Windstream 2008 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2008 Windstream annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

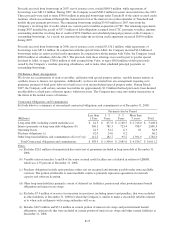

|

|

the length of time the receivables are past due and historical collection experience. Based on these assumptions, we

record an allowance for doubtful accounts to reduce the related receivables to the amount that we ultimately expect to

collect from customers. If circumstances related to specific customers change or economic conditions worsen such that

our past collection experience is no longer relevant, our estimate of the recoverability of our trade receivables could be

further reduced from the levels provided for in the consolidated financial statements.

Pension and Other Postretirement Benefits – The annual costs of providing pension and other postretirement benefits

are based on certain key actuarial assumptions, including the expected return on plan assets, discount rate and

healthcare cost trend rate. Windstream’s pension expense for 2009, estimated to be approximately $90.4 million, was

calculated based upon a number of actuarial assumptions, including an expected long-term rate of return on qualified

pension plan assets of 8.0 percent and a discount rate of 6.18 percent. In developing the expected long-term rate of

return assumption, Windstream considered its historical rate of return, as well as input from its investment advisors.

Historical returns of the plan were 9.45 percent since 1975, including periods in which it was sponsored by Alltel.

Projected returns on qualified pension plan assets were based on broad equity and bond indices and include a targeted

asset allocation of 52.5 percent to equities, 37.5 percent to fixed income assets and 10.0 percent to alternative

investments, with an aggregate expected long-term rate of return of approximately 8.0 percent. Lowering the expected

long-term rate of return on the qualified pension plan assets by 50 basis points (from 8.0 percent to 7.5 percent) would

result in an increase in our pension expense of approximately $3.2 million in 2009.

The discount rate selected is based on the Company’s expected pension benefit payments discounted from their

expected payment date to the measurement date using the appropriate spot rate from the Citigroup Pensions Discount

Curve. The discount rate determined on this basis was 6.18 percent at December 31, 2008. Lowering the discount rate

by 25 basis points (from 6.18 percent to 5.93 percent) would result in an increase in our pension expense of

approximately $4.4 million in 2009.

As a component of determining its annual pension cost, Windstream amortizes unrecognized gains or losses that

exceed 17.5 percent of the greater of the projected benefit obligation or market-related value of plan assets on a

straight-line basis over five years. Unrecognized actuarial gains and losses below the 17.5 percent corridor are

amortized over the average remaining service life of active employees, which is approximately 10 years for the pension

plan during 2009.

On August 17, 2006, the Pension Protection Act of 2006 (the “2006 Act”) was signed into law by Congress. In general,

the 2006 Act changed the rules governing the minimum contribution requirements for funding a qualified pension plan

on an annual basis without paying excise tax penalties. Among other requirements, the 2006 Act changed the

assumptions used to calculate the minimum lump-sum benefit payments, applied benefit restrictions to plans below

certain funding levels, and eliminated certain sunset provisions contained in the Economic Growth and Tax Relief

Reconciliation Act of 2001 (“EGTRRA”). EGTRRA increased the maximum amount of benefits that a qualified

defined benefit pension plan could pay and increased the maximum compensation amount allowed for determining

benefits for qualified pension plans. Windstream is complying with the provisions of the 2006 Act. The qualified

pension plan is expected to be at least 80 percent funded for the 2008 plan year and therefore is not expected to be

subject to benefit restrictions in 2009. The assumptions selected as of December 31, 2008 for financial reporting

purposes for the qualified pension plan reflected the impact of the 2006 Act. The 2006 Act has not had a significant

accounting impact nor has it triggered a significant event for the qualified pension plan. Windstream’s preliminary

funding analysis estimates prepared in accordance with the 2006 Act indicate that the Company will be required to

make a contribution in 2010 of approximately $24.0 million, net of tax benefit. Contributions to the plan are dependent

on various factors, including future investment performance, changes in future discount rates and changes in the

demographics of the population participating in the qualified pension plan.

We calculated our annual postretirement expense for 2009 based upon a number of actuarial assumptions, including a

healthcare cost trend rate of 8.5 percent and a discount rate of 6.11 percent. Consistent with the methodology used to

determine the appropriate discount rate for the Company’s pension obligations, the discount rate selected for

postretirement benefits is based on the Company’s expected postretirement benefit payments discounted from their

expected payment date to the measurement date using the appropriate spot rate from the Citigroup Pensions Discount

Curve. The discount rate determined on this basis was 6.11 percent at December 31, 2008. Lowering the discount rate

by 25 basis points (from 6.11 percent to 5.86 percent) would result in an increase in postretirement expense of

approximately $0.1 million in 2009.

The healthcare cost trend rate is based on our actual medical claims experiences adjusted for future projections of

medical costs. For the year ended December 31, 2009, a one percent increase in the assumed healthcare cost trend rate

would increase our postretirement benefit cost by approximately $0.2 million, while a one percent decrease in the rate

would reduce our allocation of postretirement benefit cost by approximately $0.2 million.

F-28