McDonalds 2009 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2009 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

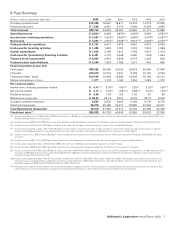

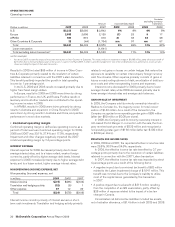

from operations was invested in our business primarily to open

868 restaurants (511 net, after 357 closings) and reimage about

1,850 existing locations. After these capital expenditures, we

returned our free cash flow to shareholders through dividends

and share repurchases. In 2009, we returned $5.1 billion consist-

ing of $2.2 billion in dividends and $2.9 billion in share

repurchases. This brought the total return to shareholders to

$16.6 billion under our $15 billion to $17 billion target for 2007

through 2009.

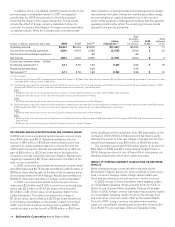

Cash from operations continues to benefit from our evolution

toward a more heavily franchised business model as the rent and

royalty income received from owner/operators is a very stable

revenue stream that has relatively low costs, and is less capital-

intensive. In addition, we believe locally-owned and operated

restaurants help us maximize brand performance and are at the

core of our competitive advantage, making McDonald’s not just a

global brand but also a locally-relevant one. To that end, for 2008

and 2009 combined, we refranchised about 1,100 restaurants,

increasing the percent of restaurants franchised worldwide to

81%. Refranchising impacts our consolidated financial state-

ments as follows:

• Consolidated revenues are initially reduced because we collect

rent and royalty as a percent of sales from a refranchised res-

taurant instead of 100% of its sales.

• Company-operated margin dollars decline while franchised

margin dollars increase.

• Margin percentages are affected depending on the sales and

cost structures of the restaurants refranchised.

• Other operating (income) expense fluctuates as we recognize

gains and/or losses resulting from sales of restaurants.

• Combined operating margin percent improves.

• Return on average assets increases primarily due to a

decrease in average asset balances.

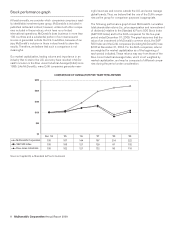

HIGHLIGHTS FROM THE YEAR INCLUDED:

• Comparable sales grew 3.8% and guest counts rose 1.4%,

building on 2008 increases of 6.9% and 3.1%, respectively.

• Growth in combined operating margin of 2.7 percentage points

from 27.4% in 2008 to 30.1% in 2009.

• Operating income increased 6% (10% in constant currencies).

• Net income per share was $4.11, an increase of 9% (13% in

constant currencies).

• Cash provided by operations totaled $5.8 billion.

• The Company increased the quarterly cash dividend per share

10% to $0.55 for the fourth quarter–bringing the current

annual dividend rate to $2.20 per share.

• One-year ROIIC was 38.0% and three-year ROIIC was 42.9%

for the period ended December 31, 2009.

OUTLOOK FOR 2010

We will continue to drive success in 2010 and beyond by remain-

ing focused on our “better, not just bigger” strategy and the key

drivers of exceptional customer experiences—People, Products,

Place, Price and Promotion. Our global System is energized by

our ongoing momentum, strong competitive position and growth

opportunities.

We intend to further differentiate our brand, increase

customer visits and grow market share by pursuing initiatives in

three key areas: service enhancement, restaurant reimaging and

menu innovation. These efforts will include leveraging technology

to make it easier for restaurant staff to quickly and accurately

serve customers, accelerating our interior and exterior reimaging

efforts and innovating at every tier of our menu to deliver great

taste and value to customers. As we execute along these prior-

ities and remain disciplined in operations and financial

management, we expect to increase McDonald’s brand relevance,

widen our competitive lead and, in turn, grow sales, profits and

returns. As we do so, we are confident we can meet or exceed

the long-term constant currency financial targets previously dis-

cussed despite expectations for a continued challenging global

economic environment in 2010.

In the U.S., our strategies include strengthening our core

menu and value offerings, aggressively pursuing new growth

opportunities in chicken, breakfast, beverages and snacking

options, and elevating the brand experience. Our initiatives

include highlighting the enduring appeal of core menu classics

such as the Big Mac, emphasizing the value our menu offers

all-day-long including the new breakfast value menu, and

encouraging the trial of new products with the Mac Snack Wrap

and—by mid-year—frappés and smoothies. In addition, our plans

to elevate the brand experience encompass updating our

technology with a new point of sale system, enhancing restaurant

manager and crew retention and productivity, and initiating a

multi-year program to contemporize the interiors and exteriors of

our restaurants through reimaging, completing about 500 in

2010. These efforts combined with the convenience of our loca-

tions, optimized drive-thru service, free wireless service and

longer operating hours will further reinforce McDonald’s position

as an easy, enjoyable eating-out experience.

Our plans for Europe are focused on building market share as

we continue to execute along Europe’s three key priorities. This

includes upgrading our restaurant ambiance by reimaging

approximately 1,000 restaurants, primarily in France and the U.K.,

as we make progress toward our goal to reimage more than 85%

of our restaurants by the end of 2011. In addition, we expect to

leverage technologies such as self-order kiosks, hand-held order

devices and drive-thru customer order displays to enhance the

customer experience and help speed service. We will further

enhance our local relevance by complementing our tiered-menu

with limited-time food events as well as new snack and dessert

options. Finally, we will remain approachable and accessible as

we continue to educate consumers about the quality and origin of

our food and communicate our sustainable business practices.

In APMEA, we will execute initiatives that best support our

goal to be customers’ first choice for eating out: convenience,

core menu, branded affordability, improved operations and

reimaging. Our convenience initiatives include leveraging the

success of 24-hour or extended operating hours, expanding

delivery service and building drive-thru traffic. At the same time,

we will continue to elevate the role of our classic core and break-

fast menus, complementing both with locally-relevant food news.

We will maximize the impact of our everyday affordability plat-

forms with mid-tier and value lunch programs and intensify our

focus on operations to drive efficiencies. In addition, we will

accelerate our reimaging efforts using a set of standard interior

and exterior designs. Finally, given its size and long-term

McDonald’s Corporation Annual Report 2009 11