Lowe's 2003 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2003 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

|

|

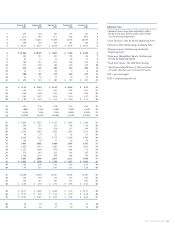

2003 ANNUAL REPORT 33

January 30, 2004

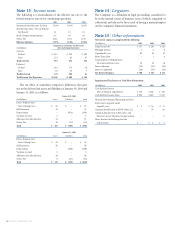

Gross Gross

(In Millions) Amortized Unrealized Unrealized Fair

Type Cost Gains Losses Value

Municipal Obligations $ 160 $ – $ – $ 160

Money Market Preferred Stock 18 – – 18

Classified as Short-Term 178 – – 178

Municipal Obligations 92 – – 92

Corporate Notes 32 – – 32

Agency Bonds 23 – – 23

Asset-Backed Obligations 16 – – 16

Mutual Funds 6 – – 6

Classified as Long-Term 169 – – 169

Total $ 347 $ – $ – $ 347

January 31, 2003

Gross Gross

(In Millions) Amortized Unrealized Unrealized Fair

Type Cost Gains Losses Value

Municipal Obligations $ 82 $ – $ – $ 82

Money Market Preferred Stock 186 – – 186

Corporate Notes 5 – – 5

Classified as Short-Term 273 – – 273

Municipal Obligations 11 – – 11

Agency Bonds 17 – – 17

Mutual Funds 1 – – 1

Classified as Long-Term 29 – – 29

Total $ 302 $ – $ – $ 302

The unrealized net gain on available-for-sale securities was $159

thousand, net of the tax expense of $58 thousand at January 30, 2004.

The unrealized net loss on available-for-sale securities was $285 thou-

sand, net of the tax benefit of $172 thousand at January 31, 2003.

The proceeds from sales of available-for-sale securities were

$204 million, $2 million and $1 million for 2003, 2002 and 2001,

respectively. Gross realized gains and losses on the sale of available-

for-sale securities were not significant for any of the periods pre-

sented. The municipal obligations and agency bonds classified as

long-term at January 30, 2004 will mature in one to five years.

Note 4

|

Property and

accumulated depreciation.

Property is summarized by major class in the following table:

January 30, January 31,

(In Millions) 2004 2003

Cost:

Land $ 3,635 $ 3,133

Buildings 5,950 5,092

Equipment 4,355 3,663

Leasehold Improvements 1,133 929

Total Cost 15,073 12,817

Accumulated Depreciation and Amortization (3,128) (2,465)

Net Property $ 11,945 $ 10,352

The estimated depreciable lives, in years, of the Company’s prop-

erty are: buildings, 20 to 40; store, distribution and office equipment,

3 to 10; leasehold improvements, generally the life of the related lease.

Included in net property are assets under capital lease of $539

million, less accumulated depreciation of $108 million at January 30,

2004, and $543 million, less accumulated depreciation of $93 mil-

lion at January 31, 2003.

Note 5

|

Impairment and

store closing costs.

The Company periodically reviews the carrying value of long-lived

assets for potential impairment. When management commits to

close or relocate a store location, or when there are indicators that

the carrying value of a long-lived asset may not be recoverable, the

Company evaluates the carrying value of the asset in relation to its

expected future cash flows. If the carrying value of the assets is

greater than the expected future cash flows and the fair value of the

assets is less than the carrying value, a provision is made for the

impairment of the assets based on the excess of carrying value over

fair value. The fair value of the assets is generally based on internal

or external appraisals and the Company’s historical experience.

The provision for impairment is included in SG&A.

Closed store real estate is included in other assets and amounted

to $89 million and $94 million at January 30, 2004 and January 31,

2003, respectively.

When leased locations are closed, a liability is recognized for the

fair value of future contractual obligations, including property taxes,

utilities and common area maintenance, net of anticipated sublease

income. The provision for store closing costs is included in SG&A.

The following table illustrates the store closing liability and the

respective changes in the obligation, which is included in other

current liabilities in the consolidated balance sheet.

(In Millions) Store Closing Liability

Balance at February 2, 2001 $ 19

Accrual for Store Closing Costs 6

Lease Payments, Net of Sublease Income (8)

Balance at February 1, 2002 $ 17

Accrual for Store Closing Costs 9

Lease Payments, Net of Sublease Income (10)

Balance at January 31, 2003 $ 16

Accrual for Store Closing Costs 12

Lease Payments, Net of Sublease Income (9)

Balance at January 30, 2004 $ 19

Note 6

|

Short-term borrowings

and lines of credit.

The Company has an $800 million senior credit facility. The facili-

ty is split into a $400 million five-year tranche, expiring in August

2006 and a $400 million 365-day tranche, expiring in July 2004,

which is renewable annually. The facility is used to support the

Company’s $800 million commercial paper program and for short-

term borrowings. Borrowings made are priced based upon market

conditions at the time of funding in accordance with the terms of

the senior credit facility. The senior credit facility contains certain

restrictive covenants, which include maintenance of a specific

financial ratio. The Company was in compliance with those

covenants at January 30, 2004. Fifteen banking institutions are par-

ticipating in the $800 million senior credit facility and, as of January

30, 2004, there were no outstanding loans under the facility.

In July 2003, the Company terminated a $100 million revolving

credit and security agreement with a financial institution which was

scheduled to expire in November 2003. The remaining outstanding

balance of $50 million was repaid at the time of termination.