Lowe's 2014 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2014 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

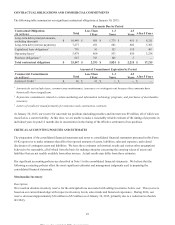

|

|

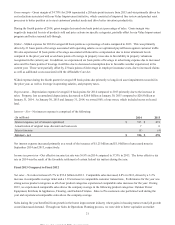

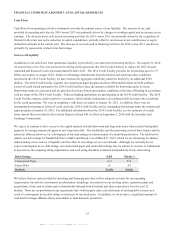

Store Closing Lease Obligations

Description

When locations under operating leases are closed, we recognize a liability for the fair value of future contractual obligations

associated with the leased location. The fair value of the store closing lease obligation is determined using an expected present

value cash flow model incorporating future minimum lease payments, property taxes, utilities, common area maintenance and

other ongoing expenses, net of estimated sublease income and other recoverable items, discounted at a credit-adjusted risk free

rate. The expected present value cash flow model uses a probability weighted scenario approach that assigns varying cash

flows to certain scenarios based on the expected likelihood of outcomes. Estimating the fair value involves making

assumptions regarding estimated sublease income by obtaining information from property brokers or appraisers in the specific

markets being evaluated. The information includes comparable lease rates of similar assets and assumptions about demand in

the market for leasing these assets. Subsequent changes to the liability, including a change resulting from a revision to either

the timing or the amount of estimated cash flows, are recognized in the period of the change.

Judgments and uncertainties involved in the estimate

Our store closing lease liability calculations require us to apply judgment in estimating expected future cash flows, primarily

related to estimated sublease income, and the selection of an appropriate discount rate.

Effect if actual results differ from assumptions

During 2014, the Company did not close or relocate any stores subject to operating leases. During 2013, the Company

relocated two stores subject to operating leases. Expenses for store closing lease obligations included $12 million and $6

million in 2014 and 2013, respectively, related to adjustments for previously closed or relocated locations.

We have not made any material changes in the methodology used to estimate the expected future cash flows of closed locations

under operating leases during the past three fiscal years. If the actual results are not consistent with the assumptions and

judgments we have made in estimating expected future cash flows, our store closing lease obligation losses could vary

positively or negatively from our estimated losses. A 10% change in the store closing lease liability would have affected net

earnings by approximately $3 million for 2014.

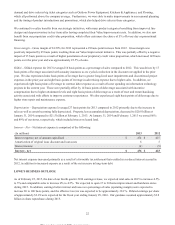

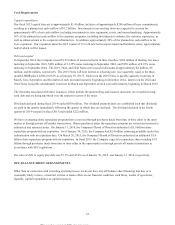

Self-Insurance

Description

We are self-insured for certain losses relating to workers’ compensation; automobile; general and product liability; extended

protection plan; and certain medical and dental claims. Our self-insured retention or deductible, as applicable, is limited to $2

million per occurrence involving workers’ compensation, $5 million per occurrence involving general or product liability, and

$10 million per occurrence involving automobile. We do not have any insurance coverage for self-insured extended protection

plan or medical and dental claims. Self-insurance claims filed and claims incurred but not reported are accrued based upon our

estimates of the discounted ultimate cost for self-insured claims incurred using actuarial assumptions followed in the insurance

industry and historical experience. During 2014, our self-insurance liability increased approximately $1 million to $905

million as of January 30, 2015.

Judgments and uncertainties involved in the estimate

These estimates are subject to changes in the regulatory environment; utilized discount rate; projected exposures including

payroll, sales and vehicle units; as well as the frequency, lag and severity of claims.

Effect if actual results differ from assumptions

We have not made any material changes in the methodology used to establish our self-insurance liability during the past three

fiscal years. Although we believe that we have the ability to reasonably estimate losses related to claims, it is possible that

actual results could differ from recorded self-insurance liabilities. A 10% change in our self-insurance liability would have

28

This proof is printed at 96% of original size

This line represents final trim and will not print