Lowe's 2015 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2015 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

|

|

19

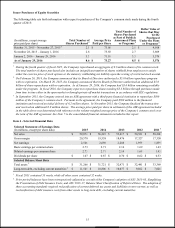

Other Metrics

2015

2014

2013

Comparable sales increase 2

4.8

%

4.3

%

4.8

%

Total customer transactions (in millions)

878

857

828

Average ticket 3

$

67.26

$

65.61

$

64.52

At end of year:

Number of stores

1,857

1,840

1,832

Sales floor square feet (in millions)

202

201

200

Average store size selling square feet (in thousands) 4

109

109

109

Return on average assets 5, 8

7.8

%

8.2

%

6.9

%

Return on average shareholders’ equity 6

28.8

%

24.4

%

17.7

%

Return on invested capital 7

14.1

%

13.9

%

11.5

%

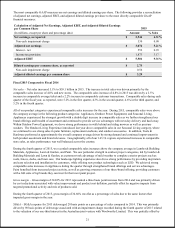

1 EBIT margin, also referred to as operating margin, is defined as earnings before interest and taxes (EBIT) as a percentage of sales. EBIT

margin for fiscal year 2015 was adjusted to exclude the negative 90 basis points impact of the non-cash impairment charge on the

Australian joint venture with Woolworths (Adjusted EBIT margin). Adjusted EBIT is a non-GAAP financial measure. See below for

additional information and a reconciliation to the most comparable GAAP measure.

2 A comparable location is defined as a location that has been open longer than 13 months. A location that is identified for relocation is no

longer considered comparable one month prior to its relocation. The relocated location must then remain open longer than 13 months to

be considered comparable. A location we have decided to close is no longer considered comparable as of the beginning of the month in

which we announce its closing. Acquired locations are included in the comparable sales calculation beginning in the first full month

following the first anniversary of the date of the acquisition. Comparable sales include online sales, which did not have a meaningful

impact for the periods presented.

3 Average ticket is defined as net sales divided by the total number of customer transactions.

4 Average store size selling square feet is defined as sales floor square feet divided by the number of stores open at the end of the period.

The average Lowe’s home improvement store has approximately 112,000 square feet of retail selling space, while the average Orchard

store has approximately 37,000 square feet of retail selling space.

5 Return on average assets is defined as net earnings divided by average total assets for the last five quarters.

6 Return on average shareholders’ equity is defined as net earnings divided by average shareholders’ equity for the last five quarters.

7 Return on invested capital is a non-GAAP financial measure. See below for additional information and a reconciliation to the most

comparable GAAP measure.

8 Fiscal years 2014 and 2013 have been adjusted as a result of the Company’s retrospective adoption of ASU 2015-03, Simplifying the

Presentation of Debt Issuance Costs, and ASU 2015-17, Balance Sheet Classification of Deferred Taxes. The adoption of these accounting

standards required reclassification of current deferred tax assets and liabilities to non-current, as well as reclassification of debt issuance

costs from other assets to long-term debt, excluding current maturities.

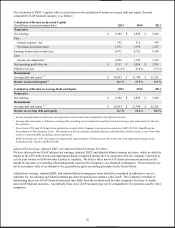

Non-GAAP Financial Measures

Return on Invested Capital

We believe Return on Invested Capital (ROIC) is a meaningful metric for investors because it measures how effectively the

Company uses capital to generate profits.

We define ROIC as trailing four quarters’ net operating profit after tax divided by the average of ending debt and equity for the

last five quarters. Although ROIC is a common financial metric, numerous methods exist for calculating ROIC. Accordingly,

the method used by our management to calculate ROIC may differ from the methods other companies use to calculate their

ROIC. We encourage you to understand the methods used by another company to calculate its ROIC before comparing its

ROIC to ours.

We consider return on average debt and equity to be the financial measure computed in accordance with generally accepted

accounting principles that is the most directly comparable GAAP financial measure to ROIC. The difference between these

two measures is that ROIC adjusts net earnings to exclude tax adjusted interest expense.