Windstream 2008 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2008 Windstream annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

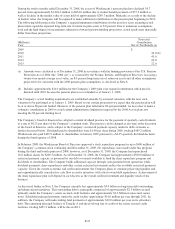

The indentures governing our senior secured credit facilities and senior notes include customary covenants that, among

other things, require the Company to maintain certain financial ratios and restrict our ability to incur additional

indebtedness. In particular, the Company must maintain the following financial ratios:

(a) total leverage ratio must be no greater than 4.5 to 1.0 on the last day of any fiscal quarter;

(b) interest coverage ratio must be greater than 2.75 to 1.0 on the last day of any fiscal quarter; and

(c) capital expenditures must not exceed a specified amount in any fiscal year (for 2009 this amount is $582.5

million, which includes $132.5 million of unused capacity from 2008).

In addition, certain of the Company’s debt agreements contain various covenants and restrictions specific to the

subsidiary that is the legal counterparty to the agreement. Under the Company’s long-term debt agreements,

acceleration of principal payments would occur upon payment default, violation of debt covenants not cured within 30

days, or breach of certain other conditions set forth in the borrowing agreements. At December 31, 2008, the Company

was in compliance with all such covenants and restrictions.

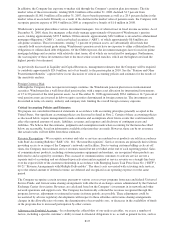

As of December 31, 2008, Moody’s Investors Service (“Moody’s”), Standard & Poor’s Corporation (“S&P”) and Fitch

Ratings (“Fitch”) had granted Windstream the following senior secured and senior unsecured credit ratings:

Description Moody’s S&P Fitch

Senior secured credit rating Baa3 BBB BBB-

Senior unsecured credit rating Ba3 BB BB+

Outlook Stable Stable Stable

Factors that could affect Windstream’s short and long-term credit ratings would include, but are not limited to, a

material decline in the Company’s operating results, increased debt levels relative to operating cash flows resulting

from future acquisitions, increased capital expenditure requirements, or changes to our dividend policy. If

Windstream’s credit ratings were to be downgraded from current levels, the Company would incur higher interest costs

on its borrowings, and the Company’s access to the public capital markets could be adversely affected. The Company’s

exposure to interest risk is further discussed in the Market Risk section below. A downgrade in Windstream’s current

short or long-term credit ratings would not accelerate scheduled principal payments of Windstream’s existing long-

term debt, as discussed further in Note 5. Windstream’s next scheduled debt maturity is in 2011. Given the Company’s

ability to generate cash flow, these maturities could be funded with available cash, if necessary.

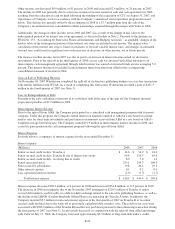

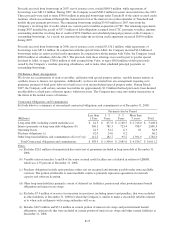

Historical Cash Flows

(Millions) 2008 2007 2006

Cash flows from (used in):

Operating activities $ 1,080.4 $ 1,033.7 $ 1,145.7

Investing activities (233.1) (867.1) (299.0)

Financing activities (622.7) (481.4) (471.8)

Change in cash and cash equivalents $ 224.6 $ (314.8) $ 374.9

Cash Flows – Operating Activities

Cash provided from operations is the Company’s primary source of funds. Cash flows from operating activities

increased by $46.7 million in 2008 as compared to 2007, primarily from the deferral of approximately $53.3 million in

cash tax payments due to the Economic Stimulus Act that allowed Windstream to deduct half of the costs of qualifying

asset purchases in 2008 for federal income tax purposes and a reduction in merger, integration and restructuring

payments. These increases were partially offset by changes in working capital requirements, including timing

differences in the billing and collections of accounts receivable, payment of trade payables and purchases of inventory.

During 2008, the Company generated sufficient cash flows from operations to fund its capital expenditures, scheduled

principle payments of long-term debt and payment of dividends as further discussed below.

Cash flows from operating activities decreased by $112.0 million in 2007 as compared to 2006. This decrease was

primarily due to increases of $140.1 million in interest payments as the Company did not make its first interest

F-23