Apple 2007 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2007 Apple annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

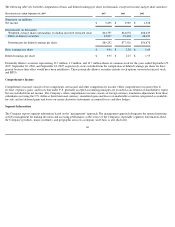

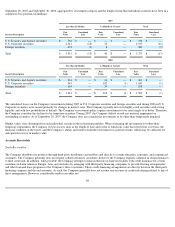

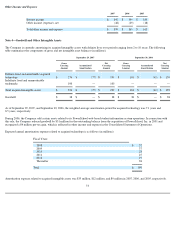

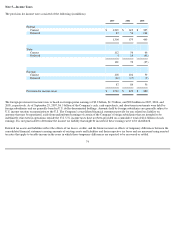

Total amortization related to capitalized software development costs was $13 million, $18 million, and $16 million in 2007, 2006, and 2005,

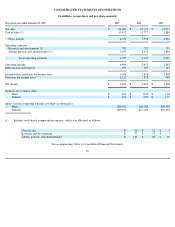

respectively.

Advertising Costs

Advertising costs are expensed as incurred. Advertising expense was $467 million, $338 million, and $287 million for 2007, 2006, and 2005,

respectively.

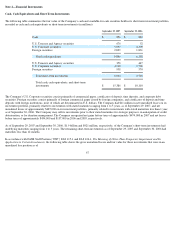

Stock-Based Compensation

On September 25, 2005, the Company adopted SFAS No. 123 (revised 2004) ("SFAS No. 123R"), Share-Based Payment , which addresses the

accounting for stock-based payment transactions in which an enterprise receives employee services in exchange for (a) equity instruments of the

enterprise or (b) liabilities that are based on the fair value of the enterprise's equity instruments or that may be settled by the issuance of such

equity instruments. In January 2005, the Securities and Exchange Commission ("SEC") issued SAB No. 107, which provides supplemental

implementation guidance for SFAS No. 123R. SFAS No. 123R eliminates the ability to account for stock-

based compensation transactions using

the intrinsic value method under Accounting Principles Board ("APB") Opinion No. 25, Accounting for Stock Issued to Employees , and instead

generally requires that such transactions be accounted for using a fair-value-based method. The Company uses the Black-Scholes-Merton

("BSM") option-pricing model to determine the fair-value of stock-based awards under SFAS No. 123R, consistent with that used for pro forma

disclosures under SFAS No. 123, Accounting for Stock-Based Compensation .

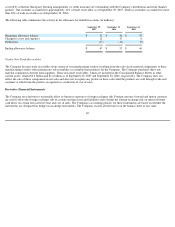

SFAS No. 123R prohibits recognition of a deferred tax asset for an excess tax benefit that has not been realized. The Company will recognize a

benefit from stock-based compensation in equity if an incremental tax benefit is realized by following the ordering provisions of the tax law. In

addition, the Company accounts for the indirect effects of stock-based compensation on the research tax credit, the foreign tax credit, and the

domestic manufacturing deduction through the income statement.

Prior to the adoption of SFAS No. 123R, the Company measured compensation expense for its employee stock-based compensation plans using

the intrinsic value method prescribed by APB Opinion No. 25. The Company applied the disclosure provisions of SFAS No. 123 as amended by

SFAS No. 148, Accounting for Stock-Based Compensation—Transition and Disclosure, as if the fair-value-based method had been applied in

measuring compensation expense. Under APB Opinion No. 25, when the exercise price of the Company's employee stock options was equal to

the market price of the underlying stock on the date of the grant, no compensation expense was recognized.

64