Windstream 2008 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2008 Windstream annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

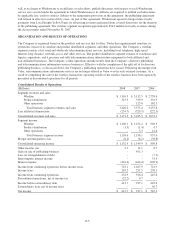

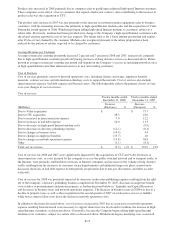

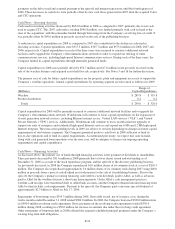

Wireline Segment Income

The following table reflects the primary drivers of year-over-year changes in wireline segment income:

Wireline segment income

Twelve months ended

December 31, 2008

Twelve months ended

December 31, 2007

(Millions)

Increase

(Decrease) %

Increase

(Decrease) %

Due to Valor acquisition $ - $ 105.6

Due to CTC acquisition 21.2 15.7

Due to elimination of royalty licensing agreement with Alltel - 129.6

Due to depreciation rate studies 35.4 18.3

Due to split off directory publishing business (41.6) -

Other (29.1) (35.3)

Total wireline segment income (loss) $ (14.1) (1)% $ 233.9 25%

Changes in wireline segment income in 2008 and 2007 primarily resulted from the acquisitions of Valor and CTC and

reduced depreciation rates, as discussed above. In addition, in 2008, wireline segment income declined due to the net

decreases in directory publishing revenues and expenses as a result of the split off of the publishing business in the

fourth quarter in 2007. In 2007, wireline segment income was also significantly impacted by the elimination of royalty

expenses that were paid to Alltel prior to the spin off. The remaining changes in segment income in 2008 and 2007

primarily resulted from the decline in revenues associated with the continued access line losses, partially offset by

increases in high-speed Internet customers.

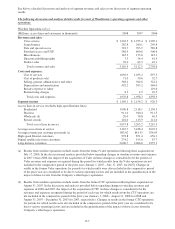

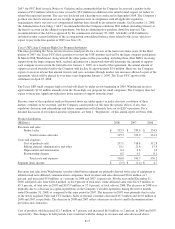

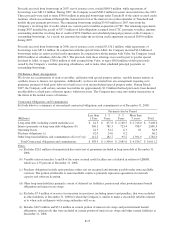

Merger and integration costs related to the wireline operations, which are triggered by strategic transactions and are

unpredictable by nature, are not included in the determination of segment income. Set forth below is a summary of

wireline merger and integration costs for the years ended December 31:

Merger and integration costs

(Millions) 2008 2007 2006

Transaction costs associated with the acquisition of CTC $ 0.1 $ 0.6 $ -

Transaction costs associated with spin off from Alltel - - 7.9

Signage and other rebranding costs - 1.4 13.8

Computer system separation and conversion costs 6.1 2.5 5.9

Total merger and integration costs $ 6.2 $ 4.5 $ 27.6

Regulatory Matters – Wireline Operations

Our incumbent local exchange carrier subsidiaries (collectively the “ILECs”) are regulated by both federal and state

agencies. Interstate products and services and the related earnings are subject to federal regulation by the Federal

Communications Commission (“FCC”), and our local and intrastate products and services and the related earnings are

subject to regulation by state Public Service Commissions (“PSCs”). The FCC has principal jurisdiction over interstate

switched and special access rates and high-speed Internet service offerings and regulates the rates that ILECs may

charge for the use of their local networks in originating or terminating interstate and international transmissions. State

PSCs have jurisdiction over matters including local service rates, intrastate access rates, quality of service, the

disposition of public utility property and the issuance of securities or debt by the local operating companies.

Federal Regulation and Legislation

Communications service providers are regulated differently depending primarily upon the network technology used to

deliver the service. This patchwork regulatory approach advantages certain companies and disadvantages others. It

impedes market-based competition where service providers, regardless of technology, exchange telecommunications

traffic between their networks and compete for customers.

From time to time, federal legislation is introduced dealing with various matters that could affect our business. Most

proposed legislation of this type never becomes law. It is difficult to predict what kind of reform efforts, if any, may be

introduced in Congress and ultimately become law. Windstream strongly supports the modernization of the nation’s

telecommunications laws, but at this time, cannot predict the timing and the resulting financial impact of any possible

federal legislative efforts.

On February 17, 2009, the American Recovery and Reinvestment Bill of 2009 was signed into law that includes

various financial incentives to qualifying entities for the expansion of broadband services in both unserved and

underserved communities throughout the nation.

F-15