Target 2007 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2007 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

|

|

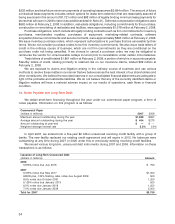

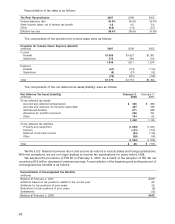

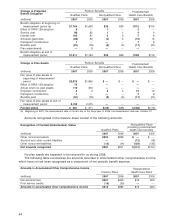

Defined Contribution Plan Expenses

(millions) 2007 2006 2005

401(k) Defined Contribution Plan

Matching contributions expense $172 $141 $118

Nonqualified Deferred Compensation Plans

Benefits expense $46 $98 $64

Related investment income (26) (68) (34)

Nonqualified plan net expense $20 $30 $30

27. Pension and Postretirement Health Care Benefits

We have qualified defined benefit pension plans covering all U.S. team members who meet age and

service requirements. We also have unfunded nonqualified pension plans for team members with qualified

plan compensation restrictions. Benefits are provided based on years of service and team member

compensation. Upon retirement, team members also become eligible for certain health care benefits if they

meet minimum age and service requirements and agree to contribute a portion of the cost.

In September 2006, the FASB issued SFAS No. 158, ‘‘Employers’ Accounting for Defined Benefit Pension

and Other Postretirement Plans, an amendment of FASB Statements No. 87, 88, 106, and 132(R)’’ (SFAS 158).

SFAS 158 requires plan sponsors of defined benefit pension and other postretirement benefit plans

(collectively postretirement benefit plans) to recognize the funded status of their postretirement benefit plans

in the statement of financial position, measure the fair value of plan assets and benefit obligations as of the

date of the fiscal year-end statement of financial position and provide additional disclosures.

At the beginning of fiscal 2007, we early adopted the measurement date provisions of SFAS 158. The

measurement date provisions of SFAS 158 require us to measure the fair value of plan assets and benefit

obligations as of the date of the year-end statement of financial position. Before 2007, we measured our

pension and postretirement benefit obligations at the end of October each year. As a result, we recorded a

$16 million decrease to retained earnings, a $54 million increase to accumulated other comprehensive

income, a $65 million increase to other noncurrent assets, a $3 million increase to other noncurrent liabilities

and a $24 million decrease to deferred income taxes. The adoption of the measurement date provisions of

SFAS 158 had no effect on our Consolidated Statements of Financial Position at February 4, 2007 or any prior

periods.

We adopted the recognition and disclosure provisions of SFAS 158 on February 3, 2007. The recognition

provisions of SFAS 158 required us to recognize the funded status, which is the difference between the fair

value of plan assets and the projected benefit obligations, of our postretirement benefit plans in the

February 3, 2007 Consolidated Statements of Financial Position, with a corresponding adjustment to

accumulated other comprehensive loss, net of tax. The adjustment to accumulated other comprehensive loss

at adoption represents the net unrecognized actuarial losses and unrecognized prior service costs, both of

which were previously netted against the plans’ funded status in our Consolidated Statements of Financial

Position pursuant to the provisions of SFAS No. 87, ‘‘Employers’ Accounting for Pensions’’ (SFAS 87). These

amounts will be subsequently recognized as net periodic pension expense pursuant to our historical

accounting policy for amortizing such amounts. Further, actuarial gains and losses that arise in subsequent

periods and are not recognized as net periodic pension expense in the same periods will be recognized as a

component of other comprehensive income. Those amounts will be subsequently recognized as a

component of net periodic pension expense on the same basis as the amounts recognized in accumulated

other comprehensive loss at adoption of SFAS 158. The adoption of the recognition provisions of SFAS 158

had no effect on our Consolidated Statements of Operations at February 3, 2007 or any prior periods.

43

PART II