HSBC 2006 Annual Report Download - page 431

Download and view the complete annual report

Please find page 431 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

421 -

422

422 -

423

423 -

424

424 -

425

425 -

426

426 -

427

427 -

428

428 -

429

429 -

430

430 -

431

431 -

432

432 -

433

433 -

434

434 -

435

435 -

436

436 -

437

437 -

438

438 -

439

439 -

440

440 -

441

441 -

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

429

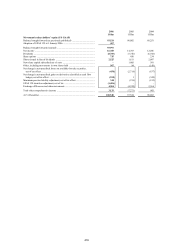

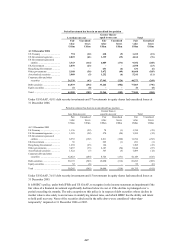

Loans outside the scope of SFAS 114

For smaller-balance homogeneous loans for which future cash flows from written-off balances can reasonably be

estimated on a portfolio basis, an asset equal to the present value of the cash flows is recognised under IFRSs as

it was previously under UK GAAP. This asset is not recognised for US GAAP purposes. This divergence

resulted in lower net income in 2006 of US$45 million (2005: US$20 million higher) under US GAAP compared

with IFRSs, and a reduction in the carrying value of loans and advances to customers and shareholders’ equity at

31 December 2006 of US$372 million (2005: US$327 million).

(i) Earnings per share

Basic earnings per share under US GAAP, SFAS 128 ‘Earnings per Share’, is calculated by dividing net income

attributable to ordinary shareholders of the parent company of US$16,268 million (2005: US$14,703 million;

2004: US$12,506 million) by the weighted average number of ordinary shares in issue in 2006 of 11,214 million

(2005: 11,042 million; 2004: US$10,916 million).

Diluted earnings per share under US GAAP is calculated by dividing net income, which requires no adjustment

for the effects of dilutive ordinary potential shares, by the weighted average number of shares outstanding plus

the weighted average number of ordinary shares that would be issued on conversion of all the dilutive potential

ordinary shares in 2006 of 11,324 million (2005: 11,175 million; 2004: 11,063 million).

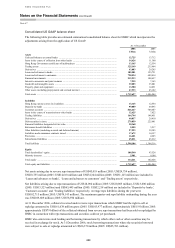

(j) Variable interest entities (‘VIEs’)

Nature, purpose and activities of VIEs with which HSBC is involved

HSBC uses VIE structures in the normal course of business in a variety of activities (outlined below), but

primarily to facilitate client needs. HSBC’s involvement in VIEs is, therefore, commercially driven. VIEs are

only used after careful consideration is given to the most appropriate structure to achieve HSBC’s objectives

from control, risk allocation, taxation and regulatory perspectives. The main VIEs are discussed below.

(i) Asset-backed conduits (‘ABCs’) and securitisation vehicles

ABCs and securitisation vehicles are structures in which interests in consumer and commercial receivables

are sold to investors. ABCs generally consist of entities which purchase assets from clients to meet their

financing needs, while securitisation vehicles generally acquire assets originated by HSBC itself and thereby

provide HSBC with a cost-effective source of financing. Under both structures, commercial paper, notes, or

equity interests are issued to investors to fund the purchase of receivables, and cash received from the

receivables is used to service the finance provided by the investors. In certain instances, HSBC receives fees

for providing liquidity facility commitments and for acting as administrator of the vehicle.

HSBC’s exposure to loss generally arises from commitments to provide back-up liquidity facilities for the

vehicles; interest-rate swaps in which HSBC is the counterparty; retained or acquired interests in the

receivables sold; or acquired interests in the vehicles themselves. In certain vehicles, the risk of loss to

HSBC is reduced by credit enhancements provided by the originator of the receivables or other parties.

In addition to these securitisation vehicles, HSBC (primarily through its North American subsidiaries)

securitises assets through entities that are not considered VIEs, including government-sponsored financing

vehicles and vehicles considered qualifying special-purpose entities under US GAAP. These entities are not

consolidated under US GAAP although certain of them are consolidated under IFRSs.

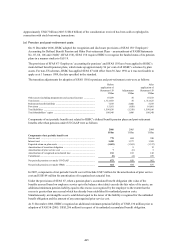

(ii) Infrastructure projects and funds

HSBC acts as an arranger for both public and private infrastructure projects and funds. The use of VIE

structures in such projects is common as a method of attracting a wider class of investor by dividing into

tranches the risk associated with such projects. HSBC’s exposure to loss generally arises from the provision

of subordinated or mezzanine debt finance to projects, either directly or through a consolidated investment

fund investing in infrastructure projects.

HSBC is deemed to be the primary beneficiary of an infrastructure project or fund when its investment in a

project’s equity, subordinated debt or mezzanine debt, or its interest in a fund, is at a level at which it

absorbs the majority of the expected losses or residual returns of the project or fund.