McDonalds 2009 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2009 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

outstanding common stock with no specified expiration date. In

2009, approximately 50 million shares were repurchased for

$2.9 billion, of which 8 million shares or $0.5 billion were pur-

chased under the new program. The Company reduced its shares

outstanding at year end by over 3% compared with 2008, net of

stock option exercises.

The Company has paid dividends on its common stock for

34 consecutive years and has increased the dividend amount

every year. The 2009 full year dividend of $2.05 per share

reflects the quarterly dividend paid for each of the first three

quarters of $0.50 per share, with an increase to $0.55 per share

paid in the fourth quarter. This 10% increase in the quarterly

dividend equates to a $2.20 per share annual dividend rate and

reflects the Company’s confidence in the ongoing strength and

reliability of its cash flow. As in the past, future dividend amounts

will be considered after reviewing profitability expectations and

financing needs, and will be declared at the discretion of the

Company’s Board of Directors.

Financial Position and Capital Resources

TOTAL ASSETS AND RETURNS

Total assets increased $1.8 billion or 6% in 2009. Excluding the

effect of changes in foreign currency exchange rates, total

assets increased $677 million in 2009. Over 70% of total assets

were in major markets at year-end 2009. Net property and

equipment increased $1.3 billion in 2009 and represented over

70% of total assets at year end. Excluding the effect of changes

in foreign currency exchange rates, net property and equipment

increased $476 million primarily due to capital expenditures,

partly offset by depreciation, the impact of refranchising and

asset retirements related to reimaging.

Operating income is used to compute return on average

assets, while income from continuing operations is used to calcu-

late return on average common equity. Month-end balances are

used to compute both average assets and average common

equity. Assets of discontinued operations are excluded from

average assets since operating income excludes results from

discontinued operations.

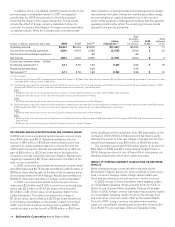

Returns on assets and equity

2009 2008 2007

Return on average assets 23.4% 21.8% 13.2%

Return on average common equity 34.0 30.6 15.1

In 2009, 2008 and 2007, return on average assets and

return on average common equity both benefited from strong

global operating results. During 2010, the Company will continue

to concentrate restaurant openings and invest new capital in

markets with acceptable returns or opportunities for long-term

growth.

In 2009, impairment and other charges (credits), net bene-

fited return on average assets and return on average common

equity by 0.2 percentage points and 0.7 percentage points,

respectively.

In 2007, impairment and other charges (credits), net reduced

return on average assets by 5.4 percentage points. Impairment

and other charges (credits), net partly offset by the 2007 net tax

benefit resulting from the completion of an IRS examination,

reduced return on average common equity by 8.5 percentage

points in 2007.

Operating income, as reported, does not include interest

income; however, cash balances are included in average assets.

The inclusion of cash balances in average assets reduced return

on average assets by 2.0 percentage points, 1.9 percentage

points and 1.3 percentage points in 2009, 2008 and 2007,

respectively.

FINANCING AND MARKET RISK

The Company generally borrows on a long-term basis and is

exposed to the impact of interest rate changes and foreign cur-

rency fluctuations. Debt obligations at December 31, 2009

totaled $10.6 billion, compared with $10.2 billion at

December 31, 2008. The net increase in 2009 was primarily due

to net issuances of $219 million and changes in exchange rates

on foreign currency denominated debt of $128 million.

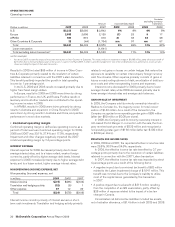

Debt highlights(1)

2009 2008 2007

Fixed-rate debt as a percent of total

debt(2,3) 68% 72% 58%

Weighted-average annual interest

rate of total debt(3) 4.5 5.0 4.7

Foreign currency-denominated debt

as a percent of total debt(2) 43 45 66

Total debt as a percent of total

capitalization (total debt and total

shareholders’ equity)(2) 43 43 38

Cash provided by operations as a

percent of total debt(2) 55 59 53

(1) All percentages are as of December 31, except for the weighted-average annual

interest rate, which is for the year.

(2) Based on debt obligations before the effect of fair value hedging adjustments. This

effect is excluded as these adjustments have no impact on the obligation at maturity.

See Debt financing note to the consolidated financial statements.

(3) Includes the effect of interest rate exchange agreements.

Fitch, Standard & Poor’s and Moody’s currently rate, with a

stable outlook, the Company’s commercial paper F1, A-1 and

P-2, respectively; and its long-term debt A, A and A3,

respectively. The Company’s key metrics for monitoring its credit

structure are shown in the preceding table. While the Company

targets these metrics for ease of focus, it also considers similar

credit ratios that incorporate capitalized operating leases to esti-

mate total adjusted debt. Total adjusted debt, a term that is

commonly used by the rating agencies referred to above,

includes debt outstanding on the Company’s balance sheet plus

an adjustment to capitalize operating leases. Based on their most

recent calculations, these agencies add between $6 billion and

$12 billion to debt for lease capitalization purposes, which

increases total debt as a percent of total capitalization and

reduces cash provided by operations as a percent of total debt

for credit rating purposes. The Company believes the rating

agency methodology for capitalizing leases requires certain

adjustments. These adjustments include: excluding percent rents

in excess of minimum rents; excluding certain Company-operated

restaurant lease agreements outside the U.S. that are cancelable

with minimal penalties (representing approximately 30% of

Company-operated restaurant minimum rents outside the U.S.,

based on the Company’s estimate); capitalizing non-restaurant

leases using a multiple of three times rent expense; and reducing

total rent expense by a percentage of the annual minimum rent

McDonald’s Corporation Annual Report 2009 23