Apple 2001 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2001 Apple annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

|

|

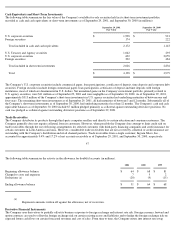

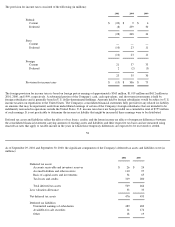

To protect gross margins from fluctuations in foreign currency exchange rates, the Company's U.S. dollar functional subsidiaries hedge a

portion of forecasted foreign currency revenues, and the Company's non-U.S. dollar functional subsidiaries selling in local currencies hedge a

portion of forecasted inventory purchases not denominated in the subsidiaries' functional currency. Other comprehensive income associated

with hedges of foreign currency revenues is recognized as a component of net sales in the same period as the related sales are recognized, and

other comprehensive income related to inventory purchases is recognized as a component of cost of sales in the same period as the related costs

are recognized. Typically, the Company hedges portions of its forecasted foreign currency exposure associated with revenues and inventory

purchases over a time horizon of 3 to 9 months.

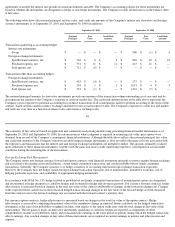

The Company also enters into foreign currency forward and option contracts to offset the foreign exchange gains and losses generated by the

remeasurement of certain recorded assets and liabilities in

49

non-functional currencies. Changes in the fair value of these derivatives are recognized in current earnings in interest and other income as

offsets to the changes in the fair value of the related assets or liabilities.

The Company may enter into foreign currency forward contracts to offset the translation and economic exposure of a net investment position in

a foreign subsidiary. Hedge effectiveness on forwards designated as net investment hedges is measured based on changes in the fair value of

the contract attributable to changes in the spot exchange rate. The effective portion of the net gain or loss on a derivative instrument designated

as a hedge of the net investment position in a foreign subsidiary is reported in the same manner as a foreign currency translation adjustment.

Any residual changes in fair value of the forward contract, including changes in fair value based on the differential between the spot and

forward exchange rates are recognized in current earnings in interest and other income and expense.

As discussed above, the Company enters into foreign currency option contracts as designated cash flow hedges and, sometimes, as items that

provide an offset to the remeasurement of certain recorded assets and liabilities denominated in non-functional currencies. All changes in the

fair value of these derivative contracts based on changes in option time value are recorded in current earnings in interest and other income and

expense. Due to market movements, changes in option time value can lead to increased volatility in other income and expense.

Derivative instruments designated as cash flow hedges must be de-designated as hedges when it is probable that the forecasted hedged

transaction will not occur in the initially identified time period or within a subsequent 60-day time period. Deferred gains and losses in other

comprehensive income associated with such derivative instruments are immediately reclassified into earnings in interest and other income, net.

Any subsequent changes in fair value of such derivative instruments are also reflected in current earnings unless they are re-designated as

hedges of other transactions. During the first quarter of fiscal 2001, the Company recorded a net gain of $5.1 million in interest and other

income, net related to the loss of hedge designation on discontinued cash flow hedges due to changes in the Company's forecast of future net

sales and cost of sales.

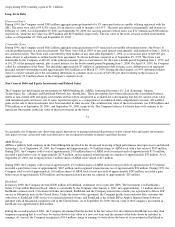

Interest Rate Risk Management

The Company sometimes enters into interest rate derivative transactions, including interest rate swaps, collars, and floors, with financial

institutions in order to better match the Company's floating-rate interest income on its cash equivalents and short-term investments with its

fixed-rate interest expense on its long-term debt, and/or to diversify a portion of the Company's exposure away from fluctuations in short-term

U.S. interest rates. The Company may also enter into interest rate contracts that are intended to reduce the cost of the interest rate risk

management program. The Company does not hold or transact in such financial instruments for purposes other than risk management.

As of September 30, 2000, the Company had entered into interest rate swaps with financial institutions in order to better match the Company's

floating-rate interest income on its cash equivalents and short-term investments with its fixed-rate interest expense on its long-

term debt, and/or

to diversify a portion of the Company's exposure away from fluctuations in short-term U.S. interest rates. The interest rate swaps generally

required the Company to pay a floating interest rate based on the three- or six-month U.S. dollar LIBOR and receive a fixed rate of interest

without exchanges of the underlying notional amounts. These swaps effectively converted the Company's fixed-rate 10 year debt to floating-

rate debt and convert a portion of the floating rate investments to fixed rate. The Company assumed no ineffectiveness with regard to the debt

interest swaps as each debt interest rate swap met the criteria for accounting under the short-cut method defined in SFAS No. 133 for fair value

hedges of debt instruments. Accordingly, no net

50

gains or losses were recorded in income relative to the Company's underlying debt interest rate swaps. During fiscal 2001, the Company closed

out all of its existing debt interest rate swap positions due to prevailing market interest rates realizing a gain of $17 million. This gain was

deferred, recognized in long-term debt and is being amortized to other income and expense over the remaining life of the debt.

The unrealized loss on these assets swaps as of September 30, 2000, of $5.7 million was deferred and then recognized in income in 2001 as

part of the SFAS No. 133 transition adjustment effective on October 1, 2000. The Company closed out all of its existing interest rate asset