Proctor and Gamble 2009 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2009 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

|

|

Management’s Discussion and Analysis The Procter & Gamble Company 41

declines in U.S. all-outlet shares of Tide and Downy, partially offset by

share growth of Gain. Home Care volume was down low single digits

due to market contractions and trade inventory reductions. Batteries

volume declined high single digits due to market contractions, trade

inventory reductions and competitive activity, which drove a 1-point

market share decline of general purpose batteries.

Net earnings declined 11% to $3.0billion primarily due to reduced net

earnings margin and lower net sales. Net earnings margin contracted

130 basis points behind lower operating margin. Operating margin

was down primarily due to a commodity-driven decline in gross mar-

gin, which was partially offset by price increases and manufacturing

cost savings. Lower marketing spending as a percentage of net sales

was largely offset by higher overhead spending as a percentage of

net sales.

Fabric Care and Home Care net sales in 2008 increased 11% to

$23.7billion. Volume was up 6%, price increases added 1% and

favorable foreign exchange added 5% to net sales growth. This was

partially offset by a negative 1% mix impact primarily from dispropor-

tionate growth in developing regions and a shift toward larger sizes

in fabric care, both of which have selling prices below the segment

average. Fabric Care volume increased mid-single digits behind high

single-digit growth in developing regions and mid-single-digit

growth in developed regions. Growth was driven by the liquid laundry

detergent compaction launch in North America and initiative activity

on Tide, Gain, Ariel and Downy. Home Care volume was up mid-

single digits due to double-digit growth in developing regions and

high-teens growth on Febreze from the launch of Febreze Candles.

Batteries volume was up mid-single digits behind double-digit growth

in developing regions and mid-single-digit growth in developed

regions. Net earnings in Fabric Care and Home Care increased 9% to

$3.4billion in 2008 primarily behind higher net sales. Net earnings

margin was down 20 basis points primarily due to lower gross margin,

partially offset by a reduction in SG&A as a percentage of net sales.

Gross margin was down due to higher commodity costs, which more

than offset benefits from pricing, increased volume scale leverage and

manufacturing cost savings projects. SG&A improved as a percentage

of net sales due to lower overhead spending as a percentage of net

sales resulting from a focus on overhead productivity improvements.

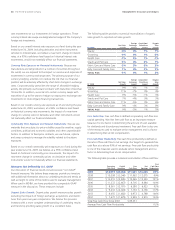

BABY CARE AND FAMILY CARE

($millions) 2009

Change vs.

Prior Year 2008

Change vs.

Prior Year

Volume n/a +1% n/a +4%

Net sales $14,103 +1% $13,898 +9%

Net earnings $1,770 +2% $1,728 +20%

Baby Care and Family Care net sales increased 1% to $14.1billion in

2009 on 1% volume growth. Pricing to help recover higher commodity

and energy costs contributed 5% to net sales growth. Unfavorable

foreign exchange reduced net sales by 4%. Negative product mix from

higher shipments of mid-tier brands, which have lower than segment

average selling prices, reduced net sales by 1%. Organic sales were up

7% on a 2% increase in organic volume. Volume growth was driven

by low single-digit growth in developing regions, while volume in

developed regions was in line with the prior year. Baby Care volume

increased low single digits due to growth of Pampers primarily in

developing regions and double-digit growth of Luvs in North America.

Our global market share of baby care was up nearly half a point.

Family Care volume was down low single digits due to the Western

European family care divestiture. Organic volume for Family Care was

up low single digits behind double-digit growth of Charmin Basic and

Bounty Basic. U.S. market share on Bounty was up nearly 1 point,

while Charmin market share remained consistent with the prior year.

Net earnings were up 2% versus the prior year to $1.8billion due to

net sales growth and higher net earnings margin. Net earnings margin

increased 10 basis points as higher gross margin was partially offset

by an increase in SG&A as a percentage of net sales and a higher

effective tax rate. Gross margin improved due to the impact of price

increases, manufacturing cost savings and more positive product mix

following the Western European family care divestiture, which more

than offset higher commodity and energy costs. SG&A as a percentage

of net sales increased due to the higher current period overhead

spending and base period reimbursements for services related to the

Western European family care divestiture, partially offset by lower

marketing spending.

Baby Care and Family Care net sales increased 9% in 2008 to

$13.9billion. Volume was up 4%, including the impact of the Western

European family care divestiture. Price increases contributed 1% to

net sales and foreign exchange had a positive 4% impact on net sales.

Organic volume and organic sales, which exclude the impacts of the

Western European family care divestiture and foreign exchange, both

grew 8%. Organic volume growth was balanced across the segment

with high single-digit growth in both Baby Care and Family Care.

Baby Care volume in developed regions was up mid-single digits

behind growth on the Pampers Baby Stages of Development and on

the Baby Dry Caterpillar Flex initiative. In developing regions, Baby

Care volume was up double digits behind continued growth on

Pampers. Family Care volume was down low single digits due to the

divestiture of the Western European family care business but was up

high single digits on an organic basis behind the Bounty and Charmin

product restages. U.S. market share on both Bounty and Charmin

was up over 1 point. Net earnings in Baby Care and Family Care were

up 20% to $1.7billion in 2008 behind higher net sales and earnings

margin expansion. Net earnings margin improved 110 basis points

primarily behind higher gross margin and lower SG&A as a percentage

of net sales. Gross margin was up due to a more profitable product

mix following the Western Europe family care divestiture, the benefit

of increased volume scale leverage, pricing and manufacturing cost

savings projects, which more than offset higher commodity and

energy costs. SG&A improved as a percentage of net sales due to

lower overhead spending as a percentage of net sales, partially offset

by higher marketing expenses as a percentage of net sales.