swaps to hedge the interest rate risk of certain non-U.S.-denominated

debt. The swaps are designated as cash fl ow hedges of interest rate risk.

Amounts reported in accumulated other comprehensive income (loss)

related to derivatives are reclassifi ed from accumulated other comprehensive

income (loss) to earnings as interest payments are made on the Company’s

variable-rate debt, converting the fl oating-rate interest expense into

fi xed-rate interest expense. These cash fl ow instruments will mature on

dates ranging from August 2013 to July 2015.

The Company is also party to receive fi xed-rate, pay fi xed-rate cross-currency

interest rate swaps to hedge the currency exposure associated with the

forecasted payments of principal and interest of non-U.S.-denominated

debt. The swaps are designated as cash fl ow hedges of the currency risk

related to payments on the non-U.S.-denominated debt. The eff ective

portion of changes in the fair value of derivatives designated as cash fl ow

hedges of foreign exchange risk is recorded in other comprehensive

income (loss) and is subsequently reclassifi ed into earnings in the period

that the hedged forecasted transaction aff ects earnings. The hedged

items are recognized foreign-currency denominated liabilities that are

remeasured at spot exchange rates each period, and the assessment of

eff ectiveness (and measurement of any ineff ectiveness) is based on total

changes in the derivative’s cash fl ows. As a result, the amount reclassifi ed

into earnings each period includes an amount that off sets the related

transaction gain or loss arising from that remeasurement and the adjustment

to earnings for the period’s allocable portion of the initial spot-forward

difference associated with the hedging instrument. These cash flow

instruments will mature on dates ranging from September 2029 to

March 2034. Any ineffectiveness with these instruments has been

and is expected to be immaterial.

Notes to Consolidated Financial Statements