Windstream 2008 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2008 Windstream annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

6. Fair Value Measurements:

The Company’s financial instruments consist primarily of cash and cash equivalents, accounts receivable,

accounts payable, long-term debt and interest rate swaps. The carrying amount of accounts receivable and

accounts payable was estimated by management to approximate fair value due to the relatively short period of

time to maturity for those instruments. Cash equivalents, long-term debt and interest rate swaps are measured at

fair value on a recurring basis in accordance with the fair value measurement provisions of SFAS No. 157.

Windstream utilizes market data or assumptions that market participants would use in pricing the asset or liability,

including assumptions about risk and the risks inherent in the inputs to the valuation technique. These inputs can

be readily observable, market corroborated, or generally unobservable. Valuation techniques that maximize the

use of observable inputs and minimize the use of unobservable inputs are used and the fair value balances are

classified based on the observability of those inputs. The highest priority is given to unadjusted quoted prices in

active markets for identical assets or liabilities (level 1 measurement) and the lowest priority is given to

unobservable inputs (level 3 measurement). As required by SFAS No. 157, financial assets and liabilities are

classified in their entirety based on the lowest level of input that is significant to the fair value measurement. The

Company’s assessment of the significance of a particular input to the fair value measurement requires judgment

and may affect the valuation of fair value assets and liabilities and their placement within the fair value hierarchy

levels.

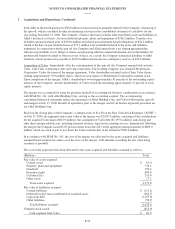

The fair values of the Company’s cash equivalents and interest rate swaps were determined using the following

inputs at December 31, 2008:

Quoted Price

in Active Markets

for

Identical Assets

Significant

Other

Observable

Inputs

Significant

Unobservable

Inputs

(Millions)

Fair

Value

Carrying

Amount Level 1 Level 2 Level 3

Cash equivalents (a) $ 296.6 $ 296.6 $ 296.6 $ - $ -

Interest rate swaps (b) $ 153.4 $ 153.4 $ - $ 153.4 $ -

(a) Included in cash and cash equivalents on the consolidated balance sheets.

(b) Included in other current liabilities and other liabilities on the consolidated balance sheets.

The Company’s cash equivalents are primarily highly liquid, actively traded money market funds with next day

access. The fair values of the interest rate swaps were determined based on the present value of expected future

cash flows using LIBOR swap rates which are observable at commonly quoted intervals for the full term of the

swaps using discount rates appropriate with consideration given to the Company’s non-performance risk.

Deducted from the December 31, 2008, interest rate swap fair value calculation was a $17.4 million adjustment in

consideration of the Company’s non-performance risk. The Company’s non-performance risk is assessed based on

the current trading discount of its Tranche B senior secured credit facility as the swap agreements are secured by

the same collateral. In addition, the Company routinely monitors and updates its evaluation of counterparty risk,

and based on such evaluation has determined that the swap agreements continue to meet the requirements of an

effective cash flow hedge. The counterparty to each of the four swap agreements is a bank with a current credit

rating at or above A+.

The fair value and carrying value of the Company’s long-term debt was $4,637.0 million and $5,382.5 million,

respectively, as of December 31, 2008. The fair value of the corporate bonds was calculated based on quoted

market prices of the specific issuances in an active market when available. When an active market is not available

for certain bonds and bank notes, the fair market value was determined based on bid prices and broker quotes. In

calculating the fair market value of the revolving line of credit and Windstream Holdings of the Midwest Inc.

bonds, an appropriate market price for similar instruments in an active market were used considering credit

quality, nonperformance risk and maturity of the instrument.

F-62