Lowe's 2003 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2003 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

|

|

2003 ANNUAL REPORT 21

conditions. However, changes in consumer purchasing patterns

could result in the need for additional reserves. The Company also

records an inventory reserve for the estimated shrinkage between

physical inventories. This reserve is based primarily on actual

shrinkage results from previous physical inventories. Changes

in actual shrinkage results from completed physical inventories

could result in revisions to previously estimated shrinkage

expense. Management believes it has sufficient current and histor-

ical knowledge to record reasonable estimates for both of these

inventory reserves.

Vendor Funds The Company receives funds from vendors in the

normal course of business for a variety of reasons, including pur-

chase-volume-related rebates, defective merchandise allowances,

advertising allowances, reimbursement for selling expenses, dis-

plays and third-party, in-store service-related costs. Management

uses projected purchase volumes to determine earnings rates, vali-

dates those projections based on actual and historical purchase

trends and applies those rates to actual purchase volumes to deter-

mine the amount of funds earned by the Company and receivable

from the vendor. Amounts earned could be impacted if actual

purchase volumes differ from projected purchase volumes. The

Company has historically treated volume-related discounts or

rebates as a reduction of inventory cost and reimbursements of

operating expenses received from vendors as a reduction of those

specific expenses. The Company’s historical accounting treatment

for these vendor-provided funds is consistent with Emerging

Issues Task Force (EITF) 02-16 “Accounting by a Customer

(Including a Reseller) for Certain Consideration Received From a

Vendor” with the exception of certain cooperative advertising

allowances and in-store services provided by third parties for

which the costs are ultimately funded by vendors. The Company

previously treated the cooperative advertising allowances and in-

store service funds as a reduction of the related expense. Under

EITF 02-16, cooperative advertising allowances and in-store serv-

ice funds should be treated as a reduction of inventory cost, unless

they represent a reimbursement of specific, incremental and iden-

tifiable costs incurred by the customer to sell the vendor’s product.

The cooperative advertising and in-store service funds that the

Company receives do not meet the specific, incremental and iden-

tifiable criteria in EITF 02-16. Therefore, for cooperative advertis-

ing and third-party, in-store service fund agreements entered into

after December 31, 2002, which was the effective date of the relat-

ed provision of EITF 02-16, the Company is treating these funds as

a reduction in the cost of inventory and recognizing these funds as

a reduction of cost of sales when the inventory is sold. There is no

impact to the timing of when the funds are received from vendors

or the associated cash flows, but there is an impact to the timing of

income recognition. This accounting change did not have a mate-

rial impact on the fiscal 2003 financial results, since substantially all

of the cooperative advertising allowance and in-store service fund

agreements for fiscal 2003 were entered into prior to December 31,

2002. The Company estimates that this one-time change in

accounting will reduce fiscal 2004 earnings per share by approxi-

mately $0.13 per share.

Self-Insurance The Company is self-insured for certain losses

relating to worker’s compensation, automobile, general and prod-

uct liability claims. Self-insurance claims filed and claims incurred

but not reported are accrued based upon management’s estimates

of the discounted aggregate liability for uninsured claims incurred

using actuarial assumptions followed in the insurance industry

and historical experience. These estimates are subject to changes in

forecasted payroll, sales and vehicle units, as well as the frequency

and severity of claims. Although management believes it has the

ability to adequately record estimated losses related to claims, it is

possible that actual results could differ from recorded self-insur-

ance liabilities.

Operations.

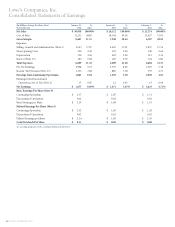

Net earnings for 2003 increased 28% to $1.9 billion or 6.1% of

sales compared to $1.5 billion or 5.6% of sales for 2002. Net earn-

ings for 2002 increased 44% to $1.5 billion or 5.6% of sales com-

pared to $1.0 billion or 4.7% of sales for 2001. Diluted earnings per

share were $2.34 for 2003 compared to $1.85 for 2002 and $1.30

for 2001. Return on beginning assets, defined as net earnings divid-

ed by beginning total assets, was 11.7% for 2003, compared to

10.7% for 2002 and 9.0% for 2001, and return on beginning share-

holders’ equity, defined as net earnings divided by beginning

shareholders’ equity, was 22.6% for 2003, compared to 22.0% for

2002 and 18.6% for 2001. Return on invested capital, defined as net

earnings plus after-tax interest divided by the sum of beginning

debt and equity, was 16.5% for 2003, compared to 15.1% for 2002

and 13.8% for 2001.

Sales amounts are from continuing operations and exclude

sales from the Contractor Yard locations. The Company recorded

sales of $30.8 billion in 2003, an 18% increase over 2002 sales of

$26.1 billion. Sales for 2002 were 20% higher than 2001 levels. The

increases in sales are attributable to the Company’s ongoing store

expansion and relocation program and comparable store sales

increases. Comparable store sales increased 6.7% in 2003, com-

pared to 5.8% in 2002. Average ticket increased 4% from $56.80 in

2002 to $59.21 in 2003 due in part to the success of the up-the-

continuum initiative as well as Lowe’s credit programs.

The comparable store sales increase in 2003 primarily resulted

from improved sales in every merchandising category due to the

initiatives previously described. During the year, the Company

experienced its strongest sales increases in lumber, building mate-

rials, outdoor power equipment, paint, flooring and home organi-

zation. Major appliances continue to perform well and also exceed-

ed the Company average comparable store sales increase. In addi-

tion, millwork, hardware, walls & windows, nursery and cabinets

performed at approximately the overall corporate average compa-

rable store sales increase. Comparable store sales were positive for

every product category and all geographic regions due in part to

the implementation of the merchandising and operations strate-

gies previously discussed. The Company experienced slight infla-

tion in lumber and building material prices during the year, which

positively impacted comparable store sales by 50 basis points. The

following table presents sales and store information excluding dis-

continued operations: