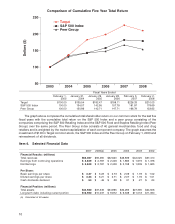

Target 2007 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2007 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

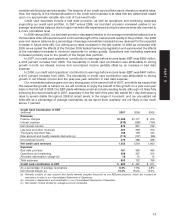

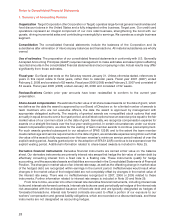

New Accounting Pronouncements

2007 Adoptions

In September 2006, the Financial Accounting Standards Board (FASB) issued SFAS No. 158. SFAS 158

requires sponsors of defined benefit pension and other postretirement benefit plans (collectively

postretirement benefit plans) to recognize the funded status of their postretirement benefit plans in the

statement of financial position, measure the fair value of plan assets and benefit obligations as of the date of

the fiscal year-end statement of financial position and provide additional disclosures. We adopted the

recognition and disclosure provisions of SFAS 158 during 2006. We adopted the SFAS 158 measurement date

provision at the beginning of the first quarter of 2007, and the details of our adoption of this provision are

described in Note 27.

In July 2006, the FASB issued FASB Interpretation No. 48, ‘‘Accounting for Uncertainty in Income Taxes –

an interpretation of FASB Statement No. 109’’ (FIN 48). FIN 48 prescribes the financial statement recognition

and measurement criteria for tax positions taken in a tax return, clarifies when tax benefits should be recorded

and how they should be classified in financial statements and requires certain disclosures of uncertain tax

matters. We adopted the provisions of FIN 48 at the beginning of the first quarter of 2007, and the details of our

adoption of FIN 48 are described in Note 22.

At the beginning of the first quarter of 2007, we adopted the FASB’s Emerging Issues Task Force Issue

No. 06-5, ‘‘Accounting for Purchases of Life Insurance – Determining the Amount That Could Be Realized in

Accordance with FASB Technical Bulletin No. 85-4, Accounting for Purchases of Life Insurance’’ and recorded

a $4 million increase to other noncurrent assets, with a corresponding increase to retained earnings of

$4 million.

2008 and Future Adoptions

In September 2006, the FASB issued SFAS No. 157, ‘‘Fair Value Measurement’’ (SFAS 157). SFAS 157

defines fair value, provides guidance for measuring fair value in U.S. generally accepted accounting principles

and expands disclosures about fair value measurements. SFAS 157 will be effective at the beginning of fiscal

2008 for financial assets and liabilities and at the beginning of fiscal 2009 for nonfinancial assets and liabilities.

The adoption of this statement will not have a material impact on our consolidated net earnings, cash flows or

financial position.

In February 2007, the FASB issued SFAS No. 159, ‘‘The Fair Value Option for Financial Assets and

Financial Liabilities’’ (SFAS 159). SFAS 159 permits entities to choose to measure many financial instruments

and certain other items at fair value. SFAS 159 will be effective at the beginning of fiscal 2008. The adoption of

this statement will not have a material impact on our consolidated net earnings, cash flows or financial

position.

In December 2007, the FASB issued SFAS No. 141(R), ‘‘Business Combinations’’ (SFAS 141(R)), which

changes the accounting for business combinations and their effects on the financial statements. SFAS 141(R)

will be effective at the beginning of fiscal 2009. The adoption of this statement is not expected to have a

material impact on our consolidated net earnings, cash flows or financial position.

In December 2007, the FASB issued SFAS No. 160, ‘‘Accounting and Reporting of Noncontrolling

Interests in Consolidated Financial Statements, an amendment of ARB No. 51’’ (SFAS 160). SFAS 160

requires entities to report non-controlling interests in subsidiaries as equity in their consolidated financial

statements. SFAS 160 will be effective at the beginning of fiscal 2009. The adoption of this statement is not

expected to have a material impact on our consolidated net earnings, cash flows or financial position.

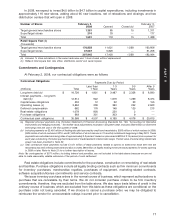

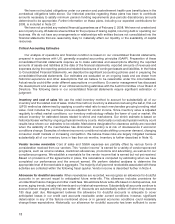

Forward-Looking Statements

This report, including the preceding Management’s Discussion and Analysis, contains forward-looking

statements regarding our performance, financial position, liquidity and adequacy of capital resources.

Forward-looking statements are typically accompanied by the words ‘‘expect,’’ ‘‘may,’’ ‘‘could,’’ ‘‘believe,’’

‘‘would,’’ ‘‘might,’’ ‘‘anticipates,’’ or words of similar import. The forward-looking statements in this report

include the anticipated impact of new and proposed accounting pronouncements, the expected outcome of

pending and threatened litigation, our expectations with respect to our share repurchase program and our

outlook in fiscal 2008. Forward-looking statements are based on our current assumptions and expectations

and are subject to certain risks and uncertainties that could cause actual results to differ materially from those

20