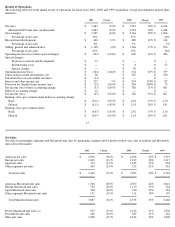

Apple 2001 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2001 Apple annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

|

|

assembled workforce may not be accounted for separately. SFAS No. 142 requires that goodwill and intangible assets with indefinite useful

lives no longer be amortized, but instead be tested for impairment at least annually in accordance with the provisions of SFAS No. 142. SFAS

No. 142 also requires that intangible assets with definite lives be amortized over their estimated useful lives and reviewed for impairment in

accordance with SFAS No. 144, "Accounting for the Impairment of Long-Lived Assets and for Long-Lived Assets to Be Disposed Of."

The Company is required to adopt the provisions of SFAS No. 141 immediately. The provisions of SFAS No. 142 are effective for fiscal years

beginning after December 15, 2001. However, early adoption by the Company is allowable effective in the first quarter of its fiscal 2002. Prior

to adoption of SFAS No. 142, any goodwill and any intangible asset determined to have an indefinite useful life acquired in a purchase

business combination completed after June 30, 2001, will not be amortized, but will continue to be evaluated for impairment in accordance

with pre-SFAS No. 142 accounting literature. Goodwill and intangible assets acquired in a purchase business combination completed prior to

July 1, 2001, will continue to be amortized prior to adoption of SFAS No. 142.

Adoption of SFAS No. 142 will require that the Company evaluate its existing intangible assets and goodwill that were acquired in a prior

purchase business combination, and make any necessary reclassifications in order to conform with the new criteria in SFAS No. 141 for

recognition apart from goodwill. Upon adoption of SFAS No. 142, the Company will be required to reassess the useful lives and residual

values of all intangible assets acquired in purchase business combinations, and make any necessary amortization period adjustments by the end

of the first interim period after adoption. In addition, to the extent an intangible asset is identified as having an indefinite useful life, the

Company will be required to test the intangible asset for impairment in accordance with the provisions of SFAS No. 142 within the first interim

period. Any impairment loss will be measured as of the date of adoption and recognized as the cumulative effect of a change in accounting

principle in the first interim period.

As of September 29, 2001, the Company has unamortized goodwill of approximately $65 million, and unamortized identifiable intangible

assets of approximately $11 million. The Company recognized amortization expense related to goodwill of approximately $16 million during

fiscal 2001, and amortization expense of $4 million related to identifiable intangible assets. These amounts for both unamortized intangibles

balances and quarterly amortization expense reflect accounting pursuant to existing accounting standards. Because of the extensive effort

needed to comply with adopting SFAS No. 141 and No. 142, it is not practicable to reasonably estimate the impact of adopting these standards

on the Company's financial results at the date of this report, including whether any reclassifications will be necessary in order to conform with

the new criteria for recognition of intangible assets apart from goodwill.

In June 2001, the Financial Accounting Standards Board issued SFAS No. 143, Accounting for Asset Retirement Obligations , which addresses

financial accounting and reporting for obligations associated with the retirement of tangible long-lived assets and the associated asset

retirement costs. The standard applies to legal obligations associated with the retirement of long-lived assets that result from the acquisition,

construction, development and (or) normal use of the asset. SFAS No. 143 requires that the fair value of a liability for an asset retirement

obligation be recognized in the period in which it is incurred if a reasonable estimate of fair value can be made. The fair value of the liability is

added to the carrying amount of the

23

associated asset and this additional carrying amount is depreciated over the life of the asset. The Company is required to adopt the provisions of

Statement No. 143 for the first quarter of its fiscal 2003. Because of the effort that may be necessary to comply with the adoption of Statement

No. 143, it is not practicable for management to estimate the impact of adopting this Statement at the date of this report.

In August 2001, the Financial Accounting Standards Board issued FASB Statement No. 144, Accounting for the Impairment or Disposal of

Long

-Lived Assets (Statement 144), which supersedes both FASB Statement No. 121, Accounting for the Impairment of Long-Lived Assets and

for Long

-Lived Assets to Be Disposed Of (Statement 121) and the accounting and reporting provisions of APB Opinion No. 30, Reporting the

Results of Operations

—Reporting the Effects of Disposal of a Segment of a Business, and Extraordinary, Unusual and Infrequently Occurring

Events and Transactions

(Opinion 30), for the disposal of a segment of a business (as previously defined in that Opinion). Statement 144

retains the fundamental provisions in Statement 121 for recognizing and measuring impairment losses on long-lived assets held for use and

long-lived assets to be disposed of by sale, while also resolving significant implementation issues associated with Statement 121. For example,

Statement 144 provides guidance on how a long-lived asset that is used as part of a group should be evaluated for impairment, establishes

criteria for when a long-lived asset is held for sale, and prescribes the accounting for a long-lived asset that will be disposed of other than by

sale. Statement 144 retains the basic provisions of Opinion 30 on how to present discontinued operations in the income statement but broadens

that presentation to include a component of an entity (rather than a segment of a business). Unlike Statement 121, an impairment assessment

under Statement 144 will never result in a write-down of goodwill. Rather, goodwill is evaluated for impairment under Statement No. 142,

Goodwill and Other Intangible Assets.

The Company is required to adopt Statement 144 no later than its first fiscal year beginning after December 15, 2001. Management does not

expect the adoption of Statement 144 for long-lived assets held for use to have a material impact on the Company's financial statements

because the impairment assessment under Statement 144 is largely unchanged from Statement 121. The provisions of the Statement for assets

held for sale or other disposal generally are required to be applied prospectively after the adoption date to newly initiated disposal activities.

Therefore, management cannot determine the potential effects that adoption of Statement 144 will have on the Company's financial statements.

Liquidity and Capital Resources