McDonalds 2009 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2009 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

When the Company sells an existing business to a devel-

opmental licensee, the licensee purchases the business,

including the real estate, and uses his/her capital and local

knowledge to build the McDonald’s Brand and optimize sales and

profitability over the long term. The sale of the business includes

primarily land, buildings and improvements, and equipment, along

with the franchising and leasing rights under existing agree-

ments. Under the related developmental licensing arrangement,

the Company collects a royalty based on a percent of sales, as

well as initial fees, but does not have either any capital invested

in the business or any commitment to invest future capital.

An impairment charge is recognized for the difference

between the net book value of the business (including any for-

eign currency translation adjustments recorded in accumulated

other comprehensive income in shareholders’ equity) and the

estimated cash sales price, less costs of disposal.

The Company bases its accounting policy on management’s

determination that royalties payable under its developmental

license arrangements are substantially consistent with market

rates for similar license arrangements. Therefore, the Company

believes that the recognition of an impairment charge based on

the net cash sales price reflects the substance of the sale trans-

action.

FAIR VALUE MEASUREMENTS

In 2006, the FASB issued guidance in the Fair Value Measure-

ments and Disclosures Topic of the FASB ASC. This guidance

defines fair value, establishes a framework for measuring fair

value in accordance with generally accepted accounting princi-

ples, and expands disclosures about fair value measurements.

This guidance does not require any new fair value measure-

ments; rather, it applies to other accounting pronouncements that

require or permit fair value measurements. The provisions of the

guidance, as issued, were effective January 1, 2008. However, in

February 2008, the FASB deferred the effective date for one

year for certain non-financial assets and non-financial liabilities,

except those that are recognized or disclosed at fair value in the

financial statements on a recurring basis (i.e., at least annually).

The Company adopted the required provisions related to debt

and derivatives as of January 1, 2008 and adopted the remaining

required provisions for non-financial assets and liabilities as of

January 1, 2009. The effect of adoption was not significant in

either period.

Fair value is defined as the price that would be received to

sell an asset or paid to transfer a liability in the principal or most

advantageous market in an orderly transaction between market

participants on the measurement date. The guidance also estab-

lishes a three-level hierarchy, which requires an entity to

maximize the use of observable inputs and minimize the use of

unobservable inputs when measuring fair value.

The valuation hierarchy is based upon the transparency of

inputs to the valuation of an asset or liability on the measurement

date. The three levels are defined as follows:

• Level 1 – inputs to the valuation methodology are quoted

prices (unadjusted) for an identical asset or liability in an active

market.

• Level 2 – inputs to the valuation methodology include quoted

prices for a similar asset or liability in an active market or

model-derived valuations in which all significant inputs are

observable for substantially the full term of the asset or liability.

• Level 3 – inputs to the valuation methodology are

unobservable and significant to the fair value measurement of

the asset or liability.

Certain of the Company’s derivatives are valued using various

pricing models or discounted cash flow analyses that incorporate

observable market parameters, such as interest rate yield curves,

option volatilities and currency rates, classified as Level 2 within

the valuation hierarchy. Derivative valuations incorporate credit

risk adjustments that are necessary to reflect the probability of

default by the counterparty or the Company.

The following table presents financial assets and liabilities

measured at fair value on a recurring basis as of

December 31, 2009 by the valuation hierarchy as defined in the

fair value guidance:

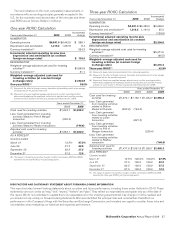

In millions Level 1 Level 2 Level 3 Carrying

value

Cash equivalents $455.8 $455.8

Investments 115.7* 115.7

Derivative

receivables 79.6* $94.5 174.1

Total assets at

fair value $651.1 $94.5 $745.6

Derivative payables $ (7.0) $ (7.0)

Total liabilities

at fair value $ (7.0) $ (7.0)

* Includes long-term investments and derivatives that hedge market driven changes in

liabilities associated with the Company’s supplemental benefit plans.

• Non-financial assets and liabilities measured at fair

value on a nonrecurring basis

Certain assets and liabilities are measured at fair value on a

nonrecurring basis; that is, the assets and liabilities are not

measured at fair value on an ongoing basis but are subject to fair

value adjustments in certain circumstances (e.g., when there is

evidence of impairment). At December 31, 2009, no material fair

value adjustments or fair value measurements were required for

non-financial assets or liabilities.

• Certain financial assets and liabilities not measured

at fair value

At December 31, 2009, the fair value of the Company’s debt

obligations was estimated at $11.3 billion, compared to a carry-

ing amount of $10.6 billion. This fair value was estimated using

various pricing models or discounted cash flow analyses that

incorporated quoted market prices and are similar to Level 2

inputs within the valuation hierarchy. The Company has no cur-

rent plans to retire a significant amount of its debt prior to

maturity. The carrying amount for both cash and equivalents and

notes receivable approximate fair value.

FINANCIAL INSTRUMENTS AND HEDGING ACTIVITIES

In March 2008, the FASB issued guidance on disclosures in the

Derivatives and Hedging Topic of the FASB ASC. This guidance

amends and expands the previous disclosure requirements sur-

rounding accounting for derivative instruments and hedging

activities to provide more qualitative and quantitative information

on how and why an entity uses derivative instruments, how

derivative instruments and related hedged items are accounted

for, and how derivative instruments and related hedged items

affect an entity’s financial position, financial performance and

34 McDonald’s Corporation Annual Report 2009