Lowe's 2003 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2003 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

|

|

2003 ANNUAL REPORT 31

flows and the fair value of the assets is less than the carrying value,

a provision is made for the impairment of the assets based on the

excess of carrying value over fair value.

When a leased location is closed, a provision is made for the fair

value of future contractual obligations, including property taxes,

utilities, and common area maintenance, net of anticipated sub-

lease income. Provisions for impairment and store closing costs are

included in selling, general and administrative expenses (SG&A).

Leases Assets under capital leases are amortized in accordance

with the Company’s normal depreciation policy for owned assets or

over the lease term, if shorter, and the charge to earnings is includ-

ed in depreciation expense in the consolidated financial statements.

Self-Insurance The Company is self-insured for certain losses

relating to worker’s compensation, automobile, property, general

and product liability claims. The Company has stop loss coverage

to limit the exposure arising from these claims. Self-insurance

claims filed and claims incurred but not reported are accrued

based upon management’s estimates of the discounted aggregate

liability for uninsured claims incurred using actuarial assumptions

followed in the insurance industry and historical experience.

Although management believes it has the ability to adequately

record estimated losses related to claims, it is possible that actual

results could differ from recorded self-insurance liabilities.

Income Taxes Income taxes are provided for temporary dif-

ferences between the tax and financial accounting bases of assets

and liabilities using the asset and liability method. The tax effects

of such differences are reflected in the balance sheet at the enacted

tax rates expected to be in effect when the differences reverse.

Store Opening Costs Costs of opening new or relocated retail

stores are charged to operations as incurred.

Revenue Recognition The Company recognizes revenues

when sales transactions occur and customers take possession of the

merchandise. A provision for anticipated merchandise returns is

provided in the period that the related sales are recorded.

Revenues from product installation services are recognized

when the installation is completed. Revenues from gift cards are

deferred and recognized when the cards are redeemed.

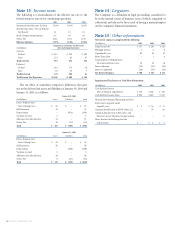

Advertising Costs associated with advertising are charged to

operations as incurred. Gross advertising expenses were $682 mil-

lion, $608 million and $519 million in 2003, 2002 and 2001, respec-

tively. Cooperative advertising vendor funds of $673 million, $583

million and $481 million in 2003, 2002 and 2001, respectively were

recorded as a reduction of these expenses with the net amount

included in SG&A.

Vendor Funds The Company receives funds from vendors in

the normal course of business for a variety of reasons including

purchase-volume-related rebates, defective merchandise allowances,

cooperative advertising allowances, reimbursement for selling

expenses, displays and third-party, in-store service related costs.

The Company has historically treated volume-related discounts or

rebates as a reduction of inventory cost and reimbursements of

operating expenses received from vendors as a reduction of those

specific expenses. The Company’s historical accounting treatment

for these vendor provided funds is consistent with Emerging Issues

Task Force (EITF) 02-16 with the exception of certain cooperative

advertising allowances and in-store services provided by third

parties for which the costs are ultimately funded by vendors.

The Company previously treated the cooperative advertising

allowances and in-store service funds as a reduction of the related

expense. Under EITF 02-16, cooperative advertising allowances

and in-store service funds should be treated as a reduction of

inventory cost, unless they represent a reimbursement of specific,

incremental and identifiable costs incurred by the customer to sell

the vendor’s product.

The cooperative advertising agreements with the Company’s

vendors provide funds for general Company advertising to drive

customer traffic, which in turn, increases sales of the vendors’

products. These funds did not meet the specific, incremental and

identifiable criteria in EITF 02-16. Therefore, for cooperative

advertising agreements entered into after December 31, 2002, the

Company is treating cooperative advertising funds as a reduction

in the cost of inventory and recognizing these funds as a reduction

of cost of sales when the inventory is sold.

The third-party, in-store service fund agreements with the

Company’s vendors provide funds for third parties to provide gen-

eral merchandising functions within the Company’s stores. Third-

party vendors providing these functions service multiple areas and

products within the Company’s retail stores. Neither the Company

nor the third-party service providers have the ability to specifically

identify time spent on a merchandise vendor’s products in multiple

locations and match them to specific funds from merchandise ven-

dors. As such, these funds did not meet the specific, incremental

and identifiable criteria in EITF 02-16. Therefore, for third-party,

in-store service fund agreements entered into after December 31,

2002, the Company is treating third-party, in-store service funds as

a reduction in the cost of inventory and recognizing these funds as

a reduction of cost of sales when the inventory is sold. Third-party,

in-store service costs are included in SG&A and are presented net of

third-party, in-store service vendor funds of $175 million, $69 mil-

lion and $30 million in 2003, 2002 and 2001, respectively.

This accounting change did not have a material impact on the

2003 financial statements since substantially all of the cooperative

advertising allowance and in-store service fund agreements for

2003 were entered into prior to December 31, 2002, the effective

date of the related provision of EITF 02-16.

Stock-Based Compensation Prior to 2003, the Company

accounted for its stock-based compensation plans under the recog-

nition and measurement provisions of Accounting Principles

Board (APB) Opinion No. 25, “Accounting for Stock Issued to

Employees,” and related Interpretations. Therefore, no stock-based

employee compensation is reflected in 2002 or 2001 net income,

other than for restricted stock grants, as all options granted under

those plans had an exercise price equal to the market value of the

underlying common stock on the date of grant.

Effective February 1, 2003, the Company adopted the fair value

recognition provisions of Statement of Financial Accounting

Standards (SFAS) No. 123, “Accounting for Stock-Based

Compensation,” prospectively for all employee awards granted or

modified after January 31, 2003. Therefore, in accordance with the

requirements of SFAS No. 148, “Accounting for Stock-Based

Compensation-Transition and Disclosure,” the cost related to stock-

based employee compensation included in the determination of net