Safeway 2000 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2000 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

|

|

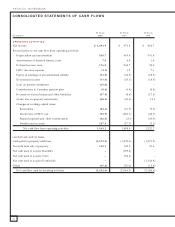

Safeway Inc. and Subsidiaries

32

NEW ACCOUNTING STANDARDS Statement of Financial

Accounting Standards (“SFAS”) No. 133, “Accounting for

Derivative Instruments and Hedging Activities,” is effective

for the Company as of December 31, 2000. SFAS No. 133

defines derivatives, requires that derivatives be carried at fair

value on the balance sheet, and provides for hedge account-

ing when certain conditions are met. Initial adoption of this

new accounting standard did not have a material impact on

Safeway’s financial statements.

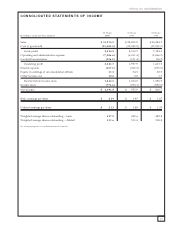

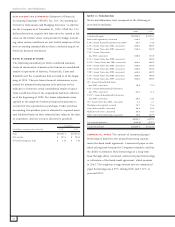

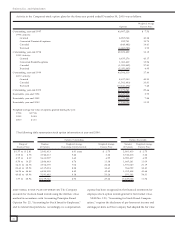

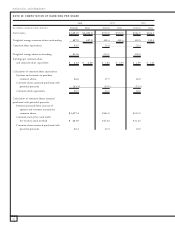

NOTE B: ACQUISITIONS

The following unaudited pro forma combined summary

financial information is based on the historical consolidated

results of operations of Safeway, Dominick’s, Carrs and

Randall’s as if the acquisitions had occurred as of the begin-

ning of 1998. This pro forma financial information is pre-

sented for informational purposes only and may not be

indicative of what the actual consolidated results of opera-

tions would have been if the acquisitions had been effective

as of the beginning of 1998. Pro forma adjustments were

applied to the respective historical financial statements to

account for the acquisitions as purchases. Under purchase

accounting, the purchase price is allocated to acquired assets

and liabilities based on their estimated fair values at the date

of acquisition, and any excess is allocated to goodwill.

Pro Forma

(in millions, except per-share amounts) 1999 1998

Sales $ 30,801.8 $ 29,474.1

Net income $ 957.6 $ 706.2

Diluted earnings per share $ 1.82 $ 1.42

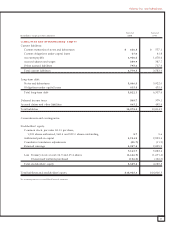

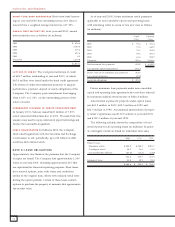

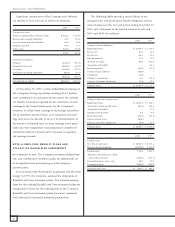

NOTE C: FINANCING

Notes and debentures were composed of the following at

year-end (in millions):

2000 1999

Commercial paper $ 2,328.1 $2,358.1

Bank credit agreement, unsecured 134.3 75.7

9.30% Senior Secured Debentures due 2007 24.3 24.3

6.85% Senior Notes due 2004, unsecured 200.0 200.0

7.00% Senior Notes due 2007, unsecured 250.0 250.0

7.45% Senior Debentures

due 2027, unsecured 150.0 150.0

5.75% Senior Notes due 2000, unsecured –400.0

5.875% Senior Notes due 2001, unsecured 400.0 400.0

6.05% Senior Notes due 2003, unsecured 350.0 350.0

6.50% Senior Notes due 2008, unsecured 250.0 250.0

7.00% Senior Notes due 2002, unsecured 600.0 600.0

7.25% Senior Notes due 2004, unsecured 400.0 400.0

7.50% Senior Notes due 2009, unsecured 500.0 500.0

10% Senior Subordinated Notes

due 2001, unsecured 79.9 79.9

9.65% Senior Subordinated Debentures

due 2004, unsecured 81.2 81.2

9.875% Senior Subordinated Debentures

due 2007, unsecured 24.2 24.2

10% Senior Notes due 2002, unsecured 6.1 6.1

Mortgage notes payable, secured 76.7 75.6

Other notes payable, unsecured 86.8 98.8

Medium-term notes, unsecured 16.5 25.5

Short-term bank borrowings, unsecured 75.0 129.7

6,033.1 6,479.1

Less current maturities (626.8) (557.1)

Long-term portion $ 5,406.3 $5,922.0

COMMERCIAL PAPER The amount of commercial paper

borrowings is limited to the unused borrowing capacity

under the bank credit agreement. Commercial paper is clas-

sified as long-term because the Company intends to and has

the ability to refinance these borrowings on a long-term

basis through either continued commercial paper borrowings

or utilization of the bank credit agreement, which matures

in 2002. The weighted average interest rate on commercial

paper borrowings was 6.59% during 2000 and 7.17% at

year-end 2000.