HSBC 2006 Annual Report Download - page 194

Download and view the complete annual report

Please find page 194 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

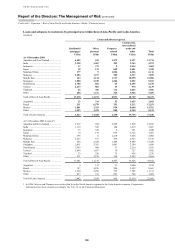

HSBC HOLDINGS PLC

Report of the Directors: The Management of Risk (continued)

Credit risk > Exposure / Credit quality > Loans and advances

192

outstandings comprise loans and advances

(excluding settlement accounts), amounts receivable

under finance leases, acceptances, commercial bills,

certificates of deposit, and debt and equity securities

(net of short positions), and exclude accrued interest

and intra-HSBC exposures.

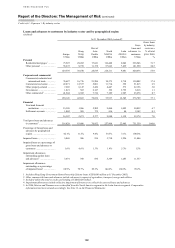

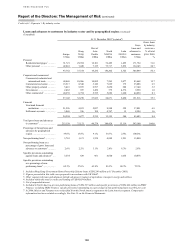

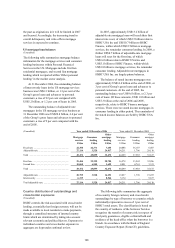

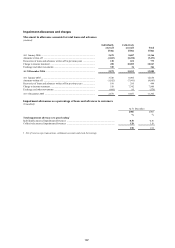

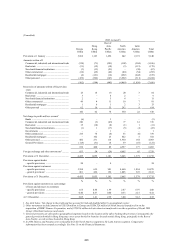

In-country foreign currency and cross-border outstandings

(Unaudited)

Banks

Government

and official

institutions Other Total

US$bn US$bn US$bn US$bn

At 31 December 2006

UK ................................................................................... 24.8 – 33.5 58.3

Germany ......................................................................... 23.7 18.9 2.0 44.6

US ................................................................................... 9.5 12.7 16.2 38.4

France ............................................................................. 22.1 2.4 6.1 30.6

The Netherlands .............................................................. 14.4 2.1 3.9 20.4

Italy ................................................................................. 4.7 12.5 1.4 18.6

At 31 December 2005

UK ................................................................................... 19.6 3.7 16.2 39.5

US ................................................................................... 10.2 11.1 17.1 38.4

Germany ......................................................................... 21.6 12.7 3.3 37.6

France ............................................................................. 11.5 4.7 5.4 21.6

The Netherlands .............................................................. 11.9 2.6 4.4 18.9

Italy ................................................................................. 4.4 10.6 3.5 18.5

At 31 December 2004

UK ................................................................................... 19.7 3.8 24.5 48.0

US ................................................................................... 9.2 13.3 14.0 36.5

Germany ......................................................................... 17.8 10.4 4.0 32.2

France ............................................................................. 11.1 3.7 4.6 19.4

Italy ................................................................................. 5.7 9.7 2.1 17.5

The Netherlands .............................................................. 9.1 2.2 4.2 15.5

Hong Kong ..................................................................... 1.6 1.1 10.3 13.0

At 31 December 2006, HSBC had in-country foreign

currency and cross-border outstandings to

counterparties in Australia and Hong Kong of

between 0.75 per cent and 1 per cent of total assets.

The aggregate in-country foreign currency and cross-

border outstandings were Australia: US$17.5 billion;

Hong Kong: US$15.5 billion.

At 31 December 2005, HSBC had in-country

foreign currency and cross-border outstandings to

counterparties in Hong Kong, Australia and Canada

of between 0.75 per cent and 1 per cent of total

assets. The aggregate in-country foreign currency

and cross-border outstandings were Hong Kong:

US$14.6 billion; Australia: US$12.5 billion; Canada:

US$11.7 billion.

At 31 December 2004, HSBC had in-country

foreign currency and cross-border outstandings to

counterparties in Australia and Canada of between

0.75 per cent and 1 per cent of total assets. The

aggregate in-country foreign currency and cross-

border outstandings were Australia: US$12.7 billion;

Canada: US$11.8 billion.

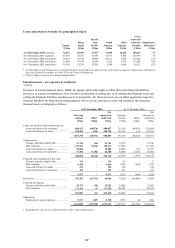

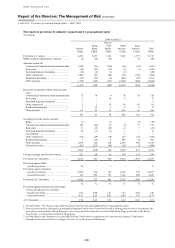

Credit quality

The following tables reflect broadly stable credit

quality across the majority of the Group’s

businesses. However, loans and advances in grades

1-3 (satisfactory risk) declined to 91.7 per cent

(2005: 96.4 per cent) of loans and advances to

customers neither past due nor impaired. This was

mainly due to the transfer of the US mortgage

services book of US$44.5 billion to grades 4 and 5 to

reflect increased scrutiny of this portfolio for the

reasons explained on page 189. Excluding this

realignment, satisfactory risk across the remainder of

the Group showed a marginally improving trend.

The deterioration in quality in US first lien and

second lien mortgages (and, to a lesser extent, UK

personal unsecured portfolios) also reflected in an

increase in the proportion of customer loans and

advances which were past due but not impaired to

1.28 per cent (2005: 1.17 per cent).

Credit quality of loans and advances to banks

was stable.