Proctor and Gamble 2009 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2009 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

|

|

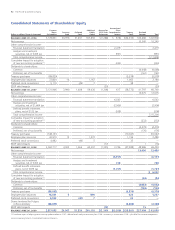

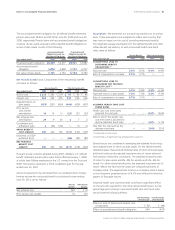

Notes to Consolidated Financial Statements The Procter & Gamble Company 59

Amounts in millions of dollars except per share amounts or as otherwise specified.

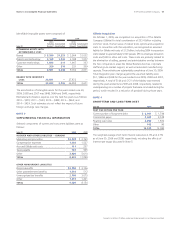

Interest Rate Risk Management

Our policy is to manage interest cost using a mixture of fixed-rate

and variable-rate debt. To manage this risk in a cost-efficient manner,

we enter into interest rate swaps in which we agree to exchange with

the counterparty, at specified intervals, the difference between fixed

and variable interest amounts calculated by reference to an agreed-

upon notional amount.

Interest rate swaps that meet specific accounting criteria are

accounted for as fair value and cash flow hedges. There were no fair

value hedging instruments at June30,2009 or June30,2008. For

cash flow hedges, the effective portion of the changes in fair value of

the hedging instrument is reported in other comprehensive income

(OCI) and reclassified into interest expense over the life of the under-

lying debt. The ineffective portion, which is not material for any year

presented, is immediately recognized in earnings.

Foreign Currency Risk Management

We manufacture and sell our products in a number of countries

throughout the world and, as a result, are exposed to movements in

foreign currency exchange rates. The purpose of our foreign currency

hedging program is to manage the volatility associated with short-

term changes in exchange rates.

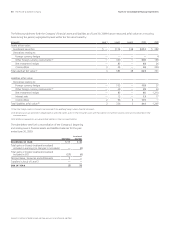

To manage this exchange rate risk, we have historically utilized a

combination of forward contracts, options and currency swaps. As

of June30,2009, we had currency swaps with maturities up to five

years, which are intended to offset the effect of exchange rate

fluctuations on intercompany loans denominated in foreign currencies

and are therefore accounted for as cash flow hedges. The Company

has also utilized forward contracts and options to offset the effect of

exchange rate fluctuations on forecasted sales, inventory purchases

and intercompany royalties denominated in foreign currencies. The

effective portion of the changes in fair value of these instruments is

reported in OCI and reclassified into earnings in the same financial

statement line item and in the same period or periods during which

the related hedged transactions affect earnings. The ineffective

portion, which is not material for any year presented, is immediately

recognized in earnings.

The change in value of certain non-qualifying instruments used to

manage foreign exchange exposure of intercompany financing

transactions, income from international operations and other balance

sheet items subject to revaluation is immediately recognized in

earnings, substantially offsetting the foreign currency mark-to-market

impact of the related exposure. The net earnings impact of such

instruments was a $1,047 loss in 2009 and gains of $1,397 and $56

in 2008 and 2007, respectively.

Net Investment Hedging

We hedge certain net investment positions in major foreign subsidiaries.

To accomplish this, we either borrow directly in foreign currencies

and designate all or a portion of foreign currency debt as a hedge of

the applicable net investment position or enter into foreign currency

swaps that are designated as hedges of our related foreign net

investments. Changes in the fair value of these instruments are imme-

diately recognized in OCI to offset the change in the value of the net

investment being hedged. Currency effects of these hedges reflected

in OCI were an after-tax gain of $964 in 2009 and $2,951 loss in 2008.

Accumulated net balances were a $4,059 and a $5,023 after-tax loss

as of June30,2009 and 2008, respectively.

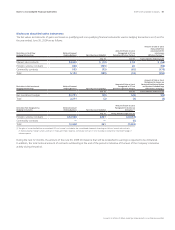

Commodity Risk Management

Certain raw materials used in our products or production processes

are subject to price volatility caused by weather, supply conditions,

political and economic variables and other unpredictable factors.

To manage the volatility related to anticipated purchases of certain of

these materials, we use futures and options with maturities generally

less than one year and swap contracts with maturities up to five years.

These market instruments generally are designated as cash flow

hedges. The effective portion of the changes in fair value for these

instruments is reported in OCI and reclassified into earnings in the

same financial statement line item and in the same period or periods

during which the hedged transactions affect earnings. The ineffective

and non-qualifying portions, which are not material for any year

presented, are immediately recognized in earnings.

Insurance

We self insure for most insurable risks. In addition, we purchase insur-

ance for Directors and Officers Liability and certain other coverage in

situations where it is required by law, by contract, or deemed to be in

the interest of the Company.

Fair Value Hierarchy

New accounting guidance on fair value measurements for certain

financial assets and liabilities requires that assets and liabilities carried

at fair value be classified and disclosed in one of the following three

categories:

Level 1: Quoted market prices in active markets for identical assets

or liabilities.

Level 2: Observable market-based inputs or unobservable inputs

that are corroborated by market data.

Level 3: Unobservable inputs reflecting the reporting entity’s own

assumptions or external inputs from inactive markets.

In valuing assets and liabilities, we are required to maximize the use

of quoted market prices and minimize the useof unobservable inputs.

We calculate the fair value of our Level 1 and Level 2 instruments

based on the exchange traded price of similar or identical instruments

where available or based on other observable instruments. The fair

value of our Level 3 instruments is calculated as the net present value

of expected cash flows based on externally provided inputs. These

calculations take into consideration the credit risk of both the Company

and our counterparties. The Company has not changed its valuation

techniques in measuring the fair value of any financial assets and

liabilities during the period.