Lowe's 2014 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2014 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

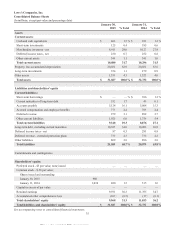

|

|

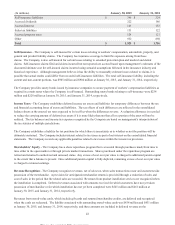

(In millions) January 30, 2015 January 31, 2014

Self-insurance liabilities $ 346 $ 324

Accrued dividends 222 186

Accrued interest 165 153

Sales tax liabilities 131 122

Accrued property taxes 124 121

Other 932 850

Tot al $ 1,920 $ 1,756

Self-Insurance - The Company is self-insured for certain losses relating to workers’ compensation, automobile, property, and

general and product liability claims. The Company has insurance coverage to limit the exposure arising from these

claims. The Company is also self-insured for certain losses relating to extended protection plan and medical and dental

claims. Self-insurance claims filed and claims incurred but not reported are accrued based upon management’s estimates of the

discounted ultimate cost for self-insured claims incurred using actuarial assumptions followed in the insurance industry and

historical experience. Although management believes it has the ability to reasonably estimate losses related to claims, it is

possible that actual results could differ from recorded self-insurance liabilities. The total self-insurance liability, including the

current and non-current portions, was $905 million and $904 million at January 30, 2015, and January 31, 2014, respectively.

The Company provides surety bonds issued by insurance companies to secure payment of workers’ compensation liabilities as

required in certain states where the Company is self-insured. Outstanding surety bonds relating to self-insurance were $234

million and $228 million at January 30, 2015, and January 31, 2014, respectively.

Income Taxes - The Company establishes deferred income tax assets and liabilities for temporary differences between the tax

and financial accounting bases of assets and liabilities. The tax effects of such differences are reflected in the consolidated

balance sheets at the enacted tax rates expected to be in effect when the differences reverse. A valuation allowance is recorded

to reduce the carrying amount of deferred tax assets if it is more likely than not that all or a portion of the asset will not be

realized. The tax balances and income tax expense recognized by the Company are based on management’s interpretation of

the tax statutes of multiple jurisdictions.

The Company establishes a liability for tax positions for which there is uncertainty as to whether or not the position will be

ultimately sustained. The Company includes interest related to tax issues as part of net interest on the consolidated financial

statements. The Company records any applicable penalties related to tax issues within the income tax provision.

Shareholders' Equity - The Company has a share repurchase program that is executed through purchases made from time to

time either in the open market or through private market transactions. Shares purchased under the repurchase program are

retired and returned to authorized and unissued status. Any excess of cost over par value is charged to additional paid-in capital

to the extent that a balance is present. Once additional paid-in capital is fully depleted, remaining excess of cost over par value

is charged to retained earnings.

Revenue Recognition - The Company recognizes revenues, net of sales tax, when sales transactions occur and customers take

possession of the merchandise. A provision for anticipated merchandise returns is provided through a reduction of sales and

cost of sales in the period that the related sales are recorded. Revenues from product installation services are recognized when

the installation is completed. Deferred revenues associated with amounts received for which customers have not yet taken

possession of merchandise or for which installation has not yet been completed were $545 million and $461 million at

January 30, 2015, and January 31, 2014, respectively.

Revenues from stored-value cards, which include gift cards and returned merchandise credits, are deferred and recognized

when the cards are redeemed. The liability associated with outstanding stored-value cards was $434 million and $431 million

at January 30, 2015, and January 31, 2014, respectively, and these amounts are included in deferred revenue on the

42

This proof is printed at 96% of original size

This line represents final trim and will not print