Proctor and Gamble 2009 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2009 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

|

|

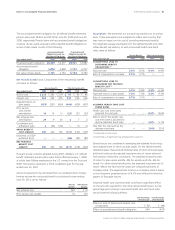

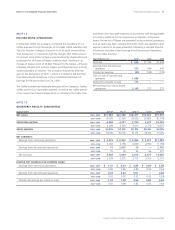

64 The Procter & Gamble Company Notes to Consolidated Financial Statements

Amounts in millions of dollars except per share amounts or as otherwise specified.

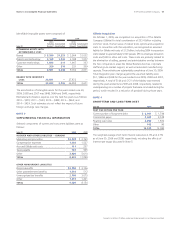

Obligation and Funded Status. We use a June30 measurement date

for our defined benefit retirement plans and other retiree benefit

plans. The following provides a reconciliation of benefit obligations,

plan assets and funded status of these plans:

Pension Benefits(1) Other Retiree Benefits(2)

Years ended June 30 2009 2008 2009 2008

CHANGE IN BENEFIT

OBLIGATION

Benefit obligation at

beginning of year(3) $10,095 $9,819 $3,553 $3,558

Service cost 214 263 91 95

Interest cost 551 539 243 226

Participants’ contributions 15 14 55 58

Amendments 47 52

—

(11)

Actuarial (gain) loss 456 (655)186 (232)

Acquisitions (divestitures) (3)(7)(17) 2

Curtailments and

settlements 3(68)

—

(3)

Special termination benefits 3116 2

Currency translation

and other (867)642 27 67

Benefit payments (498)(505)(226)(209)

BENEFIT OBLIGATION

AT END OF YEAR (3) 10,016 10,095 3,928 3,553

CHANGE IN PLAN ASSETS

Fair value of plan assets at

beginning of year7,225 7,350 3,225 3,390

Actual return on plan assets (401)(459)(678)(29)

Acquisitions (divestitures)

————

Employer contributions 657 507 18 21

Participants’ contributions 15 14 55 58

Currency translation

and other (688)318 (4)1

ESOP debt impacts (4)

——

4(7)

Benefit payments (498)(505)(226)(209)

FAIR VALUE OF PLAN

ASSETS AT END OF YEAR 6,310 7,225 2,394 3,225

FUNDED STATUS (3,706) (2,870)(1,534) (328)

(1) Primarily non-U.S.-based defined benefit retirement plans.

(2) Primarily U.S.-based other postretirement benefit plans.

(3) For the pension benefit plans, the benefit obligation is the projected benefit obligation.

For other retiree benefit plans, the benefit obligation is the accumulated postretirement

benefit obligation.

(4) Represents the net impact of ESOP debt service requirements, which is netted against plan

assets for Other Retiree Benefits.

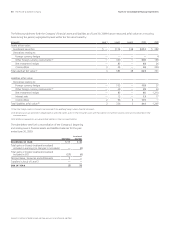

Pension Benefits Other Retiree Benefits

Years ended June 30 2009 2008 2009 2008

CLASSIFICATION OF NET

AMOUNT RECOGNIZED

Noncurrent assets $133 $321 $

—

$200

Current liability (41) (45)(18) (16)

Noncurrent liability (3,798) (3,146)(1,516) (512)

NET AMOUNT RECOGNIZED (3,706) (2,870)(1,534) (328)

AMOUNTS RECOGNIZED IN

ACCUMULATED OTHER

COMPREHENSIVE INCOME

(AOCI)

Net actuarial loss 1,976 715 1,860 578

Prior service cost (credit) 227 213 (152)(175)

NET AMOUNTS RECOGNIZED

IN AOCI 2,203 928 1,708 403

CHANGE IN PLAN ASSETS

AND BENEFIT OBLIGA-

TIONS RECOGNIZED IN

ACCUMULATED OTHER

COMPREHENSIVE INCOME

(AOCI)

Net actuarial loss

—

current year 1,335 361 1,309 226

Prior service cost (credit)

—

current year 47 52

—

(11)

Amortization of net actuarial

loss (29) (9)(2)(7)

Amortization of prior service

(cost) credit (14) (14)23 21

Settlement/ Curtailment cost

—

(32)

—

(2)

Currency translation

and other (64) 19 (25) 24

TOTAL CHANGE IN AOCI 1,275 377 1,305 251

NET AMOUNTS RECOGNIZED

IN PERIODIC BENEFIT COST

AND AOCI 1,616 609 1,088 33

The underfunding of pension benefits is primarily a function of

the different funding incentives that exist outside of the U.S. In

certain countries, there are no legal requirements or financial

incentives provided to companies to pre-fund pension obligations.

In these instances, benefit payments are typically paid directly from

the Company’s cash as they become due.