HSBC 2010 Annual Report Download - page 311

Download and view the complete annual report

Please find page 311 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

301 -

302

302 -

303

303 -

304

304 -

305

305 -

306

306 -

307

307 -

308

308 -

309

309 -

310

310 -

311

311 -

312

312 -

313

313 -

314

314 -

315

315 -

316

316 -

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

309

Overview Operating & Financial Review Governance Financial Statements Shareholder Information

For all financial instruments where fair values are determined by reference to externally quoted prices or observable

pricing inputs to models, independent price determination or validation is utilised. In inactive markets, direct

observation of a traded price may not be possible. In these circumstances, HSBC will source alternative market

information to validate the financial instrument’s fair value, with greater weight given to information that is

considered to be more relevant and reliable. The factors that are considered in this regard are, inter alia:

• the extent to which prices may be expected to represent genuine traded or tradeable prices;

• the degree of similarity between financial instruments;

• the degree of consistency between different sources;

• the process followed by the pricing provider to derive the data;

• the elapsed time between the date to which the market data relates and the balance sheet date; and

• the manner in which the data was sourced.

For fair values determined using a valuation model, the control framework may include, as applicable, independent

development or validation of (i) the logic within valuation models; (ii) the inputs to those models; (iii) any

adjustments required outside the valuation models; and (iv) where possible, model outputs. Valuation models are

subject to a process of due diligence and calibration before becoming operational and are calibrated against external

market data on an ongoing basis.

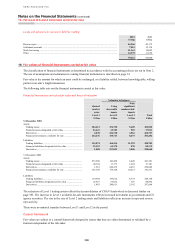

The fair value governance structure is as follows:

Finance

Responsible for determining

fair value:

•Establishing accounting

policies for fair value

•Establishing procedures

governing valuation

•Ensuring compliance with

all relevant accounting

standards

Group Finance Director

Valuation Committees

Consist of valuation experts

from several independent

support functions

(product control, market

risk management, quantitative

risk and valuation group

and finance), in addition

to senior management

Valuation Committee

Review Group

Chaired by Global Head of

Product Control,

Global Markets

Consists of heads of

Global Banking and

Markets, finance

and risk functions

Provides

results

Overseen by

and report

all valuations

considered

to have

material

subjectivity

Finance

Responsible for determining

fair value:

•Establishing accounting

policies for fair value

•Establishing procedures

governing valuation

•Ensuring compliance with

all relevant accounting

standards

Group Finance Director

Valuation Committees

Consist of valuation experts

from several independent

support functions

(product control, market

risk management, quantitative

risk and valuation group

and finance), in addition

to senior management

Valuation Committee

Review Group

Chaired by Global Head of

Product Control,

Global Markets

Consists of heads of

Global Banking and

Markets, finance

and risk functions

Provides

results

Overseen by

and report

all valuations

considered

to have

material

subjectivity

Determination of fair value

Fair values are determined according to the following hierarchy:

• Level 1 – quoted market price: financial instruments with quoted prices for identical instruments in active

markets.

• Level 2 – valuation technique using observable inputs: financial instruments with quoted prices for similar

instruments in active markets or quoted prices for identical or similar instruments in inactive markets and

financial instruments valued using models where all significant inputs are observable.

• Level 3 – valuation technique with significant unobservable inputs: financial instruments valued using valuation

techniques where one or more significant inputs are unobservable.

The best evidence of fair value is a quoted price in an actively traded market. The fair values of financial instruments

that are quoted in active markets are based on bid prices for assets held and offer prices for liabilities issued. Where a

financial instrument has a quoted price in an active market and it is part of a portfolio, the fair value of the portfolio is

calculated as the product of the number of units and quoted price and no block discounts are applied. In the event that

the market for a financial instrument is not active, a valuation technique is used.

The judgement as to whether a market is active may include, but is not restricted to, the consideration of factors such

as the magnitude and frequency of trading activity, the availability of prices and the size of bid/offer spreads. The

bid/offer spread represents the difference in prices at which a market participant would be willing to buy compared

with the price at which they would be willing to sell. In inactive markets, obtaining assurance that the transaction

price provides evidence of fair value or determining the adjustments to transaction prices that are necessary to

measure the fair value of the instrument requires additional work during the valuation process.