Safeway 2000 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2000 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

|

|

Safeway Inc. and Subsidiaries

21

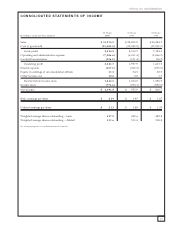

INTEREST EXPENSE Interest expense was $457.2 million

in 2000, compared to $362.2 million in 1999 and

$235.0 million in 1998. Interest expense increased in 2000

primarily due to debt incurred to finance the Randall’s

Acquisition, debt incurred to finance the repurchase of

Safeway stock during the fourth quarter of 1999 and, to a

lesser extent, higher interest rates on variable-rate borrow-

ings. Interest expense increased in 1999 primarily because

of the debt incurred to finance the Dominick’s, Carrs and

Randall’s Acquisitions and, to a lesser extent, to finance the

repurchase of Safeway stock during the fourth quarter of 1999.

As of year-end 2000, the Company had effectively con-

verted $100 million of its floating-rate debt to fixed-rate

debt through an interest rate swap agreement. Under the

swap agreement, Safeway pays interest of 6.2% on a $100

million notional amount and receives a variable interest rate

based on Federal Reserve rates quoted for commercial paper.

This agreement expires in 2007. Interest rate swap agree-

ments, and a cap agreement that expired in 1999, increased

interest expense by $0.2 million in 2000, $1.7 million in

1999 and $2.8 million in 1998.

EQUITY IN EARNINGS OF UNCONSOLIDATED AFFILIATE

Safeway’s investment in unconsolidated affiliate consists

of a 49% ownership interest in Casa Ley, S.A. de C.V.

(“Casa Ley”), which operates 97 food and general merchan-

dise stores in western Mexico. Safeway records its equity

in earnings of unconsolidated affiliate on a one-quarter

delay basis.

Income from Safeway’s equity investment in Casa Ley

decreased slightly to $31.2 million in 2000, from $34.5 mil-

lion in 1999 and $28.5 million in 1998.

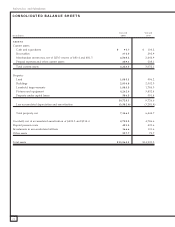

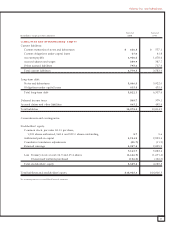

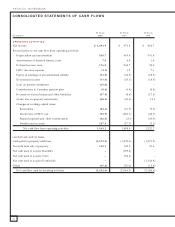

LIQUIDITY AND FINANCIAL RESOURCES

Net cash flow from operating activities was $1,901.1 million

in 2000, $1,488.4 million in 1999 and $1,252.7 million

in 1998. Net cash flow from operating activities increased

in 2000 and 1999 largely due to increased net income and

changes in working capital.

Cash flow used by investing activities was $1,481.0

million in 2000, $2,064.3 million in 1999 and $2,186.4

million in 1998. Cash flow used by investing activities

declined in 2000 primarily because of cash used to acquire

Randall’s and Dominick’s in 1999 and 1998, offset, in part,

by increased capital expenditures in 2000. Safeway opened

75 new stores and remodeled 275 stores in 2000. In 1999,

Safeway opened 67 new stores and remodeled 251 stores.

Cash flow used by financing activities was $434.4 million

in 2000 primarily due to cash flows from operations being

used to pay down debt. Cash flow from financing activities

was $636.0 million in 1999 primarily due to borrowing

related to the Randall’s and Carrs Acquisitions. Cash flow

from financing activities was $903.4 million in 1998,

reflecting borrowing related to the Dominick’s Acquisition.

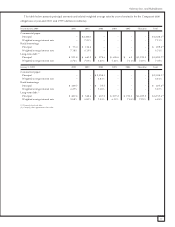

Net cash flow from operating activities as presented on

the consolidated statement of cash flows is an important

measure of cash generated by the Company’s operating activ-

ities. Operating cash flow, as defined below, is similar to net

cash flow from operations because it excludes certain non-

cash items. However, operating cash flow also excludes inter-

est expense and income taxes. Management believes that

operating cash flow is relevant because it assists investors in

evaluating Safeway’s ability to service its debt by providing a

commonly used measure of cash available to pay interest.

Operating cash flow also facilitates comparisons of Safeway’s

results of operations with those of companies having different

capital structures. Other companies may define operating

cash flow differently, and, as a result, such measures may not

be comparable to Safeway’s operating cash flow. Safeway’s

computation of operating cash flow is as follows:

(Dollars in millions) 2000 1999 1998

Income before income taxes $1,866.5 $ 1,674.0 $ 1,396.9

LIFO (income) expense (1.1) 1.2 7.1

Interest expense 457.2 362.2 235.0

Depreciation and amortization 830.7 695.6 531.4

Equity in earnings of

unconsolidated affiliate (31.2) (34.5) (28.5)

Operating cash flow $3,122.1 $ 2,698.5 $ 2,141.9

As a percent of sales 9.76% 9.35% 8.75%

As a multiple of interest expense 6.83x 7.45x 9.11x