HSBC 2006 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

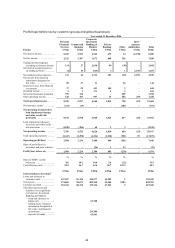

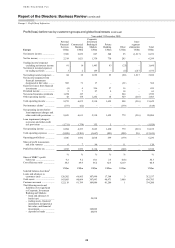

HSBC HOLDINGS PLC

Report of the Directors: Business Review (continued)

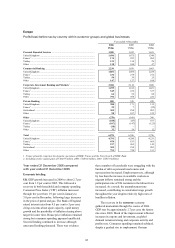

Europe > 2006

36

to raising deposits through transactional and savings

accounts and, as a result, deposit balances rose by

37 per cent and current account balances by 8 per

cent. The benefit of this volume growth was partly

offset by spread compression on sterling-

denominated accounts as customers were offered

more attractive pricing.

HSBC boosted the recruitment of small and

micro business customers in the UK by holding

commercial theme weeks and increasing client

contact by embedding business specialists in selected

branches. These initiatives delivered increases in the

number of start-up accounts and the number of

customers who switched their business from other

banks to HSBC. Higher-value international and

foreign currency accounts rose as a consequence.

Net interest income in France was broadly in

line with 2005 as the benefit of strong balance sheet

growth, driven by the acquisition of new customers

and improved levels of customer retention, was

offset by narrowing spreads from competitive market

pressures and lower earnings from free funds.

Net interest income in Turkey increased by

41 per cent, driven by a doubling in lending

balances. HSBC extended its geographic coverage

through expansion of the branch network, including

the launch of eight new centres dedicated to smaller

commercial customers, and these boosted customer

recruitment. The introduction of pre-approved credit

limits for existing customers also contributed to

lending growth, and the focus on attracting liability

products helped more than double deposit balances.

Net fee income increased by 4 per cent to

US$1,707 million. Current account and money

transmission fees rose as a result of customer

recruitment and higher transaction volumes in most

countries. In the UK, client workshops and other

promotional activities were deployed to support

increased sales of treasury products, boosting

treasury revenue as foreign exchange volumes grew.

In France a 2 per cent increase in income was largely

in transactional current account fees, reflecting

growth in the customer base.

Other operating income was 41 per cent lower

than in 2005 and reflected lower asset finance

revenues following the sale of the UK fleet

management business referred to above. This was

partly offset by the inclusion of Commercial

Banking’s share of the gain on the sale of

HSBC’s stake in The Cyprus Popular Bank

(US$38 million), and the income from UK branch

sale and lease-back transactions.

Credit quality in Commercial Banking was

stable in most countries. In the UK, loan impairment

charges and other credit risk provisions fell by

16 per cent, largely due to the non-recurrence of an

individual loan impairment allowance against a

single customer in 2005. Excluding this, there was a

modest decline in UK impairment charges, as the

effect of lending growth was more than offset by

improved credit quality, particularly in relation to

HSBC’s larger exposures. In France, loan

impairment charges, while remaining low, returned

to a more normal level after relatively high

recoveries in 2005. In Turkey, higher loan

impairment charges reflected growth in lending.

Operating expenses decreased by 1 per cent.

Excluding the sale of the UK fleet management

activities referred to above, costs were 4 per cent

higher than in 2005, reflecting investment to drive

business growth throughout the region. As a result of

revenues growing significantly faster than costs,

there was a 3.1 percentage point improvement in the

cost efficiency ratio. In the UK, increased costs

reflected the recruitment of additional sales staff and

higher IT expenditure. Costs in France fell by 2 per

cent compared with 2005 as savings from cost

control offset increases from the recruitment of

additional sales staff and expenses associated with

the migration to common IT platforms. In Turkey,

recruitment and marketing costs incurred in support

of the growing small and micro businesses drove a

38 per cent rise in expenses.

Corporate, Investment Banking and Markets

reported a pre-tax profit of US$2,304 million, an

increase of 5 per cent, compared with 2005. A

reduction in recoveries of loan impairment charges

and lower private equity gains masked strong growth

in core operating activities. Global Markets’

revenues were 36 per cent higher than in 2005 as

robust performances in the global capital markets

and securities services businesses were

complemented by strong trading gains. The cost

efficiency ratio improved modestly compared with

2005.

Total operating income was US$6,560 million,

17 per cent higher than in 2005. This was despite the

fact that in the UK, France and Turkey, balance

sheet management revenues continued to fall,

resulting in an overall decline of 56 per cent. This

shortfall was partly offset by higher net interest

income in HSBC Securities Services as customer

volumes grew in higher-value products such as

securities lending and foreign exchange. The lending

business delivered a 13 per cent increase in corporate

balances and corporate spreads remained broadly in

line with 2005.