McDonalds 2009 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2009 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

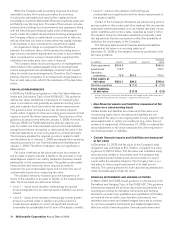

plan to dispose of the assets, the assets are available for dis-

posal, the disposal is probable of occurring within 12 months, and

the net sales proceeds are expected to be less than the assets’

net book value, among other factors. An impairment charge is

recognized for the difference between the net book value of the

business (including foreign currency translation adjustments

recorded in accumulated other comprehensive income in share-

holders’ equity) and the estimated cash sales price, less costs of

disposal.

An alternative accounting policy would be to recharacterize

some or all of any loss as an intangible asset and amortize it to

expense over future periods based on the term of the relevant

licensing arrangement and as revenue is recognized for royalties

and initial fees. Under this alternative for the 2007 Latam trans-

action, approximately $900 million of the $1.7 billion impairment

charge could have been recharacterized as an intangible asset

and amortized over the franchise term of 20 years, resulting in

about $45 million of expense annually. This policy would be

based on a view that the consideration for the sale consists of

two components–the cash sales price and the future royalties

and initial fees.

The Company bases its accounting policy on management’s

determination that royalties payable under its developmental

license arrangements are substantially consistent with market

rates for similar license arrangements. The Company does not

believe it would be appropriate to recognize an asset for the right

to receive market-based fees in future periods, particularly given

the continuing support and services provided to the licensees.

Therefore, the Company believes that the recognition of an

impairment charge based on the net cash sales price reflects the

substance of the sale transaction.

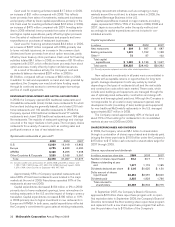

• Litigation accruals

From time to time, the Company is subject to proceedings, law-

suits and other claims related to competitors, customers,

employees, franchisees, government agencies, intellectual prop-

erty, shareholders and suppliers. The Company is required to

assess the likelihood of any adverse judgments or outcomes to

these matters as well as potential ranges of probable losses. A

determination of the amount of accrual required, if any, for these

contingencies is made after careful analysis of each matter. The

required accrual may change in the future due to new develop-

ments in each matter or changes in approach such as a change

in settlement strategy in dealing with these matters. The Com-

pany does not believe that any such matter currently being

reviewed will have a material adverse effect on its financial con-

dition or results of operations.

• Income taxes

The Company records a valuation allowance to reduce its

deferred tax assets if it is more likely than not that some portion

or all of the deferred assets will not be realized. While the Com-

pany has considered future taxable income and ongoing prudent

and feasible tax strategies, including the sale of appreciated

assets, in assessing the need for the valuation allowance, if these

estimates and assumptions change in the future, the Company

may be required to adjust its valuation allowance. This could

result in a charge to, or an increase in, income in the period such

determination is made.

In addition, the Company operates within multiple taxing juris-

dictions and is subject to audit in these jurisdictions. The

Company records accruals for the estimated outcomes of these

audits, and the accruals may change in the future due to new

developments in each matter. During 2008, the IRS examination

of the Company’s 2005-2006 U.S. tax returns was completed.

The tax provision impact associated with the completion of this

examination was not significant. During 2007, the Company

recorded a $316 million benefit as a result of the completion of

an IRS examination of the Company’s 2003-2004 U.S. tax

returns. The Company’s 2007-2008 U.S. tax returns are currently

under examination and the completion of the examination is

expected in 2010.

Deferred U.S. income taxes have not been recorded for

temporary differences totaling $9.2 billion related to investments

in certain foreign subsidiaries and corporate affiliates. The

temporary differences consist primarily of undistributed earnings

that are considered permanently invested in operations outside

the U.S. If management’s intentions change in the future,

deferred taxes may need to be provided.

EFFECTS OF CHANGING PRICES—INFLATION

The Company has demonstrated an ability to manage inflationary

cost increases effectively. This is because of rapid inventory

turnover, the ability to adjust menu prices, cost controls and sub-

stantial property holdings, many of which are at fixed costs and

partly financed by debt made less expensive by inflation.

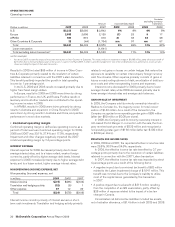

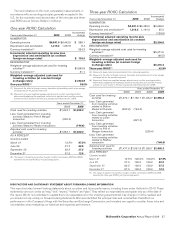

RECONCILIATION OF RETURNS ON INCREMENTAL INVESTED

CAPITAL

Return on incremental invested capital (ROIIC) is a measure

reviewed by management over one-year and three-year time

periods to evaluate the overall profitability of the business units,

the effectiveness of capital deployed and the future allocation of

capital. This measure is calculated using operating income and

constant foreign exchange rates to exclude the impact of foreign

currency translation. The numerator is the Company’s incremental

operating income plus depreciation and amortization from the

base period.

The denominator is the weighted-average adjusted cash used

for investing activities during the applicable one- or three-year

period. Adjusted cash used for investing activities is defined as

cash used for investing activities less cash generated from inves-

ting activities related to the Boston Market, Chipotle, Latam, Pret

A Manger and Redbox transactions. The weighted-average

adjusted cash used for investing activities is based on a weight-

ing applied on a quarterly basis. These weightings are used to

reflect the estimated contribution of each quarter’s investing

activities to incremental operating income. For example, fourth

quarter 2009 investing activities are weighted less because the

assets purchased have only recently been deployed and would

have generated little incremental operating income (12.5% of

fourth quarter 2009 investing activities are included in the

one-year and three-year calculations). In contrast, fourth quarter

2008 is heavily weighted because the assets purchased were

deployed more than 12 months ago, and therefore have a full

year impact on 2009 operating income, with little or no impact to

the base period (87.5% and 100.0% of fourth quarter 2008

investing activities are included in the one-year and three-year

calculations, respectively). Management believes that weighting

cash used for investing activities provides a more accurate

reflection of the relationship between its investments and returns

than a simple average.

26 McDonald’s Corporation Annual Report 2009