Lowe's 2003 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2003 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

|

|

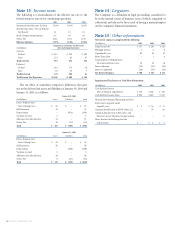

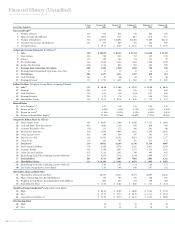

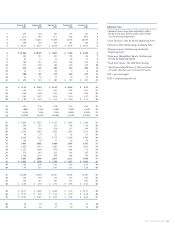

34 LOWE’S COMPANIES, INC.

Five banks have extended lines of credit aggregating $330 mil-

lion for the purpose of issuing documentary letters of credit and

standby letters of credit. These lines do not have termination dates

but are reviewed periodically. Commitment fees ranging from

.25% to .50% per annum are paid on the amounts of standby let-

ters of credit. Outstanding letters of credit totaled $161 million as

of January 30, 2004 and $122 million as of January 31, 2003.

At January 31, 2003, the interest rate on short-term borrowings

was 1.4%. There were no short-term borrowings outstanding at

January 30, 2004.

Note 7

|

Long-term debt.

Fiscal Year

(In Millions) of Final January 30, January 31,

Debt Category Interest Rates Maturity 2004 2003

Secured Debt:1

Mortgage Notes 7.00% to 9.25% 2028 $ 45 $ 55

Unsecured Debt:

Debentures 6.50% to 6.88% 2029 692 692

Notes 7.50% to 8.25% 2010 996 995

Medium-Term Notes

Series A 7.35% to 8.20% 2023 74 74

Medium-Term Notes2

Series B 6.70% to 7.61% 2037 267 266

Senior Notes 6.38% 2005 100 100

Convertible Notes 0.9% to 2.5% 2021 1,136 1,119

Capital Leases 6.58% to 19.57% 2029 445 464

Total Long-Term Debt 3,755 3,765

Less Current Maturities 77 29

Long-Term Debt, Excluding

Current Maturities $ 3,678 $ 3,736

1Real properties with an aggregate book value of $86 million were pledged as

collateral at January 30, 2004 for secured debt.

2Approximately 37% of these Medium-Term Notes may be put at the option of the

holder on either the tenth or twentieth anniversary date of the issue at par value. None

of these notes are currently putable.

Debt maturities, exclusive of capital leases, for the next five fis-

cal years and thereafter are as follows: 2004, $54 million; 2005, $608

million; 2006, $8 million; 2007, $61 million; 2008, $6 million;

thereafter, $3,036 million.

The Company’s debentures, senior notes, medium-term notes

and convertible notes contain certain restrictive covenants, includ-

ing maintenance of a specific financial ratio. The Company was in

compliance with all covenants in these agreements at January 30,

2004 and January 31, 2003.

In October 2001, the Company issued $580.7 million aggregate

principal of senior convertible notes at an issue price of $861.03 per

note. Interest on the notes, at the rate of 0.8610% per year on the prin-

cipal amount at maturity, is payable semiannually in arrears until

October 2006. After that date, the Company will not pay cash interest

on the notes prior to maturity. Instead, in October 2021 when the

notes mature,a holder will receive $1,000 per note, representing a yield

to maturity of approximately 1%. Holders may convert their notes

into 17.212 shares of the Company’s common stock, subject to adjust-

ment, only if: the sale price of the Company’s common stock reaches

specified thresholds, the credit rating of the notes is below a specified

level, the notes are called for redemption, or specified corporate trans-

actions have occurred. Holders may require the Company to purchase

all or a portion of their note in October 2006, at a price of $861.03 per

note plus accrued cash interest, if any, or in October 2011, at a price of

$905.06 per note. The Company may choose to pay the purchase price

of the notes in cash or common stock or a combination of cash and

common stock. In addition, if a change in control of the Company

occurs on or before October 2006, each holder may require the

Company to purchase for cash all or a portion of such holder’s notes.

The Company may redeem for cash all or a portion of the notes at any

time beginning October 2006, at a price equal to the sum of the issue

price plus accrued original issue discount and accrued cash interest, if

any, on the redemption date. The conditions that permit conversion

were not satisfied at January 30, 2004.

In February 2001, the Company issued $1.005 billion aggregate

principal of convertible notes at an issue price of $608.41 per note.

Interest will not be paid on the notes prior to maturity in February

2021, at which time the holders will receive $1,000 per note, repre-

senting a yield to maturity of 2.5%. Holders may convert their notes

at any time on or before the maturity date, unless the notes have been

previously purchased or redeemed, into 16.448 shares of the

Company’s common stock per note. Holders of the notes may

require the Company to purchase all or a portion of their notes in

February 2004 at a price of $655.49 per note or in February 2011 at a

price of $780.01 per note. On either of these dates, the Company may

choose to pay the purchase price of the notes in cash or common

stock, or a combination of cash and common stock. In addition, if a

change in control of the Company occurs on or before February

2004, each holder may require the Company to purchase, for cash, all

or a portion of the holder’s notes. Holders of an insignificant num-

ber of notes exercised their right to require the Company to purchase

their notes in February 2004, all of which were purchased in cash.

Note 8

|

Financial instruments.

Cash and cash equivalents, accounts receivable, short-term bor-

rowings, trade accounts payable and accrued liabilities are reflect-

ed in the financial statements at cost which approximates fair

value. Short and long-term investments, classified as available-for-

sale securities, are reflected in the financial statements at fair value.

Estimated fair values for long-term debt have been determined

using available market information and appropriate valuation

methodologies. However, considerable judgment is required in

interpreting market data to develop the estimates of fair value.

Accordingly, the estimates presented herein are not necessarily

indicative of the amounts that the Company could realize in a cur-

rent market exchange. The use of different market assumptions

and/or estimation methodologies may have a material effect on the

estimated fair value amounts. The fair value of the Company’s

long-term debt excluding capital leases is as follows:

January 30, 2004 January 31, 2003

––––––––––––––––––––––––––––––––––––––––––––––––––– ––––––––––––––––––––––––––––––––––––––––––––––

Carrying Fair Carrying Fair

(In Millions) Amount Value Amount Value

Liabilities:

Long-Term Debt

(Excluding Capital Leases) $ 3,310 $ 3,985 $ 3,302 $ 3,747