Safeway 2000 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2000 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

|

|

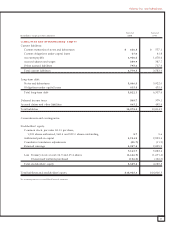

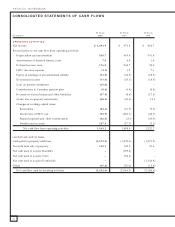

Safeway Inc. and Subsidiaries

31

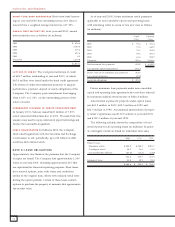

FAIR VALUE OF FINANCIAL INSTRUMENTS Accounting

principles generally accepted in the United States of America

require the disclosure of the fair value of certain financial

instruments, whether or not recognized in the balance sheet,

for which it is practicable to estimate fair value. Safeway

estimated the fair values presented below using appropriate

valuation methodologies and market information available

as of year-end. Considerable judgment is required to develop

estimates of fair value, and the estimates presented are not

necessarily indicative of the amounts that the Company

could realize in a current market exchange. The use of

different market assumptions or estimation methodologies

could have a material effect on the estimated fair values.

Additionally, these fair values were estimated at year-end,

and current estimates of fair value may differ significantly

from the amounts presented.

The following methods and assumptions were used to

estimate the fair value of each class of financial

instruments:

Cash and equivalents, accounts receivable, accounts payable

and short-term debt The carrying amount of these items

approximates fair value.

Long-term debt Market values quoted on the New York Stock

Exchange are used to estimate the fair value of publicly trad-

ed debt. To estimate the fair value of debt issues that are not

quoted on an exchange, the Company uses those interest

rates that are currently available to it for issuance of debt

with similar terms and remaining maturities. At year-end

2000 and 1999, the estimated fair value of debt approximat-

ed carrying values.

Off -balance sheet instruments The fair value of interest rate

swap agreements are the amounts at which they could be

settled based on estimates obtained from dealers. At year-end

2000, the net unrealized loss on such agreements was

$1.9 million compared to net unrealized gains of $4.7 million

at year-end 1999. Because the Company intends to hold this

agreement as a hedge for the term of the agreement, the

market risk associated with changes in interest rates is not

expected to be significant.

STORE CLOSING AND IMPAIRMENT CHARGES Safeway con-

tinually reviews its stores’ operating performance and assesses

the Company’s plans for certain store and plant closures.

The write-down of long-lived assets at stores that were

assessed for impairment because of management’s intention

to close the store or because of changes in circumstances that

indicate the carrying value of an asset many not be recover-

able is recognized in accordance with Statement of Financial

Accounting Standards (SFAS) No. 121, “Accounting for the

Impairment of Long-Lived Assets and for Long-Lived Assets

to be Disposed Of.” Safeway recognized impairment charges

on the write-down of long-lived assets at stores to be closed

of $8.4 million in 2000, $15.2 million in 1999 and

$15.3 million in 1998. For stores to be closed that are under

long-term leases, the Company records a liability for the

future minimum lease payments and related ancillary costs,

from the date of closure to the end of the remaining lease

term, net of estimated cost recoveries that may be achieved

through subletting properties or through favorable lease ter-

minations, at the time management commits to closing the

store. The operating costs, including depreciation, of stores

or other facilities to be closed are expensed during the period

they remain in use. Safeway had an accrued liability of

$138.5 million at year-end 2000 and $180.6 million at year-

end 1999 for such store lease exit costs, which is included

in Accrued Claims and Other Liabilities in the Company’s

consolidated balance sheets.

GOODWILL Goodwill was $4.7 billion at year-end 2000 and

$4.8 billion at year-end 1999, and is being amortized on a

straight-line basis over its estimated useful life of 40 years. If

it became probable that the projected future undiscounted

cash flows of acquired assets were less than the carrying value

of the goodwill, Safeway would recognize an impairment

loss in accordance with the provisions of SFAS No. 121.

Goodwill amortization was $126.2 million in 2000,

$101.4 million in 1999 and $56.3 million in 1998.

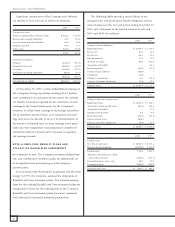

STOCK-BASED COMPENSATION Safeway accounts for stock-

based awards to employees using the intrinsic value method

in accordance with Accounting Principles Board Opinion

No. 25, “Accounting for Stock Issued to Employees.” The

disclosure requirements of SFAS No. 123, “Accounting for

Stock-Based Compensation,” are set forth in Note F.