Charter 2012 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2012 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

10

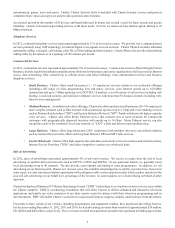

Markets

We operate in geographically diverse areas which are organized in regional clusters we call key market areas. These key market

areas are managed centrally on a consolidated level. Our eleven key market areas and the customer relationships within each

market as of December 31, 2012 are as follows (in thousands):

Key Market Area Total Customer

Relationships

California 565

Central States 573

Alabama/Georgia 605

Michigan 635

Minnesota/Nebraska 342

New England 351

Northwest 475

Carolinas 559

Tennessee/Louisiana 518

Texas 172

Wisconsin 565

Competition

We face competition for both residential and commercial customers in the areas of price, service offerings, and service reliability.

In our residential business, we compete with other providers of video, high-speed Internet access, telephone services, and other

sources of home entertainment. In our commercial business, we compete with other providers of video, high-speed Internet access

and related value-added services, fiber solutions, business telephony, and Ethernet services. We operate in a competitive business

environment, which can adversely affect the results of our business and operations. We cannot predict the impact on us of broadband

services offered by our competitors.

In terms of competition for customers, we view ourselves as a member of the broadband communications industry, which

encompasses multi-channel video for television and related broadband services, such as high-speed Internet, telephone, and other

interactive video services. In the broadband communications industry, our principal competitors for video services are direct

broadcast satellite (“DBS”) and telephone companies that offer video services. Our principal competitors for high-speed Internet

services are the broadband services provided by telephone companies, including both traditional DSL, fiber-to-the-node, and fiber-

to-the-home offerings. Our principal competitors for telephone services are established telephone companies, other telephone

service providers, and other carriers, including VoIP providers. At this time, we do not consider other cable operators to be

significant competitors in our overall market, as overbuilds are infrequent and geographically spotty (although in any particular

market, a cable operator overbuilder would likely be a significant competitor at the local level). We could, however, face additional

competition from multi-channel video providers if they began distributing video over the Internet to customers residing outside

their current territories.

Our key competitors include:

DBS

Direct broadcast satellite is a significant competitor to cable systems. The two largest DBS providers now serve more than 34

million subscribers nationwide. DBS service allows the subscriber to receive video services directly via satellite using a dish

antenna.

Video compression technology and high powered satellites allow DBS providers to offer more than 280 digital channels, thereby

surpassing the traditional analog cable system. In 2012, major DBS competitors offered a greater variety of channel packages,

and were especially competitive with promotional pricing for more basic services. While we continue to believe that the initial

investment by a DBS customer exceeds that of a cable customer, the initial equipment cost for DBS has decreased substantially,

as the DBS providers have aggressively marketed offers to new customers of incentives for discounted or free equipment,

installation, and multiple units. DBS providers are able to offer service nationwide and are able to establish a national image and