Proctor and Gamble 2015 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2015 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

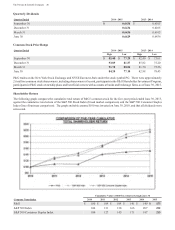

29 The Procter & Gamble Company

Net earnings from discontinued operations decreased $2.3

billion in 2015 due primarily to $2.1 billion of after tax

impairment charges in our atteries business (see Note 2 to

the Consolidated Financial Statements) and the absence of

fiscal 2015 earnings from our divested Pet Care business. Net

earnings attributable to Procter & Gamble decreased $4.6

billion, or 40 to $7.0 billion.

Diluted net earnings per share from continuing operations

decreased $0.80, or 21, to $3.06 due to the decrease in net

earnings. e had a diluted net loss per share from discontinued

operations of $0.62 due primarily to the impairment charges

on the atteries business. This was a reduction of $0.78 per

share versus the prior year. Diluted net earnings per share

decreased $1.57, or 39, to $2.44.

Core EPS decreased 2 to $4.02. Core EPS represents diluted

net earnings per share from continuing operations excluding

charges for enezuelan deconsolidation, balance sheet

remeasurement charges from foreign exchange policy changes

and devaluation in enezuela (see below), charges for certain

European legal matters and incremental restructuring related

to our productivity and cost savings plan. The decline was

driven by reduced net sales, partially offset by minor brand

divestiture gains.

Fiscal year 2014 compared with fiscal year 2013

Net earnings from continuing operations increased $365

million or 3 to $11.3 billion in 2014 due to the increase in

sales and a 40-basis point expansion in net earnings margin.

The increase in net earnings margin was primarily driven by

the decrease in SG&Aas a percentage of net sales and the lower

tax rate, partially offset by the gross margin contraction and

the acquisition and divestiture-driven net reduction in other

non-operating income, net.

Net earnings from discontinued operations increased $18

million in 2014 due to stronger results in our atteries business

offsetting the ongoing impacts of prior year product recalls in

Pet Care. Net earnings attributable to Procter & Gamble

increased $331 million, or 3 to $11.6 billion.

Diluted net earnings per share from continuing operations

increased 4 to $3.86 primarily due to the increase in net

earnings. Diluted net earnings per share from discontinued

operations was $0.15 due to the earnings of the atteries and

Pet Care businesses. Diluted net earnings per share increased

4 to $4.01.

Core EPS increased 5 to $4.09 primarily due to increased net

sales, a 40 basis point net earnings margin expansion and the

reduction in shares outstanding. Core EPS represents diluted

net earnings per share from continuing operations excluding

charges from foreign exchange policy changes and the

devaluation of the foreign exchange rates in enezuela (see

below), the 2013 holding gain on the purchase of the balance

of our Iberian joint venture, the 2013 impairment of goodwill

and indefinite-lived intangible assets and charges in both years

for European legal matters and incremental restructuring

related to our productivity and cost savings plan.

Veneuela Imacts

Effective June 30, 2015, the Company deconsolidated its local

enezuelan operations from our Consolidated Financial

Statements. P&G has operated in enezuela for over 65 years

and remains committed to serving enezuelan consumers with

our leading brands and products to grow our business. e

expect our operations in enezuela will continue for the

foreseeable future. e continue to work proactively with the

enezuelan official agencies to ensure we fully understand and

remain compliant as the policies within which our enezuelan

subsidiaries operate evolve. e do not expect this change in

accounting to directly affect the local operations of our

enezuelan subsidiaries.

There are a number of currency and other operating controls

and restrictions in enezuela, which have evolved over time

and may continue to evolve in the future. These evolving

conditions have resulted in an other-than-temporary lack of

exchangeability between the enezuelan bolivar and U.S.

dollar and have restricted our enezuelan operations ability

to pay dividends and satisfy certain other obligations

denominated in U.S. dollars. For accounting purposes, this has

resulted in a lack of control over our enezuelan subsidiaries.

Therefore, in accordance with the applicable accounting

standards for consolidation, effective June 30, 2015, we

deconsolidated our enezuelan subsidiaries and began

accounting for our investment in those subsidiaries using the

cost method of accounting. This change resulted in a fourth

quarter fiscal 2015 one-time before-tax charge of $2.0 billion

($2.1 billion after tax, or $0.71 per share). In future periods,

our financial results will only include sales of finished goods

to our enezuelan subsidiaries to the extent we receive

payments from enezuela (expected to be largely through the

CENCOEX exchange market). Accordingly, we will no longer

include the results of our enezuelan subsidiaries operations

in future reporting periods (see Note 1 to the Consolidated

Financial Statements). Our operations in enezuela accounted

for less than 2 of consolidated net sales and earnings from

continuing operations (before the deconsolidation charge)

during fiscal 2015.

enezuela is a highly inflationary economy under U.S. GAAP.

As a result, prior to deconsolidation, the U.S. dollar had been

the functional currency for our subsidiaries in enezuela. A

number of changes have been initiated in the enezuelan

exchange rate system, including changes that resulted in

devaluations to their currency. Prior to deconsolidation,

currency remeasurement adjustments for non-dollar

denominated monetary assets and liabilities held by our

enezuelan subsidiaries, along with any other transactional

foreign exchange gains and losses, have been reflected in

earnings, and totaled $104 million, $275 million and $236

million on an after-tax basis in 2015, 2014 and 2013,

respectively.

There are currently three official exchange rate mechanisms

in enezuela. The CENCOEX (National Center for External

Commerce) exchange rate is 6.3 enezuelan bolivares fuerte

(EF) per dollar and can be used for the importation of certain

qualifying products and materials. SICAD (Complementary