Charter 2012 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2012 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

55

Cross Acceleration

The indentures of CCO Holdings include various events of default, including cross acceleration provisions. Under these provisions,

a failure by the note issuer or any of its restricted subsidiaries to pay at the final maturity thereof the principal amount of other

indebtedness having a principal amount of $100 million or more (or any other default under any such indebtedness resulting in

its acceleration) would result in an event of default under the indenture governing the applicable notes. As a result, an event of

default related to the failure to repay principal at maturity or the acceleration of the indebtedness under the CCO Holdings notes,

CCO Holdings credit facility or the Charter Operating credit facilities could cause cross-defaults under all of CCO Holdings'

indentures.

Recently Issued Accounting Standards

In July 2012, the FASB issued ASU 2012-02, Intangibles - Goodwill and Other (Topic 350): Testing Indefinite-Lived Intangible

Assets for Impairment ("ASU 2012-02"). ASU 2012-02 permits an entity to make a qualitative assessment to determine whether

it is more likely than not that an indefinite-lived intangible asset, other than goodwill, is impaired. This standard is effective for

annual and interim impairment tests performed for fiscal years beginning after September 15, 2012. Early adoption is permitted.

We adopted ASU 2012-02 with our 2012 annual impairment testing. The adoption of ASU 2012-02 did not have a material impact

on our consolidated financial statements.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk.

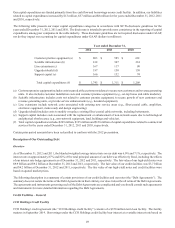

We are exposed to various market risks, including fluctuations in interest rates. We have used interest rate swap agreements to

manage our interest costs and reduce our exposure to increases in floating interest rates. We manage our exposure to fluctuations

in interest rates by maintaining a mix of fixed and variable rate debt. Using interest rate swap agreements, we agree to exchange,

at specified intervals through 2017, the difference between fixed and variable interest amounts calculated by reference to agreed-

upon notional principal amounts.

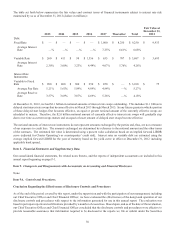

As of December 31, 2012 and 2011, the accreted value of our debt was approximately $12.8 billion and $12.9 billion, respectively.

As of December 31, 2012 and 2011, the weighted average interest rate on the credit facility debt, including the effects of our

interest rate swap agreements, was approximately 4.2% and 4.3%, respectively, and the weighted average interest rate on the high-

yield notes was approximately 6.7% and 8.5%, respectively, resulting in a blended weighted average interest rate of 6.0% and

7.1%, respectively. The interest rate on approximately 87% and 82% of the total principal amount of our debt was effectively

fixed, including the effects of our interest rate swap agreements, as of December 31, 2012 and 2011, respectively.

We do not hold or issue derivative instruments for speculative trading purposes. We have interest rate derivative instruments that

have been designated as cash flow hedging instruments. Such instruments effectively convert variable interest payments on certain

debt instruments into fixed payments. For qualifying hedges, realized derivative gains and losses offset related results on hedged

items in the consolidated statements of operations. We formally document, designate and assess the effectiveness of transactions

that receive hedge accounting. For each of the years ended December 31, 2012, 2011 and 2010, there was no cash flow hedge

ineffectiveness on interest rate swap agreements.

Changes in the fair value of interest rate agreements that are designated as hedging instruments of the variability of cash flows

associated with floating-rate debt obligations, and that meet effectiveness criteria are reported in other comprehensive loss. For

the years ended December 31, 2012, 2011 and 2010, losses of $10 million, $8 million and $57 million, respectively, related to

derivative instruments designated as cash flow hedges, were recorded in other comprehensive loss. The amounts are subsequently

reclassified as an increase or decrease to interest expense in the same periods in which the related interest on the floating-rate debt

obligations affects earnings (losses).