Proctor and Gamble 2009 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2009 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

|

|

Notes to Consolidated Financial Statements The Procter & Gamble Company 65

Amounts in millions of dollars except per share amounts or as otherwise specified.

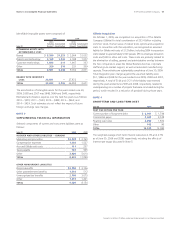

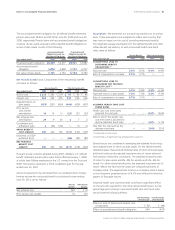

The accumulated benefit obligation for all defined benefit retirement

pension plans was $8,637 and $8,750 at June30,2009 and June30,

2008, respectively. Pension plans with accumulated benefit obligations

in excess of plan assets and plans with projected benefit obligations in

excess of plan assets consist of the following:

Accumulated Benefit

Obligation Exceeds the

Fair Value of Plan Assets

Projected Benefit

Obligation Exceeds the

Fair Value of Plan Assets

Years ended June 30 2009 2008 2009 2008

Projected benefit obligation $6,509 $5,277 $9,033 $7,987

Accumulated benefit

obligation 5,808 4,658 7,703 6,737

Fair value of plan assets 3,135 2,153 5,194 4,792

Net Periodic Benefit Cost. Components of the net periodic benefit

cost were as follows:

Pension Benefits Other Retiree Benefits

Years ended June 30 2009 2008 2007 2009 2008 2007

Service cost $214 $263 $279 $91 $95 $85

Interest cost 551 539 476 243 226 206

Expected return on

plan assets (473)(557)(454)(444)(429)(407)

Prior service

cost (credit)

amortization 14 14 13 (23) (21)(22)

Net actuarial loss

amortization 29 945 27 2

Curtailment and

settlement gain 6(36)(176)

—

(1)(1)

GROSS BENEFIT

COST (CREDIT) 341 232 183 (131)(123)(137)

Dividends on ESOP

preferred stock

—— —

(86) (95)(85)

NET PERIODIC

BENEFIT COST

(CREDIT) 341 232 183 (217)(218)(222)

Pursuant to plan revisions adopted during 2007, Gillette’s U.S. defined

benefit retirement pension plans were frozen effective January1, 2008,

at which time Gillette employees in the U.S. moved into the Trust and

ESOP. This revision resulted in a $154 curtailment gain for the year

ended June30, 2007.

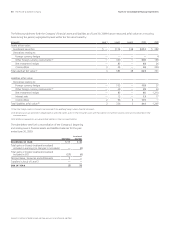

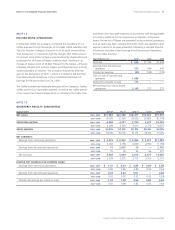

Amounts expected to be amortized from accumulated other compre-

hensive income into net period benefit cost during the year ending

June30, 2010, are as follows:

Pension

Benefits

Other Retiree

Benefits

Net actuarial loss $92 $19

Prior service cost (credit) 15 (21)

Assumptions. We determine our actuarial assumptions on an annual

basis. These assumptions are weighted to reflect each country that

may have an impact on the cost of providing retirement benefits.

The weighted average assumptions for the defined benefit and other

retiree benefit calculations, as well as assumed health care trend

rates, were as follows:

Pension Benefits Other Retiree Benefits

Years ended June 30 2009 2008 2009 2008

ASSUMPTIONS USED TO

DETERMINE BENEFIT

OBLIGATIONS (1)

Discount rate 6.0% 6.3% 6.4% 6.9%

Rate of compensation increase 3.7% 3.7%

——

ASSUMPTIONS USED TO

DETERMINE NET PERIODIC

BENEFIT COST (2)

Discount rate 6.3% 5.5% 6.9% 6.3%

Expected return on plan assets 7.4% 7.4% 9.3% 9.3%

Rate of compensation increase 3.7% 3.1%

——

ASSUMED HEALTH CARE COST

TREND RATES

Health care cost trend rates

assumed for next year

——

8.5% 8.6%

Rate to which the health care

cost trend rate is assumed to

decline (ultimate trend rate)

——

5.0% 5.1%

Year that the rate reaches the

ultimate trend rate

——

2016 2015

(1) Determined as of end of year.

(2) Determined as of beginning of year and adjusted for acquisitions.

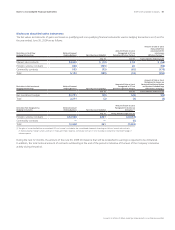

Several factors are considered in developing the estimate for the long-

term expected rate of return on plan assets. For the defined benefit

retirement plans, these include historical rates of return of broad equity

and bond indices and projected long-term rates of return obtained

from pension investment consultants. The expected long-term rates

of return for plan assets are 8%–9% for equities and 5% –6% for

bonds. For other retiree benefit plans, the expected long-term rate of

return reflects the fact that the assets are comprised primarily of

Company stock. The expected rate of return on Company stock is based

on the long-term projected return of 9.5% and reflects the historical

pattern of favorable returns.

Assumed health care cost trend rates could have a significant effect

on the amounts reported for the other retiree benefit plans. A one-

percentage point change in assumed health care cost trend rates

would have the following effects:

One-Percentage

Point Increase

One-Percentage

Point Decrease

Effect on total of service and interest cost

components $ 58 $(46)

Effect on postretirement benefit obligation 549 (447)