Lowe's 2000 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2000 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

Lowe’s Companies, Inc.

20

to $5.2billion at January 28, 2000. The increase in property result-

ed primarily from the Company’s store expansion program, includ-

ing land, building, store equipment, fixtures and displays.

Net interest costs as a percent of sales were 0.7% for 2000,

0.5% for 1999 and 0.6% for 1998. Net interest costs totaled

$120.8million in 2000, $84.9million in 1999 and $80.9million

in 1998. Interest costs relating to capital leases were $42.0, $42.6

and $39.3million for 2000, 1999 and 1998, respectively. See the

discussion of liquidity and capital resources below.

The Company’s effective income tax rates were 36.8%, 36.7%

and 36.4% in 2000, 1999 and 1998, respectively. The higher rates

in 2000 and 1999 were primarily related to expansion into states

with higher state income tax rates. The rate increase in 1999 is also

attributable to the impact of non-deductible merger expenses.

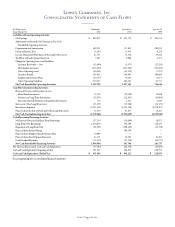

Liquidity and Capital Resources

Primary sources of liquidity are cash flows from operating activi-

ties and certain financing activities. Net cash provided by operat-

ing activities was $1.1billion for 2000. This compares to $1.2

billion and $746.0million in 1999 and 1998, respectively. The

decrease in net cash provided by operating activities for 2000 is

primarily the result of an increase in inventory, net of an increase

in accounts payable, from year to year, which was partially offset

by increased earnings and a larger increase in other operating

liabilities. The increase in net cash provided by operating activi-

ties for 1999 and 1998 is primarily related to increased earnings

and various operating liabilities which were offset by an increase

in inventory, net of an increase in accounts payable, from year

to year. Working capital at February 2, 2001 was $1.2billion

compared to $1.3billion at January 28, 2000.

The primary component of net cash used in investing activi-

ties continues to be new store facilities in connection with

the Company’s expansion plan. Cash acquisitions of fixed assets

were $2.3billion for 2000. This compares to $1.5billion and $1.1

billion for 1999 and 1998, respectively. Retail selling space as of

February 2, 2001 increased 19% over the selling space as of

January 28, 2000. The January 28, 2000 selling space total of

57.0million square feet represents a 19% increase over 1998.

Investing activities also include noncash transactions of capital

leases for new store facilities and equipment, the result of which

is to increase long-term debt and property.

Cash flows provided by financing activities were $1.1billion in

2000, $583.5million in 1999 and $283.2million in 1998. The

major cash components of financing activities in 2000 included

increased cash from the issuance of $500 million principal amount

of 8.25% notes due June 1, 2010 and $500 million principal

amount of 7.50% notes due December 15, 2005. These cash

inflows were offset by a decrease in cash due to the payment of

$53.5million in cash dividends and $61.3million in scheduled debt

maturities. In 1999, financing activities included the issuance of

$400 million principal amount of 6.5% debentures and $348.3

million in net proceeds from a common stock offering. These pro-

ceeds were offset by a decrease in cash of $47.6million in cash div-

idend payments and $108.3million in scheduled debt repayments.

Major financing activities during 1998 included cash received from

the issuance of $300 million principal amount of debentures offset

by cash dividend payments of $50.8million and $23.3million of

scheduled debt repayments. The ratio of long-term debt to equity

plus long-term debt was 33.3%, 27.6% and 28.9% as of fiscal year

ends 2000, 1999 and 1998, respectively.

In February 2001, the Company issued $1.005 billion principal

of Liquid Yield Option

TM

Notes* (LYONs) at an issue price of

$608.41 per LYON. Interest will not be paid on the LYONs prior

to maturity. On February 16, 2021, the maturity date, the holders

will receive $1,000 per LYON, representing a yield to maturity of

2.5%. Holders may convert their LYONs at any time on or before

the maturity date, unless the LYONs have been purchased or

redeemed previously, into 8.224 shares of the Company’s common

stock per LYON. The Company may redeem for cash all or a por-

tion of the LYONs at any time on or after February 16, 2004 at a

price equal to the sum of the issue price and accrued original issue

discount on the redemption date. Holders of the LYONs may

require the Company to purchase all or a portion of their LYONs

on February 16, 2004 at a price of $655.49 per LYON or on

February 16, 2011 at a price of $780.01 per LYON. The Company

may choose to pay the purchase price of the LYONs in cash or

common stock, or a combination of cash and common stock. In

addition, if a change in the control of the Company occurs on or

before February 16, 2004, each holder may require the Company

to purchase, for cash, all or a portion of the holder’s LYONs.

* Trademark of Merrill Lynch & Co., Inc.