Apple 2007 Annual Report Download - page 110

Download and view the complete annual report

Please find page 110 of the 2007 Apple annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

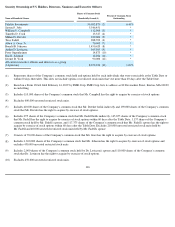

|

|

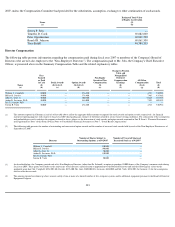

The Committee reviews compensation practices at peer companies (gathered from SEC filings and the Radford High Technology

compensation survey) at a high level to ensure that Apple's total compensation is within a reasonably competitive range. The

Committee, however, does not attempt to set compensation components to meet specific benchmarks, such as salaries "above the

median" or equity compensation "at the 75

th

percentile." Furthermore, the Committee believes that excessive reliance on

benchmarking is detrimental to shareholder interests because it can result in compensation that is unrelated to the value delivered

by the named executive officers.

7.

Tax and Accounting Considerations

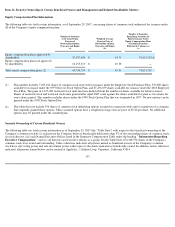

Tax Deductibility of Compensation Expense. Section 162(m) of the Internal Revenue Code places a limit of $1,000,000 on the

amount of compensation to certain officers that may be deducted by Apple as a business expense in any tax year unless, among

other things, the compensation is performance-based and has been approved by the shareholders. To qualify as performance-

based compensation, the amount of compensation must depend on the officer's performance against pre-determined performance

goals established by a committee that consists solely of at least two "outside" directors who have never been employed by Apple

or its subsidiaries. Two Compensation Committee members, Mr. Gore and Mr. Drexler, qualify as outside directors under the IRS

definition. Although Mr. Campbell is an independent director under SEC and NASDAQ governance standards, he does not

qualify as an outside director because he was an officer of Apple from 1983 to 1987 and an Apple subsidiary from 1987 to 1991.

For this reason, he does not discuss or vote on any Section 162(m)-related matters.

Salaries for the named executive officers do not qualify as performance-based compensation. Apple's performance-based cash

incentives, however, are exempt from the Section 162(m) limit because they are paid based on predetermined goals established by

the Compensation Committee pursuant to the shareholder-approved Performance Bonus Plan. The RSUs do not qualify as

performance-based compensation for purposes of Section 162(m) because vesting is based on continued employment rather than

specific performance goals. See page 103 for an explanation of Apple's decision not to implement performance-based vesting.

Tax Implications for Officers. Section 409A of the Internal Revenue Code imposes additional income taxes on executive

officers for certain types of deferred compensation that do not comply with Section 409A. Because Apple does not generally

provide deferred compensation to the named executive officers, this limitation has no impact on the structure of the compensation

program for the officers. Section 280G of the Internal Revenue Code imposes an excise tax on payments to executives of

severance or change of control compensation that exceed the levels specified in Section 280G. The named executive officers

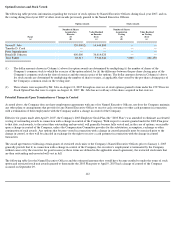

could receive the amounts shown on the table on page 113 as severance or change of control payments, but the Committee does

not consider their potential impact in compensation program design.

Accounting Considerations. The Committee also considers the accounting and cash flow implications of various forms of

executive compensation. In its financial statements, Apple records salaries and performance-based compensation incentives as

expenses in the amount paid, or to be paid, to the named executive officers. Accounting rules also require Apple to record an

expense in its financial statements for equity awards, even though equity awards are not paid as cash to employees. The

accounting expense of equity awards to employees is calculated in accordance with SFAS 123R. The Committee believes,

however, that the many advantages of equity compensation, as discussed above, more than compensate for the non-cash

accounting expense associated with them.

106