American Express 2013 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2013 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

AMERICAN EXPRESS COMPANY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

all dividends paid by ICBC, as well as ongoing hedge costs. The TRC

matures on August 1, 2014.

Derivatives may give rise to counterparty credit risk, which is the

risk that a derivative counterparty will default on, or otherwise be

unable to perform pursuant to, an uncollateralized derivative

exposure. The Company manages this risk by considering the current

exposure, which is the replacement cost of contracts on the

measurement date, as well as estimating the maximum potential value

of the contracts over the next 12 months, considering such factors as

the volatility of the underlying or reference index. To mitigate

derivative credit risk, counterparties are required to be pre-approved

by the Company and rated as investment grade. Counterparty risk

exposures are centrally monitored by the Company. Additionally, in

order to mitigate the bilateral counterparty credit risk associated with

derivatives, the Company has in certain instances entered into master

netting agreements with its derivative counterparties, which provide a

right of offset for certain exposures between the parties. A significant

portion of the Company’s derivative assets and liabilities as of

December 31, 2013 and 2012 is subject to such master netting

agreements with its derivative counterparties. There are no instances

in which management makes an accounting policy election to not net

assets and liabilities subject to an enforceable master netting

agreement on the Company’s Consolidated Balance Sheets. To further

mitigate bilateral counterparty credit risk, the Company exercises its

rights under executed credit support agreements with certain of its

derivative counterparties. These agreements require that, in the event

the fair value change in the net derivatives position between the two

parties exceeds certain dollar thresholds, the party in the net liability

position posts collateral to its counterparty. All derivative contracts

cleared through a central clearinghouse are collateralized to the full

amount of the fair value of the contracts.

In relation to the Company’s credit risk, under the terms of the

derivative agreements it has with its various counterparties, the

Company is not required to either immediately settle any outstanding

liability balances or post collateral upon the occurrence of a specified

credit risk-related event. Based on the assessment of credit risk of the

Company’s derivative counterparties as of December 31, 2013 and

2012, the Company does not have derivative positions that warrant

credit valuation adjustments.

The Company’s derivatives are carried at fair value on the

Consolidated Balance Sheets. The accounting for changes in fair value

depends on the instruments’ intended use and the resulting hedge

designation, if any, as discussed below. Refer to Note 3 for a

description of the Company’s methodology for determining the fair

value of derivatives.

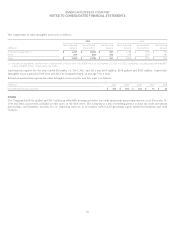

The following table summarizes the total fair value, excluding interest accruals, of derivative assets and liabilities as of December 31:

Other Assets

Fair Value

Other Liabilities

Fair Value

(Millions) 2013 2012 2013 2012

Derivatives designated as hedging instruments:

Interest rate contracts

Fair value hedges $ 455 $ 824 $2$—

Total return contract

Fair value hedge 8——19

Foreign exchange contracts

Net investment hedges 174 43 116 150

Total derivatives designated as hedging instruments 637 867 118 169

Derivatives not designated as hedging instruments:

Foreign exchange contracts, including certain embedded derivatives(a) 64 75 95 160

Total derivatives not designated as hedging instruments 64 75 95 160

Total derivatives, gross 701 942 213 329

Cash collateral netting(b) (336) (326) —(21)

Derivative asset and derivative liability netting(c) (36) (23) (36) (23)

Total derivatives, net(d) $ 329 $ 593 $ 177 $ 285

(a) Includes foreign currency derivatives embedded in certain operating agreements.

(b) Represents the offsetting of derivative instruments and the right to reclaim cash collateral (a receivable) or the obligation to return cash collateral (a payable) arising

from derivative instrument(s) executed with the same counterparty under an enforceable master netting arrangement. Additionally, the Company received noncash

collateral in the form of security interest in U.S. Treasury securities with a fair value of nil and $335 million as of December 31, 2013 and 2012, respectively, none of

which was sold or repledged. Such noncash collateral effectively further reduces the Company’s risk exposure to $329 million and $258 million as of December 31,

2013 and 2012, respectively, but does not reduce the net exposure on the Company’s Consolidated Balance Sheets. Additionally, the Company posted $26 million

and nil as of December 31, 2013 and 2012, respectively, as initial margin on its centrally cleared interest rate swaps not netted against the derivative balances.

(c) Represents the amount of netting of derivative assets and derivative liabilities executed with the same counterparty under an enforceable master netting

arrangement.

(d) The Company has no individually significant derivative counterparties and therefore, no significant risk exposure to any single derivative counterparty. The total net

derivative assets and derivative liabilities are presented within other assets and other liabilities on the Company’s Consolidated Balance Sheets.

88