Electronic Arts 2000 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2000 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

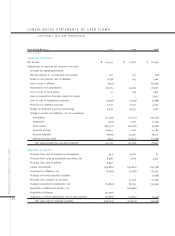

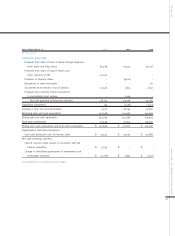

|

|

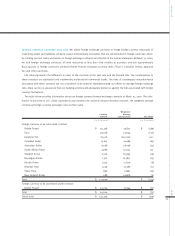

Software Licenses:

For those agreements which provide the customers the right to multiple copies in exchange for guaranteed

minimum royalty amounts, revenue is recognized at delivery of the product master or the first copy. Per copy royalties on sales

that exceed the guarantee are recognized as earned.

Revenue from the licensing of software was $21,704,000, $17,788,000, and $15,431,000 for the fiscal years ended March 31,

2000, 1999 and 1998, respectively.

(C) CASH AND INVESTMENTS Cash equivalents consist of highly liquid investments with insignificant rate risk and with matu-

rities of three months or less at the date of purchase. Short-term investments include securities with maturities greater than

three months and less than one year, except for certain investments with stated maturities greater than one year. Long-term

investments consist of securities with maturities greater than one year.

The Company accounts for investments under Statement of Financial Accounting Standards No. 115,

“Accounting for Certain

Investments in Debt and Equity Securities,”

(“SFAS 115”). The Company’s policy is to protect the value of its investment port-

folio and to minimize principal risk by earning returns based on current interest rates. Management determines the appropriate

classification of its debt and equity securities at the time of purchase and reevaluates such designation as of each balance

sheet date. Debt securities are classified as held-to-maturity when the Company has the positive intent and ability to hold the

securities to maturity. Securities classified as held-to-maturity are carried at amortized cost, which is adjusted for amortization

of premiums and accretion of discounts to maturity. Such amortization is included in interest income. Debt securities, not clas-

sified as held-to-maturity, are classified as available-for-sale and are stated at fair value. Securities sold is based on the specific

identification method.

(D) PREPAID ROYALTIES Prepaid royalties consist primarily of prepayments for manufacturing royalties, original equipment

manufacturer (OEM) fees and license fees paid to celebrities and professional sports organizations for use of their trade

name. Also included in prepaid royalties are prepayments made to independent software developers under development

arrangements that have alternative future uses. Prepaid royalties are expensed at the contractual royalty rate as cost of goods

sold based on actual net product sales. Management evaluates the future realization of prepaid royalties quarterly and charges

to income any amounts that management deems unlikely to be realized through product sales. Royalty advances are classified

as current and non-current assets based upon estimated net product sales for the following year. The current portion of pre-

paid royalties, included in other current assets, was $54,970,000 and $35,057,000 at March 31, 2000 and 1999, respectively.

The long-term portion of prepaid royalties, included in other assets, was $11,373,000 and $7,602,000 at March 31, 2000 and

1999, respectively.

(E) SOFTWARE DEVELOPMENT COSTS Research and development costs, which consist primarily of software development

costs, are expensed as incurred. Statement of Financial Accounting Standards No. 86,

“Accounting for the Cost of Computer

Software to be Sold, Leased, or Otherwise Marketed”

(“SFAS 86”), provides for the capitalization of certain software develop-

ment costs incurred after technological feasibility of the software is established or for development costs that have alternative

future uses. Under the Company’s current practice of developing new products, the technological feasibility of the underlying

software is not established until substantially all product development is complete, which generally includes the development

of a working model. The software development costs that have been capitalized to date have been insignificant.

EA 2000 AR

43

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS