Proctor and Gamble 2010 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2010 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

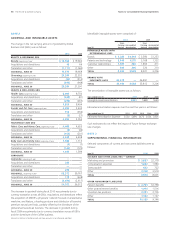

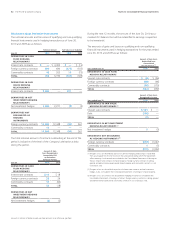

Notes to Consolidated Financial Statements The Procter & Gamble Company 59

Amounts in millions of dollars except per share amounts or as otherwise specified.

NOTE 4

SHORT-TERM AND LONG-TERM DEBT

June 30 2010 2009

DEBT DUE WITHIN ONE YEAR

Current portion of long-term debt $ 564 $ 6,941

Commercial paper 7,838 5,027

Other 70 4,352

TOTAL 8,472 16,320

Short-term weighted average interest rates (1) 0.4% 2.0%

(1) Weighted average short-term interest rates include the effects of interest rate swaps

discussed in Note 5.

June 30 2010 2009

LONG-TERM DEBT

1.35% USD note due August 2011 $ 1,000 $ —

4.88% EUR note due October 2011 1,221 1,411

1.38% USD note due August 2012 1,250 —

3.38% EUR note due December 2012 1,710 1,975

4.50% EUR note due May 2014 1,832 2,116

4.95% USD note due August 2014 900 900

3.50% USD note due February 2015 750 750

0.95% JPY note due May 2015 1,129 —

3.15% USD note due September 2015 500 —

4.85% USD note due December 2015 700 700

5.13% EUR note due October 2017 1,344 1,552

4.70% USD note due February 2019 1,250 1,250

4.13% EUR note due December 2020 733 846

9.36% ESOP debentures due 2010 – 2021 (1) 854 896

4.88% EUR note due May 2027 1,221 1,411

6.25% GBP note due January 2030 753 832

5.50% USD note due February 2034 500 500

5.80% USD note due August 2034 600 600

5.55% USD note due March 2037 1,400 1,400

Capital lease obligations 401 392

All other long-term debt 1,876 10,062

Current portion of long-term debt (564) (6,941)

TOTAL 21,360 20,652

Fair value of long-term debt 23,072 21,514

Long-term weighted average interest rates (2) 3.6% 4.9%

(1) Debt issued by the ESOP is guaranteed by the Company and must be recorded as debt of the

Company as discussed in Note 8.

(2) Weighted average long-term interest rates include the effects of interest rate swaps and net

investment hedges discussed in Note 5.

Long-term debt maturities during the next five years are as follows:

June 30 2011 2012 2013 2014 2015

Debt maturities $564 $2,304 $3,051 $1,924 $2,897

The Procter& Gamble Company fully and unconditionally guarantees

the registered debt and securities issued by its 100% owned finance

subsidiaries.

NOTE 5

RISK MANAGEMENT ACTIVITIES AND FAIR VALUE

MEASUREMENTS

As a multinational company with diverse product offerings, we are

exposed to market risks, such as changes in interest rates, currency

exchange rates and commodity prices. We evaluate exposures on a

centralized basis to take advantage of natural exposure netting and

correlation. To the extent we choose to manage volatility associated

with the net exposures, we enter into various financial transactions

which we account for using the applicable accounting guidance for

derivative instruments and hedging activities. These financial transac-

tions are governed by our policies covering acceptable counterparty

exposure, instrument types and other hedging practices.

At inception, we formally designate and document qualifying instru-

ments as hedges of underlying exposures. We formally assess, at

inception and at least quarterly, whether the financial instruments

used in hedging transactions are effective at offsetting changes in

either the fair value or cash flows of the related underlying exposure.

Fluctuations in the value of these instruments generally are offset by

changes in the value or cash flows of the underlying exposures being

hedged. This offset is driven by the high degree of effectiveness

between the exposure being hedged and the hedging instrument.

The ineffective portion of a change in the fair value of a qualifying

instrument is immediately recognized in earnings. The amount of

ineffectiveness recognized is immaterial for all years presented.

Credit Risk Management

We have counterparty credit guidelines and generally enter into

transactions with investment grade financial institutions. Counterparty

exposures are monitored daily and downgrades in counterparty

credit ratings are reviewed on a timely basis. Credit risk arising from

the inability of a counterparty to meet the terms of our financial

instrument contracts generally is limited to the amounts, if any, by

which the counterparty’s obligations to us exceed our obligations to

the counterparty. We have not incurred, and do not expect to incur,

material credit losses on our risk management or other financial

instruments.

Certain of the Company’s financial instruments used in hedging

transactions are governed by industry standard netting agreements

with counterparties. If the Company’s credit rating were to fall below

the levels stipulated in the agreements, the counterparties could

demand either collateralization or termination of the arrangement.

The aggregate fair value of the instruments covered by these contrac-

tual features that are in a net liability position as of June30, 2010

was $226. The Company has never been required to post collateral

as a result of these contractual features.