Windstream 2008 Annual Report Download - page 133

Download and view the complete annual report

Please find page 133 of the 2008 Windstream annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

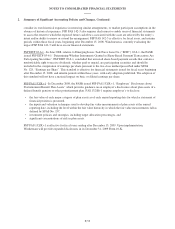

2. Summary of Significant Accounting Policies and Changes, Continued:

Derivative Instruments – SFAS No. 133, “Accounting for Derivative Instruments and Hedging Activities”, as

amended, provides guidance on accounting for derivatives, including interest rate swaps. In addition, SFAS

No. 133 governs when a derivative or other financial instrument can be designated as a hedge, and requires

recognition of all derivative instruments at fair value. Accounting for the changes in fair value depends on

whether the derivative has been designated as, qualifies as and is effective as a hedge. Changes in fair value of the

effective portions of hedges should be recorded as a component of other comprehensive income in the current

period. Changes in fair values of the derivative instruments not qualifying as hedges, or of any ineffective portion

of hedges, should be recognized in earnings in the current period.

On July 17, 2006, in conjunction with issuing debt, Windstream entered into four identical pay fixed, receive

variable interest rate swap agreements totaling $1,600.0 million in notional value in order to mitigate the interest

rate risk inherent in its variable rate senior secured credit facilities. The four interest rate swap agreements

amortize quarterly to a notional value of $906.3 million at maturity on July 17, 2013. The variable rate received

resets on the seventeenth day of each quarter to the three-month LIBOR (London-Interbank Offered Rate). The

Company’s interest rate swap agreements are designated as cash flow hedges of the interest rate risk created by

the variable interest rate paid on Tranche B of the senior secured credit facilities, which matures on July 17, 2013.

The variable interest rate paid on Tranche B is based on the three-month LIBOR, and it also resets on the

seventeenth day of each quarter.

After the completion of a refinancing transaction in February 2007, a portion of one of the four interest rate swap

agreements with a notional value of $125.0 million ($105.0 million as of December 31, 2008) was de-designated

as the corresponding hedged item was repaid. Therefore, the undesignated portion of the swap agreement was no

longer an effective hedge of the variable interest rate paid on Tranche B.

Set forth below is information related to the Company’s interest rate swap agreements as of December 31:

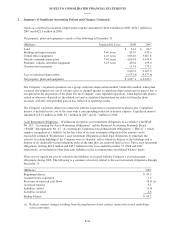

(Millions, except for percentages) 2008 2007

Unamortized notional value:

Designated portion $ 1,176.2 $ 1,296.7

Undesignated portion $ 105.0 $ 115.8

Fair value of interest rate swap agreements (see Note 6):

Designated portion $ (144.8) $ (80.4)

Undesignated portion $ (8.6) $ (2.8)

Weighted average fixed rate paid 5.60% 5.60%

Variable rate received 4.55% 5.21%

The effectiveness of the Company’s cash flow hedges is assessed each quarter using the “Change in Variable Cash

Flow Method”, or Method 1, described in Derivatives Implementation Group (“DIG”) Issue No. G7, “Cash Flow

Hedges: Measuring the Ineffectiveness of a Cash Flow Hedge under Paragraph 30(b) When the Shortcut Method

Is Not Applied”. Method 1 utilizes the matched terms principle of measuring effectiveness, and requires the

floating-rate leg of the swap and the hedged variable cash flows of the asset or liability to be based on the same

interest rate index. It also requires the variable interest rates of both instruments to reset on the same dates.

Furthermore, there should be no other differences in the terms of the hedge and the hedged item, and the

likelihood of default by the interest rate swap counterparties must be assessed as being unlikely in order to

conclude that there is no ineffectiveness in the hedging relationship. The Company performs and documents this

assessment under Method 1 each quarter, and it concluded at December 31, 2008 that there was no ineffectiveness

to be recognized in earnings in any of its four interest rate swap agreements that are designated as hedges.

In accordance with SFAS No. 133, the Company recognizes all derivative instruments at fair value in the

accompanying consolidated balance sheets as either assets or liabilities depending on the rights or obligations

under the related contracts. Changes in the fair value of the effective portion of these derivative instruments were

F-45