American Express 2008 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2008 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

|

|

notes to consolidated financial statements

american express company

85

(b) The interest-only strip is accounted for at fair value and is reported in other

assets on the Company’s Consolidated Balance Sheets with changes in fair

value recorded in securitization income, net in the Company’s Consolidated

Statements of Income.

The Company partially adopted SFAS No. 157 as of

January 1, 2008. SFAS No. 157 established a three-level

hierarchy of valuation techniques used to measure fair value.

Refer to Note 1 for additional discussion regarding each level

in the fair value hierarchy as defined by SFAS No. 157. The

Company classifies its subordinated securities and its interest-

only strip in Level 3 of the fair value hierarchy.

The Company determines the fair value of its retained

subordinated securities using discounted cash flow models.

The discount rate used is based on an interest rate curve

that is observable in the marketplace plus an unobservable

credit spread commensurate with the risk of these securities

and similar financial instruments. The Company classifies

such securities in Level 3 of the fair value hierarchy because

the applicable credit spreads are not observable due to the

illiquidity in the market with respect to these securities and

similar financial instruments.

The fair value of the interest-only strip is the present value of

estimated future positive excess spread expected to be generated

by the securitized loans over the estimated remaining life of those

loans. Management utilizes certain estimates and assumptions to

determine the fair value of the interest-only strip asset, including

estimates for finance charge yield, credit losses, LIBOR (which

determines future certificate interest costs), monthly payment

rate and discount rate. On a quarterly basis, the Company

compares the assumptions it uses in calculating the fair value of

its interest-only strip to observable market data when available,

and to historical trends. The interest-only strip is classified

within Level 3 of the fair value hierarchy due to the significance

of the unobservable inputs used in valuing this asset.

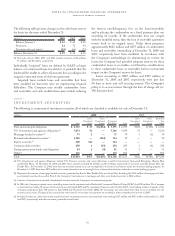

The following table presents the changes in fair value of the

Company’s retained subordinated securities and its interest-

only strip during the year ended December 31, 2008:

(Millions)

Investments-

Retained

Subordinated

Securities

Other

Assets-

Interest-

Only Strip

Beginning fair value $ 78 $ 223

Increases in securitized loans 1,250 71

Decreases in securitized loans — (42)

Total realized and unrealized losses (584)(a) (220)(b)

Ending fair value $ 744 $ 32

(a) Included in accumulated other comprehensive (loss) income.

(b) Included in securitization income, net.

Changes in the estimates and assumptions used may have a

significant impact on the Company’s valuation of the retained

interests. The key economic assumptions used in measuring

the interest-only strip asset at the time of issuance as well as

at December 31, 2008, and the sensitivity of the fair value to

immediate 10 percent and 20 percent adverse changes in these

assumptions are as follows (rates are per annum):

Interest-Only Strip

At time of issuance As of December 31, 2008

(Millions, except

rates per annum) 2008 2007 Assumptions

Impact on

fair value

of 10%

adverse

change(a)

Finance

charge

yield 13.5%-15.6% 15.8%-16.3% 13.8%-14.0% $(92.4)(b)

Expected

credit losses 4.3%-5.8% 2.6%-4.3% 9.2%-10.2% $(63.1)(b)

LIBOR 2.7%-4.6% 5.0%-5.4% 0.8%-2.0% $ (7.8)

Monthly

payment

rate 23.8%-24.7% 24.6%-25.6% 23.5% $ (0.2)

Discount

Rate 11.0%-12.0% 12.0% 19.4% $ (0.1)

(a) The impact on fair value of a 20 percent adverse change is approximately two

times the impact of a 10 percent adverse change identified above.

(b) The fair value of the interest-only strip is $32 million as of December 31, 2008.

Therefore, a 10 percent adverse change in the assumption would result in the

fair value of the interest-only strip written down to zero.

The key assumptions and the sensitivity of the current year’s

fair value of the retained subordinated securities to immediate

10 percent and 20 percent adverse changes in these key

assumptions are as follows:

Retained Subordinated Securities

(Millions, except

rates per annum) Assumptions

Impact on fair

value of 10%

adverse change

Impact on fair

value of 20%

adverse change

Discount rate 22.0%-32.6% $(45.0) $(85.4)

LIBOR 2.0%-2.5% $ (5.5) $(10.9)

This sensitivity analysis does not represent management’s

expectations of adverse changes in these assumptions but is

provided as a hypothetical scenario to assess the sensitivity of

the fair value of the retained subordinated interests to changes

in key inputs. Management cannot extrapolate changes in fair

value based on a 10 percent or 20 percent change in all key

assumptions simultaneously in part because the relationship of

the change in one assumption on the fair value of the retained

interest is calculated independently from any change in another

assumption. Changes in one factor may cause changes in

another, which could magnify or offset the sensitivities.