Proctor and Gamble 2009 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2009 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

|

|

Management’s Discussion and Analysis The Procter & Gamble Company 39

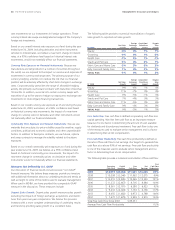

GROOMING

($ millions) 2009

Change vs.

Prior Year 2008

Change vs.

Prior Year

Volume n/a -6% n/a +5%

Net sales $7,543 -9% $8,254 +11%

Net earnings $1,492 -11% $1,679 +21%

Grooming net sales declined 9% in 2009 to $7.5billion on a 6%

decline in unit volume. Unfavorable foreign exchange reduced net

sales by 6%. Product mix had a negative 2% impact on net sales as

favorable product mix from growth of the premium-priced Gillette

Fusion brand was more than offset by a disproportionate decline of

Braun, both of which have higher than segment average selling

prices. Price increases, taken across most product lines and in part to

offset foreign exchange impacts in developing regions, added 5% to

net sales. Organic sales were down 2% versus the prior year on a 5%

decline in organic volume, mainly due to the sharp decline of the

Braun business. Volume in developed regions declined high single

digits and volume in developing regions declined mid-single digits.

Blades and Razors volume declined low single digits primarily driven

by market contractions in developed regions and trade inventory

reductions. Growth of Gillette Fusion and Venus was morethan offset

by declines in legacy shaving systems. Global value share of blades

and razors was up less than half a point versus the prior year. Volume

in Braun was down double digits due to market contractions, trade

inventory reductions and the exits of the U.S. home appliance and

Tassimo coffee appliance businesses. Global value share of the female

dry shaving market was up more than a point, while global value share

of the male dry shaving market was down less than half a point.

Net earnings were down 11% in 2009 to $1.5billion primarily on the

decline in net sales and a 60-basis point reduction in net earnings

margin. Net earnings margin was down due to a higher effective tax

rate and reduced gross margin, partially offset by lower SG&A as a

percentage of net sales. Gross margin declined due to unfavorable

product mix resulting from disproportionate growth of disposable

razors, higher commodity costs and volume scale deleverage which

were partially offset by price increases and manufacturing cost savings.

SG&A as a percentage of net sales was down due to lower overhead

and marketing spending. The economic downturn in fiscal 2009 has

resulted in a disproportionate decline in the Braun business particularly

in developing geographies, given the more discretionary nature of home

and personal grooming appliance purchases. We believe the Braun

business will return to sales and earnings growth rates consistent with

our long-term business plans. Failure to achieve these business plans

or a further deterioration of the macroeconomic conditions could

result in an impairment of the Braun business goodwill and intangibles

recorded in 2005 as part of the Gillette acquisition.

Grooming net sales increased 11% to $8.3billion in 2008. Net sales

were up behind 5% volume growth, a 7% favorable foreign exchange

impact and a 2% positive pricing impact driven by price increases

on premium shaving systems. Product mix had a negative 3% impact

on net sales as positive product mix from growth on the premium-

priced Gillette Fusion brand was more than offset by the impact of

disproportionate growth in developing regions, where selling prices

are below the segment average. Blades and Razors volume increased

high single digits behind double-digit growth in developing regions

driven primarily by Gillette Fusion expansion and the Prestobarba3

launch. In developed regions, Blades and Razors volume was down

low single digits as double-digit growth on Fusion was more than

offset by lower shipments of legacy shaving systems. Gillette Fusion

delivered more than $1billion in net sales for 2008. Braun volume

was down mid-single digits primarily due to supply constraints at a

contract manufacturer, the announced exits of certain appliance

businesses and the divestiture of the thermometer and blood pressure

devices business. Net earnings in Grooming were up 21% in 2008 to

$1.7billion behind net sales growth and a 170-basis point earnings

margin expansion. Earnings margin improved behind lower SG&A as

a percentage of net sales, partially offset by a reduction in gross

margin. Gross margin declined due to higher costs incurred at a

contract manufacturer on the Braun home appliance business, which

more than offset benefits from higher pricing and volume scale

leverage. SG&A as a percentage of net sales was down primarily due

to lower overhead spending driven largely by synergies from the

integration of Gillette into P&G’s infrastructure.

Health and Well-Being

HEALTH CARE

($ millions) 2009

Change vs.

Prior Year 2008

Change vs.

Prior Year

Volume n/a -4% n/a +4%

Net sales $13,623 -7% $14,578 +9%

Net earnings $2,435 -3% $2,506 +12%

Health Care net sales were down 7% to $13.6billion in 2009 on a

4% decline in unit volume. The divestitures of Thermacare and other

minor brands resulted in 1% of the unit volume decline. Unfavorable

foreign exchange reduced net sales by 5%. Negative product mix from

disproportionately higher volume declines of Personal Health Care and

Pharmaceuticals, which have higher than segment average selling

prices, reduced net sales by 2%. These negative impacts were partially

offset by positive pricing impacts of 4%. Organic sales were down

1% versus fiscal 2008. Volume declined mid-single digits in developed

regions and low single digits in developing regions. Personal Health

Care volume was down double digits due to the loss of marketplace

exclusivity of Prilosec in North America, the impact of a mild cold and

flu season on Vicks and the divestiture of Thermacare. All-outlet

value share of the U.S. personal health care market has declined over

2 points, including a double-digit share decline of Prilosec OTC.

Pharmaceuticals volume decreased high single digits mainly due to

minor brand divestitures and the impact of generic competition to our

Actonel brand in the osteoporosis category. The impact from the loss

of Prilosec exclusivity and from generic competition to the Actonel

brand are expected to continue. Oral Care volume declined low single

digits behind trade inventory reductions and market contractions in

North America and CEEMEA. Our global market share of oral care

was in line with the prior year. Feminine Care volume was down low

single digits mainly due to trade inventory reductions and market

contractions in North America and CEEMEA. Our global feminine care

market share was down half a point versus the prior year.