Apple 2001 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2001 Apple annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

|

|

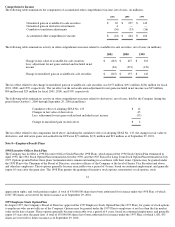

agreements to modify the interest rate profile of certain investments and debt. The Company's accounting policies for these instruments are

based on whether the instruments are designated as hedge or non-hedge instruments. The Company records all derivatives on the balance sheet

at fair value.

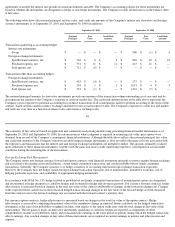

The following table shows the notional principal, net fair value, and credit risk amounts of the Company's interest rate derivative and foreign

currency instruments as of September 29, 2001 and September 30, 2000 (in millions).

The notional principal amounts for derivative instruments provide one measure of the transaction volume outstanding as of year-end, and do

not represent the amount of the Company's exposure to credit or market loss. The credit risk amount shown in the table above represents the

Company's gross exposure to potential accounting loss on these transactions if all counterparties failed to perform according to the terms of the

contract, based on then-current currency exchange and interest rates at each respective date. The Company's exposure to credit loss and market

risk will vary over time as a function of interest rates and currency exchange rates.

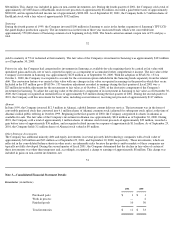

48

The estimates of fair value are based on applicable and commonly used pricing models using prevailing financial market information as of

September 29, 2001 and September 30, 2000. In certain instances where judgment is required in estimating fair value, price quotes were

obtained from several of the Company's counterparty financial institutions. Although the table above reflects the notional principal, fair value,

and credit risk amounts of the Company's interest rate and foreign exchange instruments, it does not reflect the gains or losses associated with

the exposures and transactions that the interest rate and foreign exchange instruments are intended to hedge. The amounts ultimately realized

upon settlement of these financial instruments, together with the gains and losses on the underlying exposures, will depend on actual market

conditions during the remaining life of the instruments.

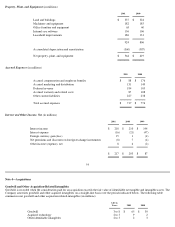

Foreign Exchange Risk Management

The Company enters into foreign currency forward and option contracts with financial institutions primarily to protect against foreign exchange

risk associated with existing assets and liabilities, certain firmly committed transactions and certain probable but not firmly committed

transactions. Generally, the Company's practice is to hedge a majority of its existing material foreign exchange transaction exposures.

However, the Company may not hedge certain foreign exchange transaction exposures due to immateriality, prohibitive economic cost of

hedging particular exposures, and availability of appropriate hedging instruments.

In accordance with SFAS No. 133, hedges related to probable but not firmly committed transactions of an anticipatory nature are designated

and documented at hedge inception as cash flow hedges and evaluated for hedge effectiveness quarterly. For currency forward contracts, hedge

effectiveness is measured based on changes in the total fair value of the contract attributable to changes in the forward exchange rate. Changes

in the expected future cash flows on the forecasted hedged transaction and changes in the fair value of the forward hedge are both measured

from the contract rate to the forward exchange rate associated with the forward contract's maturity date.

For currency option contracts, hedge effectiveness is measured based on changes in the total fair value of the option contract. Hedge

effectiveness is assessed by comparing the present value of the cumulative change in expected future cash flows on the hedged transaction

determined as the sum of the probability-weighted outcomes with respect to the option strike rates with the total change in fair value of the

option hedge. The net gains or losses on derivative instruments qualifying as cash flow hedges are reported as components of other

comprehensive income in stockholders' equity and reclassified into earnings in the same period or periods during which the hedged transaction

affects earnings. Any residual changes in fair value of these instruments are recognized in current earnings in interest and other income and

expense.

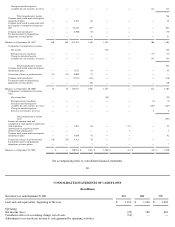

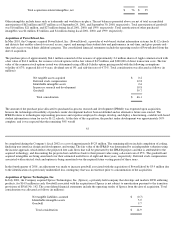

September 29, 2001

September 30, 2000

Notional

Principal

Fair

Value

Credit Risk

Amounts

Notional

Principal

Fair

Value

Credit Risk

Amounts

Transactions qualifying as accounting hedges:

Interest rate instruments:

Swaps

$

—

$

—

$

—

$

800

$

(1

)

$

4

Foreign exchange instruments:

Spot/Forward contracts, net

$

562

$

8

$

8

$

826

$

10

$

10

Purchased options, net

$

551

$

11

$

11

$

615

$

21

$

—

Sold options, net

$

712

$

(8

)

$

—

$

—

$

—

$

—

Transactions other than accounting hedges:

Foreign exchange instruments:

Spot/Forward contracts, net

$

455

$

(4

)

$

—

$

275

$

—

$

—

Purchased options, net

$

334

$

1

$

1

$

1,051

$

4

$

4

Sold options, net

$

354

$

(1

)

$

—

$

1,201

$

(5

)

$

—